Market capitalization is the market value of a public company’s common equity. It is calculated by multiplying the current share price by shares outstanding. The result is useful for company-size context and valuation comparison, but it is not intrinsic value, enterprise value, or a standalone investment conclusion.

Key Points

- Market capitalization measures what the equity market currently assigns to a company’s common equity.

- The formula is share price multiplied by shares outstanding.

- Market cap can change because the share price changes, because the share count changes, or because both inputs change.

- It helps frame company size, peer comparison, and valuation context, but it does not prove business quality or undervaluation.

- Investors usually need other concepts to interpret market cap, including balance sheet structure, cash flow, valuation assumptions, and estimated value.

What Market Capitalization Means

Market capitalization, often shortened to market cap, is the public market’s current pricing of a company’s common equity. It is an observable market value, not a private estimate of what the business is worth.

A company with a higher market cap is being assigned a larger total equity value by the market than a company with a lower market cap. That does not automatically mean the larger company is better, safer, more profitable, or more attractively valued. It only means the market price of the common equity, multiplied across the relevant share count, is larger.

Market cap can look precise while still being only a market-price output. It changes whenever price changes, and it can also change when the share count changes through issuance, buybacks, conversions, or other share-structure events.

Market Cap Formula

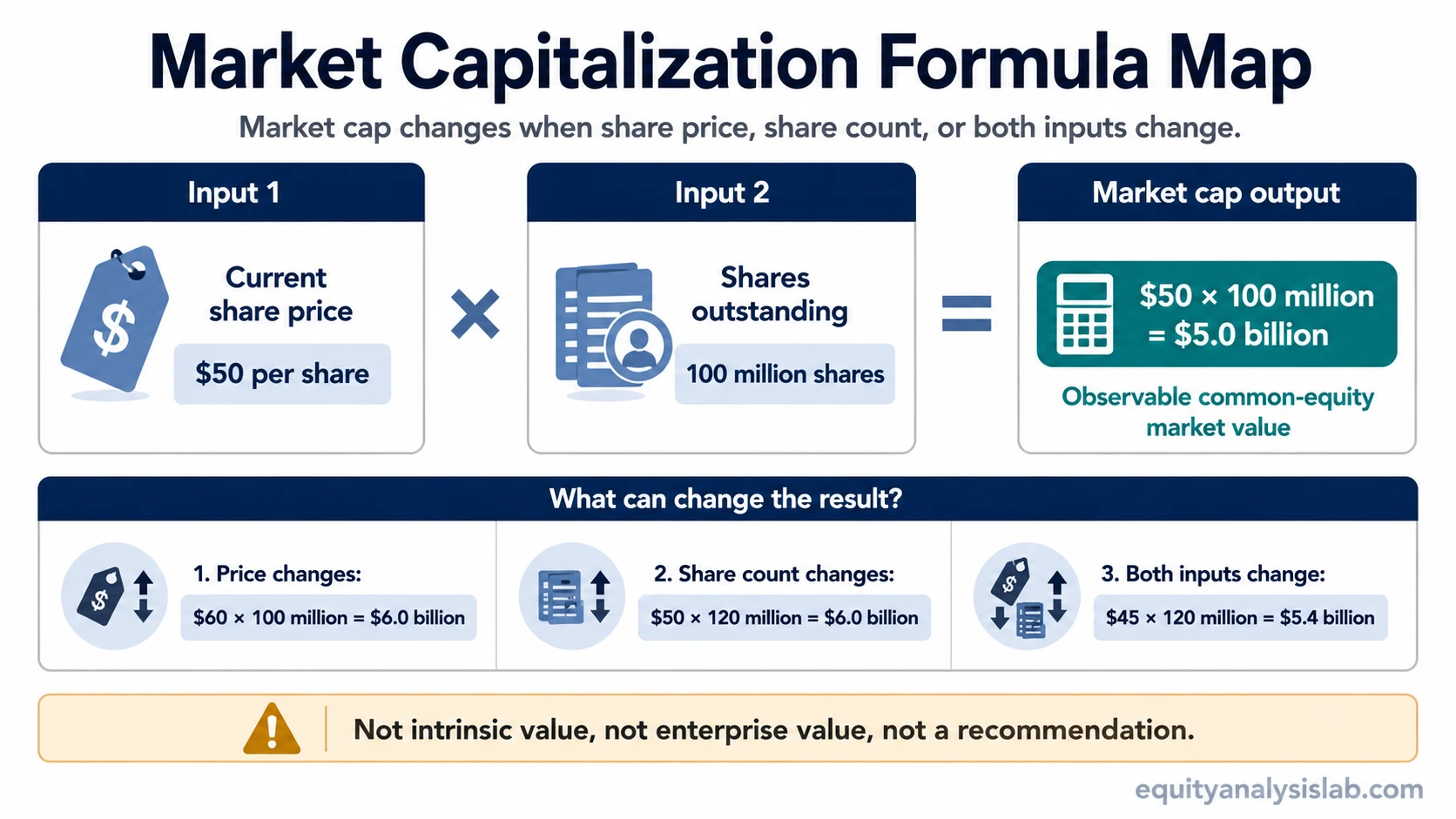

Market capitalization = current share price × shares outstanding

The share price is the current market price for one common share. Shares outstanding are the common shares currently counted as outstanding for the company. Multiplying those two inputs gives the total market value assigned to common equity.

For a simple example, if a company trades at $50 per share and has 100 million shares outstanding, its market capitalization is $5.0 billion.

Simple Calculation Example

A company with a $50 share price and 100 million shares outstanding has a market cap of $5.0 billion because $50 × 100 million equals $5.0 billion. If the share price rises to $60 while the share count stays the same, market cap rises to $6.0 billion. If the share price stays at $50 but the share count rises to 120 million, market cap also rises to $6.0 billion.

