EBIT, or earnings before interest and taxes, measures a company’s profit before financing costs and income tax effects. Investors use it to compare operating profitability before differences in debt structure and tax position, but the number still needs checks for depreciation, capital spending, working capital, and cash conversion.

Definition: EBIT is a profit measure that starts with earnings and removes the effect of interest expense and income tax expense. It is often used as an operating-profit lens because it focuses on profit before capital structure and tax effects, while still keeping depreciation and amortization inside the result.

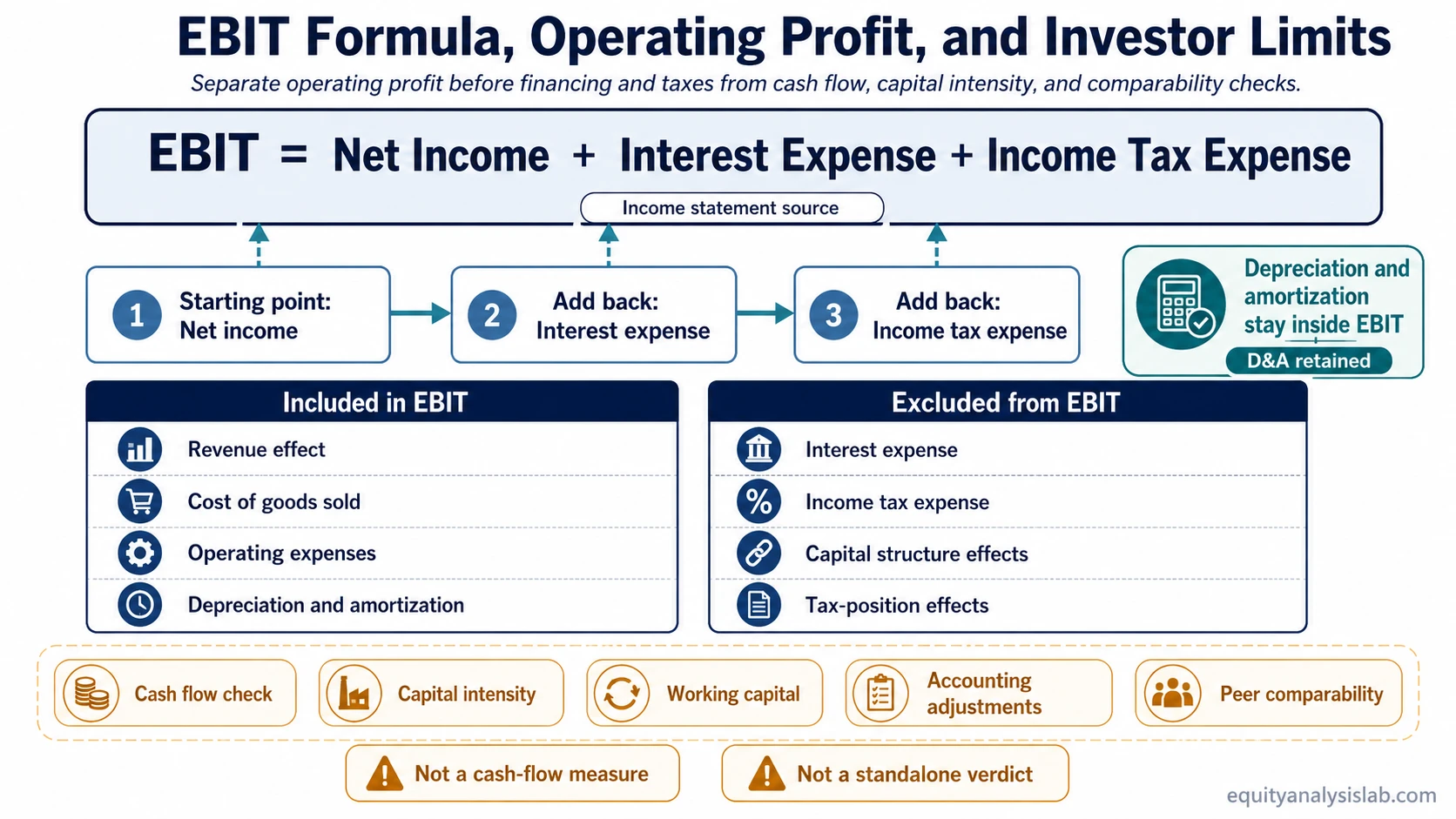

Key points about EBIT

- EBIT means earnings before interest and taxes.

- It can be calculated by adding interest expense and income tax expense back to net income.

- It helps compare operating profit before financing and tax differences.

- It is not the same as net income, EBITDA, or operating cash flow.

- It should be checked against depreciation, capital intensity, working capital, and accounting adjustments.

