Terminal growth rate is the steady long-term growth assumption applied to cash flows after the explicit forecast period in a valuation model. It helps estimate terminal value, but it is an assumption for valuation review, not a guarantee of future company growth.

Definition: Terminal growth rate is the perpetual or steady-state growth rate used after a forecast period when a valuation model assumes the business has reached a more mature, normalized growth phase.

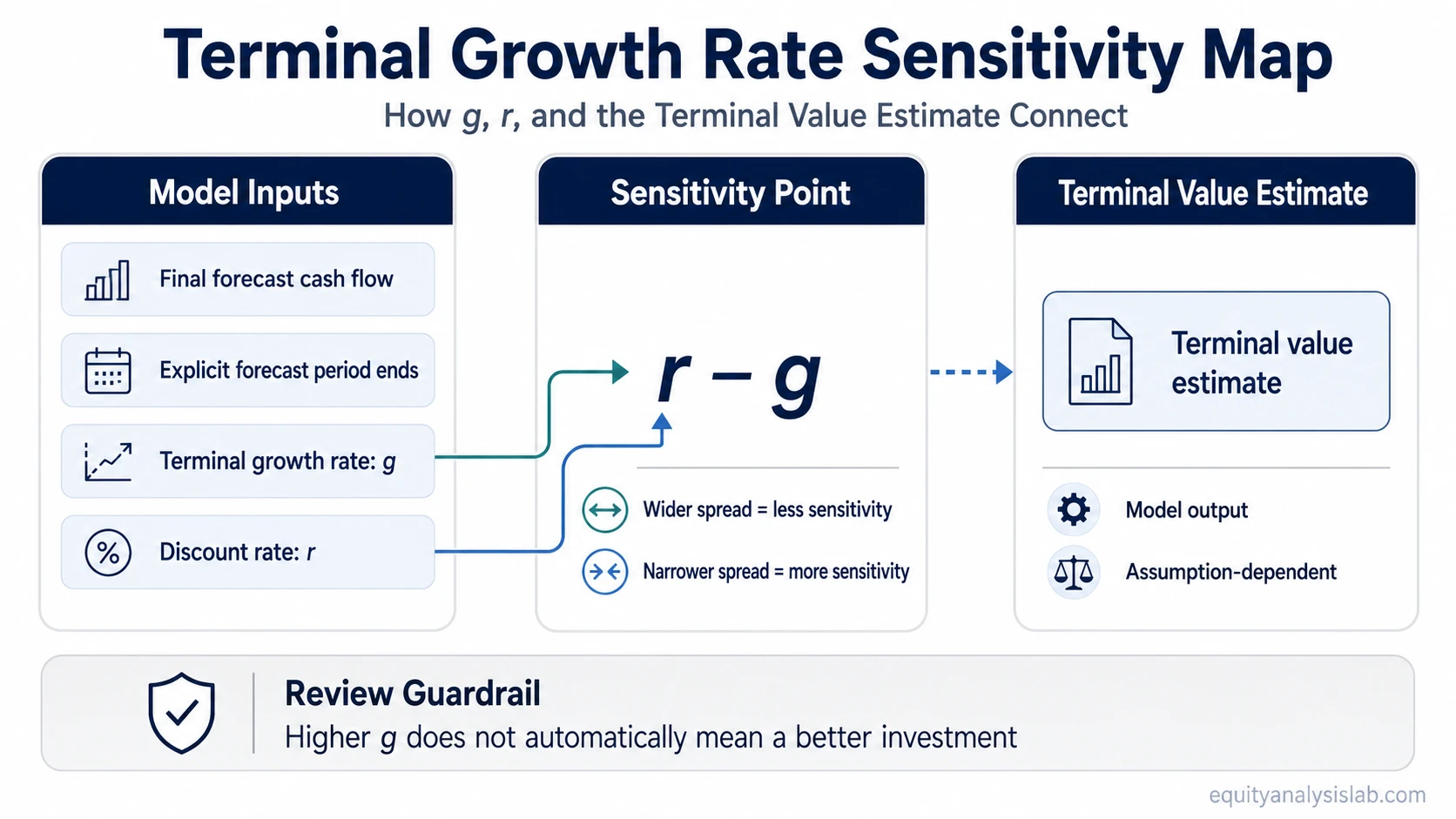

The assumption matters because it changes the denominator in the perpetuity-growth formula. A small change in g can produce a much larger change in terminal value, especially when the spread between the discount rate and terminal growth rate is narrow.

For that reason, terminal growth rate should be reviewed together with the cash-flow base, the length of the explicit forecast period, the discount rate, and the durability of the business economics behind the model.

Key Points

- Terminal growth rate is a long-term valuation assumption used after the explicit forecast period.

- It is commonly used in DCF models to estimate terminal value under a perpetuity-growth approach.

- The formula is highly sensitive when the discount rate or WACC is close to the growth rate.

- A higher terminal growth rate does not automatically mean a better investment; it may only mean the model is using a more aggressive assumption.

- The assumption should be checked against business maturity, reinvestment needs, industry structure, inflation context, and long-term economic plausibility.

What Terminal Growth Rate Means

Terminal growth rate represents the growth assumption used after detailed year-by-year forecasts end. Instead of forecasting cash flow for every future year, the model assumes that cash flows grow at a stable rate beyond the explicit forecast window.

This is why the assumption belongs to valuation mechanics rather than short-term forecasting. It does not say what next quarter, next year, or the next market cycle will look like. It tries to simplify the long tail of future cash flows into one steady-state assumption.

Useful boundary: Terminal growth rate is the growth assumption. The related terminal value estimate is the output affected by that assumption.