Why Share Count Changes Matter

Market cap is not only a price story. A company can have a larger market cap because its share price rises, because its share count increases, or because both inputs move together. The share base behind the calculation matters for interpreting the result.

Share-count changes are especially important when a company has convertible securities, stock-based compensation, warrants, or other potential sources of dilution. In those cases, diluted shares outstanding can help investors think about how the share base may look if potential shares become common shares.

| Scenario | Share price | Shares outstanding | Market cap | What changed |

|---|---|---|---|---|

| Base | $50 | 100 million | $5.0 billion | Starting point |

| Price rises | $60 | 100 million | $6.0 billion | Price changed |

| Share count rises | $50 | 120 million | $6.0 billion | Share count changed |

| Price falls, share count rises | $45 | 120 million | $5.4 billion | Both inputs changed |

Input-level interpretation matters. The same market cap can come from a higher price on the same share count or the same price on a larger share count. Those situations can mean different things for per-share value, dilution, and investor ownership.

What Market Cap Does Not Show

Market cap does not show the value of the operating business by itself because it does not adjust for debt, cash, preferred stock, minority interest, or other capital-structure items. It also does not show whether the market price is above or below a reasonable estimate of business value.

It also does not prove investment quality. A large market cap can reflect durable earnings power, broad investor confidence, index inclusion, or high expectations. It can also reflect an expensive price relative to future cash flows. A small market cap can reflect neglect or opportunity, but it can also reflect weak business quality, financial stress, dilution risk, or limited earnings durability.

The sharper question is what the current market value implies relative to fundamentals, share count, capital structure, and valuation assumptions.

Market Cap Compared With Nearby Valuation Concepts

Market cap is often confused with other valuation terms because several concepts describe value from different angles. The differences matter because each concept answers a different question.

| Concept | What it measures | What it does not measure | Investor use |

|---|---|---|---|

| Market capitalization | Current market value of common equity | Debt-adjusted operating value or estimated fair value | Company-size context, equity-market comparison, valuation starting point |

| Enterprise value | Capital-structure-adjusted value of the operating enterprise | Common-equity market value alone | Comparing businesses with different debt and cash positions |

| Equity value | Value attributable to equity holders, depending on context and method | Always the same thing as market cap in every valuation context | Connecting valuation outputs to per-share equity value |

| Intrinsic value | An estimated value based on assumptions about cash flows, growth, risk, and returns | An observable market price or guaranteed true value | Comparing market price with an investor’s valuation estimate |

Market cap is observable. Intrinsic value is estimated. Enterprise value adjusts market cap for capital structure. Equity value depends on whether the context is public market value, transaction value, or a valuation output. Mixing these concepts can lead to poor comparisons.

How Investors Use Market Cap in Valuation

Market cap is often the first market-based reference point in equity valuation. It tells investors what the public market is currently assigning to the company’s common equity before they compare that market value with fundamentals.

A valuation process may then compare market cap with earnings, free cash flow, revenue, book value, or estimated future cash flows. The interpretation depends on assumptions such as the discount rate, required rate of return, and terminal growth rate. Market cap alone does not answer those questions.

When value is estimated separately from market price, the gap between the estimate and the market price can become part of margin of safety analysis. That does not turn market cap into a price target. It only makes market cap one observable input in a broader valuation comparison.

Common Market Cap Mistakes

Mistake 1: Treating market cap as true value. Market cap is a market price output. It can be above, below, or near an investor’s estimate of value.

Mistake 2: Comparing market cap without checking capital structure. Two companies with similar market caps can have very different debt, cash, and enterprise values.

Mistake 3: Ignoring share-count changes. A rising market cap can come from a higher share price, a larger share count, or both. Per-share interpretation changes when dilution or buybacks are involved.

Mistake 4: Using size as a shortcut for quality. A large company can still be overvalued, and a small company can still be financially weak. Size and value are different questions.

Mistake 5: Confusing market price with value estimate. Price vs value matters because market cap is built from price, while valuation work estimates what the equity may be worth under a set of assumptions.

Market Cap Categories Are Only a Starting Point

Companies are often grouped broadly into large-cap, mid-cap, and small-cap categories. These labels can help organize a market universe, but they should not be treated as valuation conclusions.

A category can describe size, liquidity, index relevance, or investor familiarity. It does not automatically describe earnings quality, balance-sheet strength, competitive advantage, valuation risk, or expected return. Those require separate analysis.

Free-Float Market Cap Note

Some indexes and data providers use free-float market capitalization, which focuses on shares available for public trading rather than all shares outstanding. That can matter when insiders, governments, founders, or strategic holders own a large portion of the company.

Free-float market cap is useful for index construction and tradable-share analysis, but it should not replace the basic concept. Standard market cap still begins with share price multiplied by shares outstanding.

Related Valuation Concepts

Capital structure changes the comparison between market cap and operating-business value. The distinction is covered in enterprise value vs market cap. Public market value and valuation-context equity value are separated in market cap vs equity value.

Market cap works best as a starting point. It becomes more useful when it is connected to business quality, cash flow, share count, capital structure, and valuation assumptions.

FAQ

Is market capitalization the same as company value?

No. Market capitalization measures the market value of common equity. It does not adjust for debt, cash, preferred stock, or other capital-structure items, and it does not estimate intrinsic value.

Can market cap change if the share price does not change?

Yes. Market cap can change if the share count changes. Share issuance, buybacks, conversions, or other share-structure events can change the market cap calculation even when the share price is unchanged.

Does a larger market cap mean a better investment?

No. A larger market cap means the market assigns a larger total value to the company’s common equity. It does not prove business quality, undervaluation, lower risk, or better future returns.