Cost of equity is the required return that equity investors demand for taking ownership risk in a company. In valuation work, it is usually an estimated discount-rate input, not a forecast of what the stock will actually return.

The estimate can discipline a valuation model because it forces the analyst to state the equity return requirement explicitly. It can also mislead when the inputs are treated as precise facts, when beta is used mechanically, or when the estimate is confused with business quality.

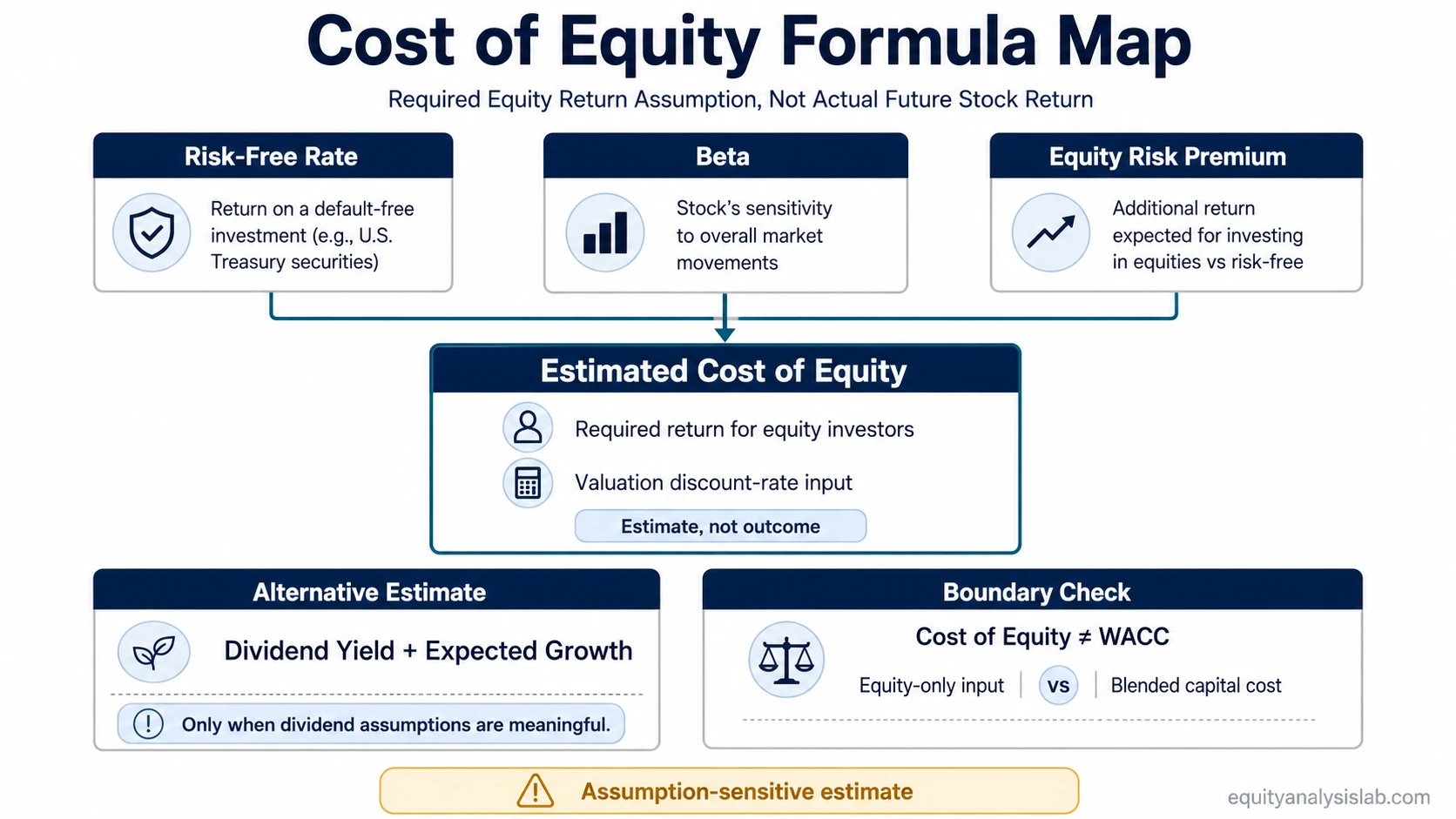

Definition: Cost of equity is the return required by common shareholders for bearing equity risk. Analysts use it as a discount rate for equity cash flows, as an input in valuation models, and as one component of broader capital-cost analysis.

Key Points

- Cost of equity estimates the return equity investors require for ownership risk.

- CAPM is the most common estimation method, but its inputs remain assumptions.

- Dividend-based models can be useful only when dividend and growth assumptions are meaningful.

- Cost of equity is part of broader cost-of-capital analysis, not the same concept as WACC.

- The estimate does not guarantee actual future stock returns or prove that a stock is safe.

What Cost of Equity Means

Cost of equity represents the return shareholders require for owning a company’s equity rather than a lower-risk asset. The rate is not directly quoted like an interest rate on debt, so it must be estimated from assumptions about risk, market returns, dividends, or comparable companies.

The concept is closely related to the required return investors demand, but it is usually applied at the company or equity-valuation level. A higher estimate generally lowers the present value of future equity cash flows, while a lower estimate raises it, all else equal.

The important boundary is that cost of equity is an input, not a verdict. It may shape a valuation model, but it does not prove that a business is high quality, that a stock is undervalued, or that future returns will match the model.