Terminal Growth Rate Formula

In a perpetuity-growth terminal value model, terminal growth rate is usually shown as g. The simplified formula is:

Terminal Value = FCFn × (1 + g) / (r − g)

| Formula item | What it means | Why it matters |

|---|---|---|

| FCFn | The final forecast-period free cash flow before applying the terminal growth rate | A weak or inflated cash-flow base can distort the terminal value before the growth rate is even applied. |

| g | The terminal growth rate | A higher g increases the terminal value estimate, but only if the long-term assumption is credible. |

| r | The discount rate used in the model, often WACC in an enterprise-value DCF | The spread between the discount rate and g controls much of the formula’s sensitivity. |

The formula becomes unstable if the terminal growth rate gets too close to the discount rate. The model may still calculate a number, but the result can become more dependent on assumption choice than on business reality.

How Terminal Growth Rate Affects Terminal Value

Terminal growth rate affects terminal value through the denominator spread: discount rate minus terminal growth rate. When the growth assumption rises, the denominator becomes smaller and the terminal value estimate increases.

That relationship is powerful because terminal value can represent a large part of a DCF model’s total estimated value. The exact share depends on the company, forecast period, discount rate, cash-flow profile, and model design, so it should not be treated as one fixed percentage.

Assumption stack: cash-flow base → explicit forecast period → steady-state growth assumption → discount rate / WACC spread → terminal value estimate → present-value discounting.

The terminal growth rate therefore works as one link in a valuation stack. It should not be reviewed in isolation from the required rate of return, reinvestment needs, or the company’s ability to sustain cash generation.

Why Small Changes in Terminal Growth Rate Matter

A small terminal growth rate change can produce a large valuation change because the formula magnifies the difference between the discount rate and the growth rate. This is especially important when the model uses a mature-company cash-flow base and a long forecast horizon.

| Terminal growth assumption | Directional effect on terminal value | Interpretation risk |

|---|---|---|

| Lower growth case | Lower terminal value estimate | May be conservative, but could understate value if durable growth is still realistic. |

| Base growth case | Middle valuation estimate | Useful as a reference point, but still depends on the cash-flow base and discount rate. |

| Higher growth case | Higher terminal value estimate | Can make the model look attractive even when the long-term assumption is not well supported. |

A simple hypothetical example shows the sensitivity. If the same cash-flow base is valued with a 9% discount rate, moving the terminal growth assumption from 2% to 3% narrows the denominator from 7% to 6%. That does not prove the business is more valuable; it only shows that the valuation output is highly exposed to the growth assumption.

What Makes a Terminal Growth Rate Reasonable

A reasonable terminal growth rate depends on what the model is assuming about the company after the forecast period. Mature businesses usually need a more restrained steady-state assumption than early high-growth forecasts, because terminal growth is meant to represent a durable long-term phase.

The assumption becomes more credible when it is consistent with normalized margins, reinvestment needs, competitive position, industry maturity, capital intensity, and long-term economic context. It becomes weaker when the model uses high perpetual growth to justify a valuation that the business economics do not support.

Limitation: A terminal growth rate should not be reduced to a mechanical rule such as “always below GDP” or “acceptable because the spreadsheet calculates it.” The assumption needs economic support, and the model should show sensitivity around it.

A useful review asks whether the company can keep growing cash flows without requiring unrealistic reinvestment, margin expansion, market share gains, or pricing power. If those supporting assumptions are weak, a high terminal growth rate can create false precision.

Terminal Growth Rate vs Terminal Value

Terminal growth rate and terminal value are related, but they are not the same thing. Terminal growth rate is the input. Terminal value is the estimated value of cash flows beyond the explicit forecast period.

Terminal growth rate: the steady long-term growth assumption used in the formula.

Terminal value: the valuation output produced by applying the cash-flow base, growth assumption, and discount rate.

The distinction matters because changing the growth assumption changes the terminal value estimate. If a model’s valuation conclusion depends heavily on a small increase in terminal growth rate, the conclusion should be treated as sensitive rather than definitive.

Common Mistakes When Using Terminal Growth Rate

| Mistake | Why it creates risk | Cleaner review question |

|---|---|---|

| Treating g as a precise forecast | The assumption compresses a long future period into one rate. | What range of terminal growth assumptions produces a still-credible valuation? |

| Using high growth to force upside | The model may become assumption-driven rather than business-driven. | Does the company’s long-term economics support that steady-state growth? |

| Ignoring the discount-rate spread | A narrow spread can sharply inflate terminal value. | How sensitive is the result when the discount rate or WACC changes? |

| Confusing terminal growth rate with terminal value | The input and output can be discussed as if they were the same. | Which assumption changed, and how much did it move the valuation output? |

The safest use is not to choose one terminal growth rate and defend it as exact. A better process is to test a range, check whether the assumptions remain economically plausible, and identify whether the investment case depends on the most aggressive version.

FAQ

What is terminal growth rate?

Terminal growth rate is the steady long-term growth assumption applied to cash flows after the explicit forecast period in a valuation model.

What is the terminal growth rate formula?

In a perpetuity-growth terminal value model, the formula is Terminal Value = FCFn × (1 + g) / (r − g), where FCFn is final forecast-period free cash flow, g is terminal growth rate, and r is the discount rate.

Is a higher terminal growth rate always better?

No. A higher terminal growth rate increases the valuation estimate, but it can also make the model less credible if the long-term growth assumption is not supported by the business economics.

How is terminal growth rate different from terminal value?

Terminal growth rate is the input assumption. Terminal value is the estimated value of cash flows beyond the explicit forecast period that is affected by that assumption.