How EBIT is calculated

The most common EBIT calculation starts from net income and adds back interest expense and income tax expense:

EBIT = Net income + interest expense + income tax expense

It can also be approached from operating results when the reporting structure provides enough detail:

EBIT = Revenue – cost of goods sold – operating expenses

The second version depends on how the company presents expenses, non-operating items, depreciation, amortization, and unusual charges. For that reason, EBIT should be tied back to the company’s reported financial statements rather than treated as a single universal line item.

What EBIT includes and excludes

EBIT sits above interest and income taxes, but it is not the same as a pure cash measure. The most useful first check is whether the inputs are being matched consistently across companies and periods.

| Item | Typical EBIT treatment | Why it matters for investors |

|---|---|---|

| Revenue | Included through operating profit calculation | Sets the starting point for operating profitability. |

| Cost of goods sold | Included | Shows whether gross profit supports the operating base. |

| Operating expenses | Included | Captures selling, administrative, research, and other operating costs when reported that way. |

| Depreciation and amortization | Usually included | Separates EBIT from EBITDA and keeps part of the asset-consumption cost inside profit. |

| Interest expense | Excluded | Removes financing-cost differences between companies. |

| Income taxes | Excluded | Removes tax-position differences before comparing operating profit. |

| Non-operating or unusual items | Depends on the reporting and adjustment method | Can make EBIT less comparable if one-time gains, losses, or adjustments are handled inconsistently. |

Where EBIT comes from in financial statements

EBIT is usually derived from the income statement. Some companies report operating income directly, while others require the analyst to reconcile net income, interest expense, tax expense, and operating items.

The reporting caveat matters because EBIT is not always labeled the same way across companies. One company may disclose a clean operating profit line, while another may require adjustments for non-operating income, restructuring charges, asset sales, or other items that affect comparability.

How investors use EBIT

Investors use EBIT to compare profit generated before financing and tax effects. That can be useful when two companies operate in the same industry but have different debt levels, tax structures, or capital structures.

The measure becomes more useful when it is compared against revenue, peer economics, and reporting quality. For example, the operating margin connects operating profit to sales, which helps show whether EBIT is improving because the business is becoming more efficient or simply because revenue is growing.

Comparable EBIT analysis usually works best inside the same industry, with similar accounting policies, similar asset intensity, and similar business models. A software company, a manufacturer, and a bank can have very different expense structures, so a simple EBIT comparison across sectors can mislead.

EBIT vs EBITDA, net income, and cash flow

EBIT vs EBITDA: EBIT includes depreciation and amortization, while EBITDA adds those charges back. That makes EBITDA less affected by accounting depreciation, but also less sensitive to the cost of using long-lived assets.

EBIT vs net income: Net income includes interest expense and income tax expense. EBIT removes those effects to focus on profit before financing and taxes.

EBIT vs cash flow: EBIT is an accrual profit measure. It does not show cash collected, cash paid, capital expenditures, debt repayment needs, or working-capital movement.

Simple EBIT calculation example

Assume a company reports net income of 80, interest expense of 10, and income tax expense of 20.

EBIT = 80 + 10 + 20 = 110

The EBIT result of 110 shows profit before financing and tax effects. It does not show whether the company generated cash, how much capital spending the business requires, or whether the reported profit came from recurring operations.

Limits and common mistakes

Positive EBIT does not prove business quality. A company can report positive EBIT while still consuming cash through capital expenditures, inventory buildup, customer receivables, or debt service.

EBIT does not remove accounting risk. Revenue recognition, restructuring adjustments, impairment charges, stock-based compensation treatment, and non-recurring items can affect how clean the number is.

EBIT is not a valuation conclusion. A low valuation multiple can look attractive, but the interpretation depends on earnings quality, cyclicality, balance-sheet risk, growth durability, and capital needs.

EBIT comparisons need context. The number is most useful when companies have similar business models, similar accounting treatment, and similar operating economics.

EBIT in valuation context

EBIT connects operating-profit analysis with valuation, but each concept has a different job. The EV/EBIT valuation multiple uses EBIT as part of a valuation comparison, while EBIT itself is only the operating-profit input. The investor still has to check source quality, comparability, capital intensity, and cash conversion before drawing conclusions.

FAQ

Is EBIT the same as operating income?

EBIT and operating income can be close, but they are not always identical. Operating income usually reflects profit from core operations, while EBIT may require adjustments depending on how interest, taxes, and non-operating items are presented.

Is EBIT better than EBITDA?

EBIT is not automatically better than EBITDA. EBIT keeps depreciation and amortization inside the profit measure, while EBITDA removes them. The better measure depends on the business model, asset intensity, and the question being asked.

Does EBIT show cash flow?

No. EBIT is an accrual profit measure, not a cash-flow measure. It does not capture working-capital changes, capital expenditures, debt repayment, or the timing of cash receipts and payments.