SaaS customer acquisition cost measures the sales and marketing cost required to acquire a new paying customer over a defined period. The basic formula is acquisition-related costs divided by new customers acquired, but the metric is useful only when the cost base, customer definition, measurement period, sales motion, and retention context are comparable.

Definition: SaaS customer acquisition cost, often shortened to SaaS CAC, is the average acquisition cost assigned to each new paying customer added during a specific period.

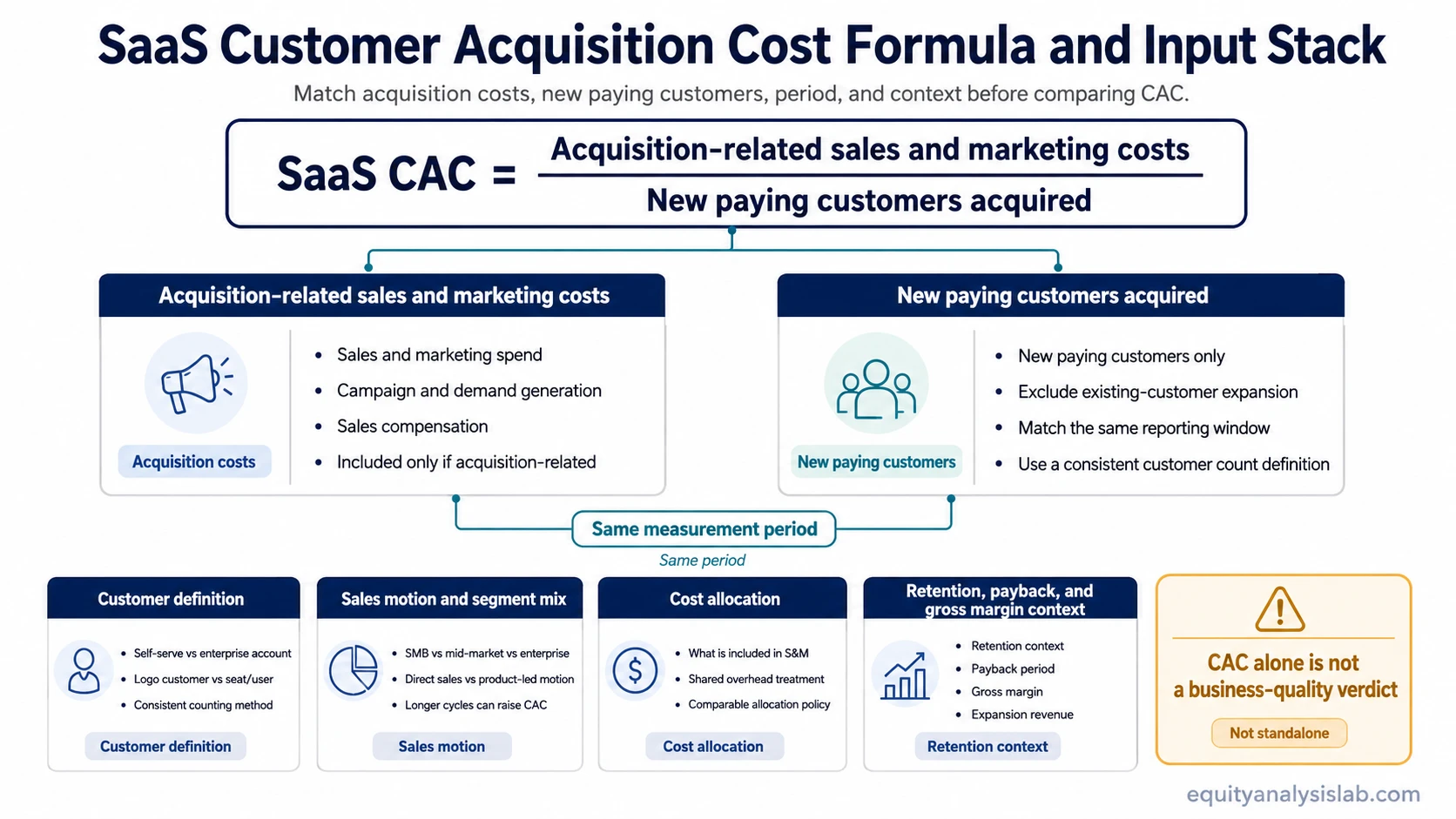

Formula: SaaS CAC = acquisition-related sales and marketing costs / new paying customers acquired.

Investor use: CAC helps evaluate acquisition efficiency, but it does not prove business quality by itself. The same CAC can have a very different meaning when churn, payback period, expansion revenue, gross margin, and customer mix differ.

Key Points About SaaS Customer Acquisition Cost

- SaaS CAC should match acquisition costs and new paying customers over the same measurement period.

- The numerator should focus on acquisition-related sales and marketing costs, not every operating cost in the business.

- The denominator should count new paying customers, not leads, trials, demos, retained customers, or total accounts.