How Cost of Equity Is Estimated

Analysts usually estimate cost of equity with a model rather than observing it directly. The method depends on the company, available data, dividend policy, and the purpose of the valuation.

| Method | Basic idea | Best use | Main limitation |

|---|---|---|---|

| CAPM | Risk-free rate plus beta-adjusted equity risk premium | Public companies with market beta data | Highly sensitive to beta, market premium, and risk-free-rate assumptions |

| Dividend capitalization model | Dividend yield plus expected dividend growth | Stable dividend-paying companies | Weak fit for non-dividend companies or unstable growth assumptions |

| Build-up or proxy approach | Starts with a base return and adds risk premia | Private companies or cases with limited market data | Input selection can become subjective and hard to verify |

The most common public-company method is the capital asset pricing model. It estimates cost of equity as the risk-free rate plus beta multiplied by the equity risk premium.

CAPM Inputs and Formula Logic

The CAPM version of cost of equity is often written as:

Cost of Equity = Risk-Free Rate + Beta × Equity Risk Premium

Risk-free rate: The baseline return assumption, often linked to a government bond yield in the relevant currency. A higher risk-free rate usually raises the cost of equity estimate before company-specific risk is even considered.

Beta: The sensitivity assumption for the stock relative to the broader equity market. A higher beta increases the estimated equity return requirement, but beta is historical and can be unstable across regimes, business changes, and measurement periods.

Equity risk premium: The additional return investors require for owning equities instead of the risk-free asset. This input is not directly observable as a fixed fact, so different analysts may use different assumptions.

Changing any one of these inputs can materially change the estimate without changing the company’s revenue, margins, cash flow, balance sheet, or competitive position. That is why cost of equity should be interpreted as an assumption-sensitive valuation input.

Cost of Equity vs Cost of Capital and WACC

Cost of equity focuses only on the return required by shareholders. The broader cost of capital includes the financing cost of all capital sources, including equity and debt.

| Concept | What it measures | How it differs from cost of equity |

|---|---|---|

| Cost of equity | Required return for common shareholders | Applies to equity holders and equity cash-flow valuation |

| Cost of debt | Borrowing cost for lenders, usually adjusted for tax effects in WACC | Debt has contractual claims, while equity absorbs residual risk |

| WACC | Weighted average cost of equity and debt capital | Blends capital sources according to capital structure |

| Required rate of return | Investor hurdle rate for taking risk | Broader concept that can apply across assets, investors, and decision contexts |

This boundary matters in valuation. Equity cash flows are usually discounted at the cost of equity, while firm-level cash flows are often discounted at WACC. Mixing the two can create valuation errors because the cash-flow type and discount-rate type no longer match.

Simple Cost of Equity Example

A company’s operations can remain unchanged while the estimated cost of equity rises because the risk-free rate, beta assumption, or equity risk premium has moved higher. The CAPM estimate can change even if revenue, margins, and cash flow are the same as before.

That does not automatically make the company better or worse. It means the valuation model is now using a higher required return for equity risk, which can lower the present value assigned to future equity cash flows.

A useful estimate separates business analysis from valuation assumptions. Business quality may come from durable margins, cash generation, reinvestment opportunity, and balance-sheet strength. Cost of equity controls the discount-rate side of the model.

When Cost of Equity Becomes Misleading

Cost of equity becomes less useful when the estimate is treated as a precise market truth. Small changes in beta, the equity risk premium, or the risk-free rate can shift the answer enough to change a valuation conclusion.

Common mistake: Treating cost of equity as a forecast of actual stock returns can create false confidence. The estimate is a required-return assumption inside a model, not a promise that the market will deliver that return.

A useful estimate keeps the valuation assumption visible; a misleading estimate turns model inputs into a false sense of precision.

| Misuse | Why it creates risk | Cleaner interpretation |

|---|---|---|

| Using stale beta | The company’s risk profile or market sensitivity may have changed | Check whether the input still reflects the business and market context |

| Treating CAPM as exact | The model depends on assumptions that cannot be observed perfectly | Use it as one disciplined estimate, not as a final answer |

| Equating high cost of equity with bad business quality | The estimate may reflect market volatility or input choices rather than operations | Separate discount-rate assumptions from company fundamentals |

| Using cost of equity as a buy/sell rule | Valuation still depends on cash flows, growth, balance sheet, and price paid | Use it as one valuation input inside a broader investor process |

Cost of Equity in Valuation Use

Cost of equity is most useful when it makes the valuation assumption visible. A model that uses a low discount rate will usually assign more value to future cash flows than a model that uses a high discount rate. That sensitivity is especially important for long-duration growth companies, cyclical businesses, and companies whose value depends heavily on future cash flows.

The estimate should be read alongside business quality, earnings durability, cash-flow conversion, leverage, reinvestment opportunity, and valuation multiple context. A clean business thesis can still be weakened by unrealistic discount-rate assumptions, and a conservative discount rate cannot fix weak cash-flow assumptions.

The practical distinction is simple: fundamentals define the business case, while cost of equity defines part of the valuation lens applied to that case.

FAQ

Is cost of equity the same as WACC?

No. Cost of equity measures the required return for shareholders only. WACC blends the cost of equity and the cost of debt according to the company’s capital structure.

Why does beta affect cost of equity?

Beta affects cost of equity in CAPM because it adjusts the equity risk premium for the stock’s historical sensitivity to the market. A higher beta usually raises the estimate, but beta is still an assumption.

Does cost of equity predict future stock returns?

No. Cost of equity is a required-return estimate used in valuation work. Actual future stock returns can differ because market price, fundamentals, sentiment, rates, and company results can all change.