Required rate of return is the minimum return an investor requires to justify taking risk in an investment. In equity valuation, it works as a required return assumption for comparing expected cash flows, estimated value, and the return demanded for a given level of risk.

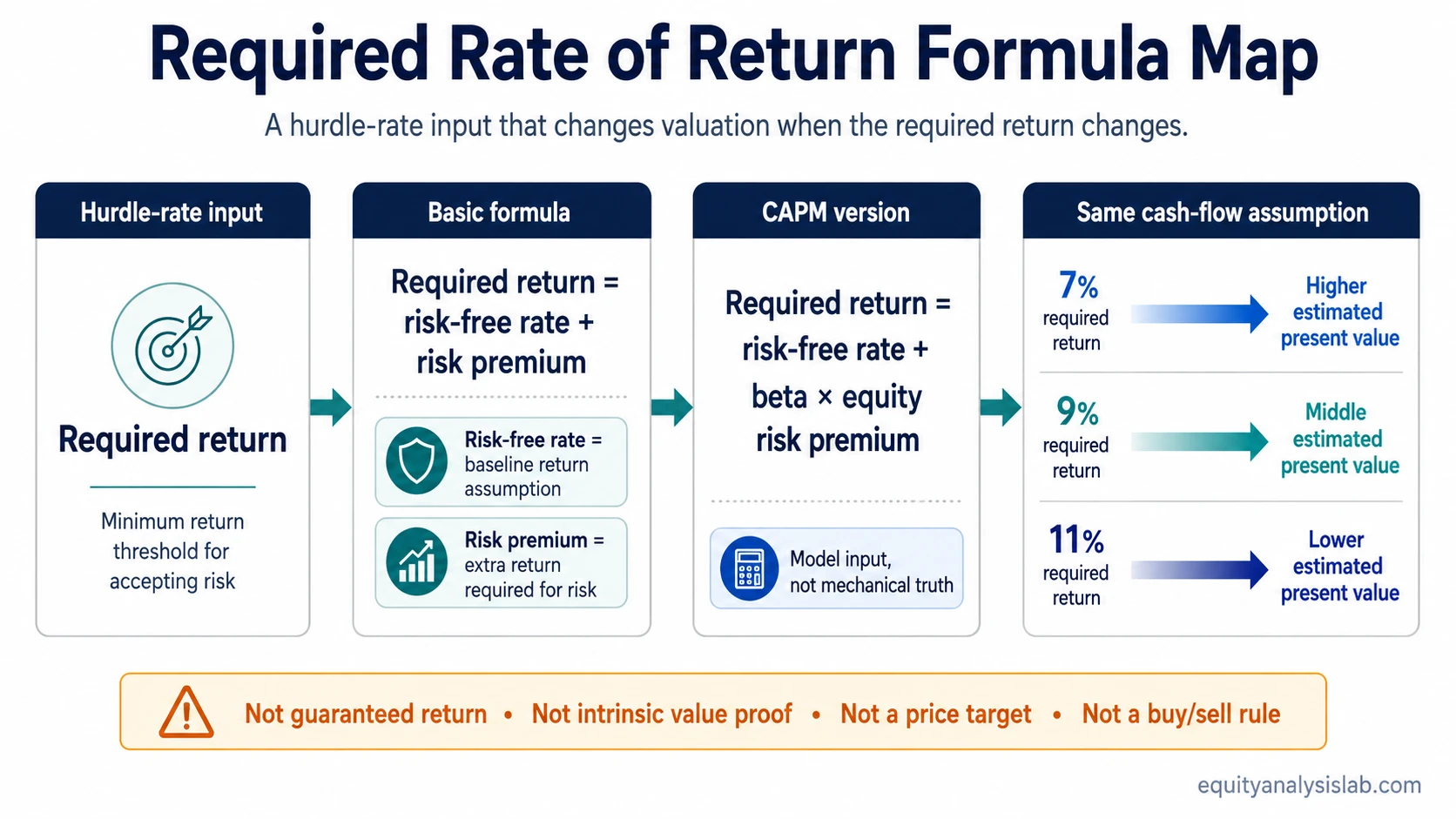

Definition: Required rate of return is the return threshold an investor uses before an investment becomes acceptable on a risk-adjusted basis. It is an input, not a guaranteed return, not proof of intrinsic value, not a price target, and not a buy or sell rule.