- Peer comparisons are weak unless sales motion, segment mix, customer definition, and cost allocation are similar.

- CAC becomes more useful when read with retention, payback, revenue quality, and acquisition efficiency metrics.

What SaaS Customer Acquisition Cost Means

SaaS customer acquisition cost is a unit economics metric for recurring-revenue businesses. It estimates how much a company spent to add one new paying customer during a defined period.

The SaaS context matters because subscription revenue is earned over time. A company may spend heavily before the customer produces enough gross profit to recover the acquisition cost. For investors, CAC is a business-model quality signal that must be checked against retention, contract value, sales cycle length, payback, and expansion revenue.

SaaS CAC is more specific than broad customer acquisition cost because SaaS companies often have recurring contracts, onboarding periods, sales-led or product-led motions, and revenue expansion after the first sale. Those features change how acquisition cost should be interpreted.

SaaS Customer Acquisition Cost Formula

The standard SaaS customer acquisition cost formula is:

SaaS CAC = acquisition-related sales and marketing costs / new paying customers acquired

The formula is simple, but the inputs are not automatic. A useful calculation requires the numerator and denominator to describe the same acquisition period. If the costs are measured over one quarter but the customers were acquired over a different period, the result can look precise while comparing mismatched data.

| Formula part | What it should capture | Interpretation risk |

|---|---|---|

| Numerator | Acquisition-related sales and marketing costs for the period being measured. | Including broad overhead can overstate CAC. Excluding relevant commissions, campaign spend, or sales costs can understate it. |

| Denominator | New paying customers acquired during the same period. | Counting leads, free trials, demos, or retained customers can make acquisition efficiency look better than it is. |

| Measurement period | The time window used for both acquisition costs and new customers. | Timing mismatches can distort CAC when sales cycles are long or seasonal spending is uneven. |

| Customer definition | The type of customer counted, such as new logo, new paying account, or new subscription customer. | Mixing enterprise accounts, SMB accounts, self-serve customers, and expansion customers weakens comparability. |

| SaaS interpretation context | Retention, gross margin, expansion revenue, payback, and contract size. | CAC alone cannot show whether customer acquisition creates durable value. |

What Belongs in the CAC Numerator

The numerator should usually include costs tied to acquiring new customers. In SaaS, that may include paid marketing, demand generation, sales compensation, sales commissions, sales development costs, marketing software directly used for acquisition, and acquisition-focused events or campaigns.

The harder judgment is allocation. Some sales and marketing spending supports new customer acquisition, while some supports renewals, brand awareness, account management, partner development, or expansion inside existing accounts. A company that assigns all sales and marketing spending to new acquisition may report a higher CAC than a company that allocates only the direct acquisition portion.

For investor comparison, the useful question is whether the reported cost base is consistent across periods and comparable across companies.

What Counts as a New Customer

The denominator should count new paying customers acquired during the same period as the costs in the numerator. It should not count marketing-qualified leads, sales-qualified leads, demos booked, free trial users, website signups, retained customers, or total customers already in the base.

This distinction is especially important in SaaS because product-led companies may generate many free users before conversion, while sales-led companies may spend months closing fewer but larger customers. A low reported CAC based on signups may not be comparable with a higher CAC based on paying enterprise accounts.

The cleaner the customer definition, the more useful the metric becomes. If a company changes the way it defines a new customer, period-over-period CAC comparisons can become unreliable even when the headline formula does not change.

New CAC vs Blended CAC

New CAC focuses on the cost of acquiring new customers. Blended CAC often mixes acquisition activity across a broader customer base or cost base. The blended version can be easier to calculate, but it can hide what matters most: the current marginal cost of adding the next customer.

A SaaS company may look efficient on a blended basis because older cohorts were acquired cheaply or because inbound demand remains strong. That does not necessarily mean new acquisition is still efficient. If paid channels become more expensive, sales cycles lengthen, or win rates decline, new CAC can rise before blended CAC fully reflects the change.

Useful distinction: blended CAC can describe the average acquisition burden across a broader base, while new CAC is better for judging the current cost of growth. Investors usually need both the average picture and the marginal trend.

How Investors Interpret SaaS CAC

Investors use SaaS CAC as a diagnostic input, not as a standalone verdict. A lower CAC can signal efficient acquisition, strong product pull, effective distribution, or a favorable customer segment. It can also reflect underinvestment, early-market demand that may not repeat, or a customer mix with lower contract value.

A higher CAC can signal inefficient sales and marketing spend, heavy competition, long sales cycles, or weak conversion. It can also be reasonable when customers have larger contracts, strong gross margins, high retention, meaningful expansion revenue, and a manageable CAC payback period.