For stock analysis, the required rate of return helps translate uncertainty into a valuation assumption. A higher required return usually makes the same expected cash flows less valuable today, while a lower required return usually makes those same expected cash flows more valuable today.

Key Points

- Required rate of return sets the minimum return threshold for taking investment risk.

- In valuation, it often functions as the return assumption used to discount expected future cash flows.

- A higher required return lowers estimated present value when future cash-flow assumptions stay unchanged.

- The number can look precise even when the risk premium, beta, growth, and cash-flow assumptions remain uncertain.

- Required rate of return should not be treated as a guaranteed return, price target, or investment recommendation.

What Is Required Rate of Return?

Required rate of return, often shortened to RRR, is the minimum return an investor demands before accepting the risk of an investment. It is sometimes described as a hurdle rate because the expected return must clear that threshold before the investment appears attractive under the investor’s assumptions.

In equity analysis, RRR is not only a personal preference. It can become a valuation input. When expected cash flows are discounted back to the present, the required return helps determine how much those future cash flows are worth today.

The practical interpretation is simple: higher perceived risk normally requires a higher return threshold. If two companies have the same expected future cash flow but one has more uncertainty, weaker balance-sheet quality, or less durable earnings, an investor may require a higher return to compensate for that risk.

Required Rate of Return Formula

The simplest required rate of return formula combines a risk-free rate with a risk premium:

Required return = risk-free rate + risk premium

The risk-free rate represents the baseline return assumption before taking equity risk. The risk premium represents the extra return required for uncertainty, volatility, business risk, balance-sheet risk, or other investment-specific risks.

In equity valuation, a common model-based version uses the Capital Asset Pricing Model:

Required return = risk-free rate + beta × equity risk premium

In that formula, beta estimates how sensitive the stock is to broad equity market movements. The equity risk premium represents the extra return investors demand for owning equities instead of a lower-risk baseline asset. The formula can be useful, but it should not be treated as mechanical truth. Beta, risk premium, and cash-flow assumptions can all change the final valuation output.

What Required Rate of Return Is and Is Not

Required rate of return is useful because it forces a valuation model to state the return threshold being assumed. It becomes risky when the percentage is treated as a certainty rather than an input.

| It is | It is not |

|---|---|

| A minimum acceptable return assumption | A guaranteed return |

| A valuation input | Proof of intrinsic value |

| A risk-adjusted hurdle | A buy or sell signal |

| A comparison benchmark | A price target |

| A way to reflect uncertainty | A replacement for due diligence |

The most important boundary is that required return does not decide whether a stock is good or bad by itself. It only changes the hurdle that expected cash flows must clear.

How Required Rate of Return Affects Valuation

Required rate of return affects valuation because expected future cash flows are worth less today when the discounting hurdle is higher. If the expected cash-flow assumption stays the same, raising the required return usually lowers the estimated value.

This is why small changes in RRR can create large differences in valuation. A model may look precise because it uses a specific percentage, but that precision can be misleading if the underlying risk premium, growth, and cash-flow assumptions are fragile.

| Required return | Same expected cash-flow assumption | Valuation effect |

|---|---|---|

| 7% | Unchanged | Higher estimated present value |

| 9% | Unchanged | Middle estimated present value |

| 11% | Unchanged | Lower estimated present value |

The same logic matters when terminal assumptions are used. A valuation model can become highly sensitive when the required return is close to the terminal growth rate. In that situation, a small input change can move the valuation output more than the business reality has changed.

Simple Illustrative Example

Illustrative scenario: A hypothetical company is expected to produce the same stream of future cash flows under three valuation cases. Nothing changes in the cash-flow forecast. Only the required return changes.

At a 7% required return, the cash flows receive a higher present value because the hurdle is lower. At a 9% required return, the estimate sits between the lower and higher cases. At an 11% required return, the same expected cash flows receive a lower present value because the investor is demanding more compensation for risk.

The example is not a real valuation, not a historical case, and not a recommendation. Its only purpose is to show directionality: when expected cash flows stay unchanged, a higher required return reduces the value assigned to those cash flows today.

Required Rate of Return vs Nearby Concepts

Required rate of return is often confused with discount rate, WACC, cost of capital, expected return, and IRR. These concepts overlap, but they do not mean the same thing in every valuation context.

| Concept | How it differs from required rate of return |

|---|---|

| Discount rate | The discount rate is the rate used to convert future cash flows into present value. Required return can be used as a discount rate, but the terms are not always interchangeable in every model. |

| WACC | Weighted average cost of capital reflects the blended cost of debt and equity capital for the business. Required return may refer specifically to the equity investor’s return threshold. |

| Cost of capital | Cost of capital describes the return demanded by capital providers. Required return is usually the investor-facing hurdle used to decide whether the risk is adequately compensated. |

| Expected return | Expected return is what the investor estimates the investment may produce. Required return is the minimum return the investor demands before the investment is acceptable under the assumptions. |

| IRR | Internal rate of return is the return implied by a set of cash flows and price assumptions. Required return is the hurdle used to judge whether that implied return is sufficient. |

The clean distinction is hurdle versus estimate. Required return is the hurdle. Expected return or IRR is the estimate being compared against that hurdle.

Limitations of Required Rate of Return

Main limitation: Required rate of return can look precise while the assumption stack remains fragile. A model using 9.2% may appear more exact than a model using 9%, but the extra decimal does not remove uncertainty in the business, cash flows, risk premium, or growth assumptions.

Risk premium inputs can be subjective. Two investors can look at the same company and require different returns because they assess durability, cyclicality, leverage, management quality, or opportunity cost differently.

Beta can also miss important business risk. A stock may have a measured beta that looks moderate while the company still faces customer concentration, margin pressure, refinancing risk, or weakening competitive position.

Growth and cash-flow assumptions may dominate the result. A clean required-return estimate does not fix an unrealistic cash-flow forecast. It also does not replace balance-sheet analysis, earnings quality review, or business model judgment.

Required return can support a margin of safety process, but it does not prove that a margin exists. The valuation output still depends on the full assumption stack.

Related Concepts

Required rate of return connects to several nearby valuation concepts. Each one answers a different part of the valuation question.

| Concept | Why it matters |

|---|---|

| market capitalization | Market capitalization shows the market value assigned to common equity, while required return helps frame the return threshold behind a valuation assumption. |

| Discount rate | Discount rate is the model input that converts future cash flows into present value. |

| Terminal growth rate | Terminal growth rate affects the long-term cash-flow assumption that interacts with the required return. |

| Margin of safety | Margin of safety compares estimated value against market price while recognizing that valuation assumptions can be wrong. |

| Capital Asset Pricing Model | CAPM is one common method for estimating an equity required return from a risk-free rate, beta, and equity risk premium. |

FAQ

Is required rate of return the same as discount rate?

Not always. Required rate of return can be used as a discount rate in valuation, but discount rate is the model input used to convert future cash flows into present value. Required return is the investor’s hurdle for accepting risk.

Does required rate of return guarantee the investor will earn that return?

No. Required rate of return is a threshold or assumption. Actual returns depend on price paid, business performance, market conditions, and whether the underlying assumptions prove reasonable.

Why does a higher required return lower valuation?

A higher required return discounts future cash flows more heavily. When the cash-flow forecast stays the same, a higher return hurdle gives those future cash flows a lower present value.

Can two investors use different required rates of return for the same stock?

Yes. Investors may use different required returns because they have different risk tolerance, opportunity costs, assumptions about the business, and views of uncertainty.