The metric becomes stronger when read beside customer durability. If a company spends heavily to acquire customers who churn quickly, CAC can become a warning sign. If customers stay, expand, and generate high-margin recurring revenue, the same acquisition cost can be easier to justify. That is why SaaS churn rate changes the interpretation of acquisition efficiency.

| CAC reading | What it may suggest | What must be checked before concluding |

|---|---|---|

| Lower CAC | Efficient acquisition, strong organic demand, product-led adoption, or easier customer conversion. | Customer quality, churn, contract value, gross margin, sales motion, and whether the company is underinvesting in growth. |

| Higher CAC | Longer sales cycles, heavier competition, enterprise sales cost, paid-channel dependence, or weaker conversion. | Retention, expansion revenue, payback period, customer lifetime value, and whether larger customers justify the cost. |

| Rising CAC | Acquisition is becoming more expensive or the company is pushing into harder channels or segments. | Whether average contract value, gross retention, net retention, and sales efficiency are improving enough to offset the increase. |

| Falling CAC | Acquisition may be improving or the company may be benefiting from cheaper channels. | Whether the company is still acquiring durable customers, not only smaller or lower-quality accounts. |

Illustrative Scenario: Same CAC, Different Meaning

Two SaaS companies can report the same CAC and still have very different acquisition quality.

| Scenario | Company A | Company B |

|---|---|---|

| Reported CAC | Same as Company B | Same as Company A |

| Customer retention | Customers stay and renew at a high rate. | Customers leave quickly after the first contract or trial period. |

| Payback context | Gross profit can recover acquisition spend within a reasonable operating window. | Acquisition spend takes too long to recover, or may not be recovered before churn. |

| Expansion revenue | Existing customers often add seats, usage, or modules. | Existing customers rarely expand after the initial sale. |

| Investor interpretation | The CAC may support durable recurring revenue if the pattern continues. | The same CAC may signal weak acquisition quality despite the identical headline number. |

The useful lesson is that CAC needs a revenue-quality check. Acquisition cost has more meaning when the customers acquired are retained, profitable, and capable of expanding over time.

Why SaaS CAC Comparisons Can Break

SaaS CAC comparisons can break when two companies use different sales motions, customer segments, cost allocation methods, or timing windows. A product-led company selling monthly self-serve subscriptions may naturally report a different acquisition cost profile than an enterprise SaaS company using account executives, implementation teams, and long procurement cycles.

Segment mix can also change the reading. Enterprise customers may cost more to acquire but produce larger contract values. SMB customers may cost less to acquire but churn faster. B2B, B2C, product-led, sales-led, partner-led, and vertical SaaS models can all produce different CAC patterns without one model being automatically better.

Limitation: CAC should not be compared across SaaS companies unless the period, cost base, customer definition, sales motion, customer segment, and retention profile are close enough to make the comparison meaningful.

Common Mistakes When Reading SaaS CAC

- Counting leads instead of customers: Leads, demos, trials, and signups do not equal new paying customers.

- Mixing periods: Costs and customers should come from the same measurement window, especially when sales cycles are long.

- Ignoring cost allocation: A company may include or exclude different sales and marketing costs, which can change the result.

- Treating lower CAC as automatically better: Low CAC can come from efficient acquisition, but it can also reflect smaller customers, weak investment, or temporary channel advantages.

- Treating higher CAC as automatically worse: High CAC can be acceptable if customers are durable, profitable, and likely to expand.

- Applying benchmark numbers without context: Benchmark comparisons are weak unless the peer set, methodology, period, and customer definitions are aligned.

SaaS CAC and Related Metrics

SaaS CAC becomes more useful when it is connected to the rest of the SaaS metric stack. CAC shows the cost of acquisition, but other metrics show whether the acquired customer base is durable and economically attractive.

CAC payback period shows how long it takes to recover acquisition spend from customer gross profit. Retention and churn show whether the acquired customers stay long enough to matter. LTV/CAC connects acquisition cost with expected customer value, but it depends heavily on retention assumptions and gross margin. Sales efficiency metrics, including the SaaS Magic Number, help connect sales and marketing spend to recurring revenue growth.

Related SaaS metric checks: Use CAC to understand acquisition cost, CAC payback to understand recovery time, churn to understand customer durability, and sales efficiency metrics to understand whether spending is turning into recurring revenue growth.

FAQ

What is SaaS customer acquisition cost?

SaaS customer acquisition cost is the average sales and marketing cost required to acquire a new paying SaaS customer during a defined period.

What is the SaaS CAC formula?

The basic formula is acquisition-related sales and marketing costs divided by new paying customers acquired during the same period.

Is a lower SaaS CAC always better?

No. A lower CAC can be positive, but it must be checked against customer quality, retention, contract value, gross margin, and whether the company is still investing enough to grow.

Why can two SaaS companies have different CAC levels?

CAC can differ because of sales motion, customer segment, pricing model, contract size, sales cycle length, channel mix, and how acquisition costs are allocated.

Should CAC be judged alone?

No. CAC should be read with payback, retention, expansion revenue, gross margin, and revenue quality because acquisition cost alone does not show whether growth is durable.