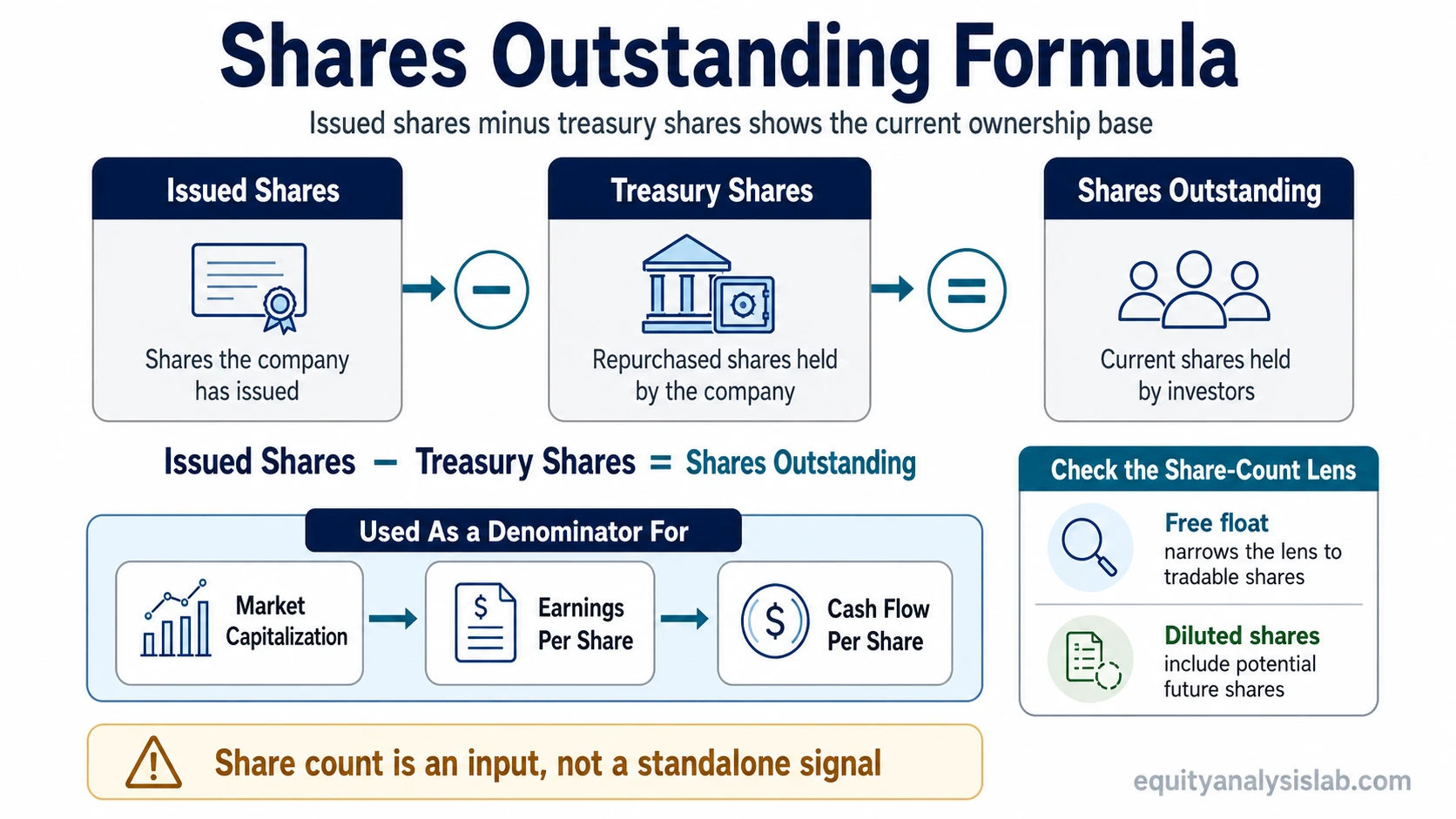

Shares outstanding are the shares currently held by investors, excluding treasury shares held by the company. They represent the current ownership base used in market capitalization, earnings per share, cash-flow-per-share, and other per-share analysis.

For investors, the number matters because it defines how a company’s value, earnings, cash flow, and ownership are spread across shareholders. A company can have the same business value but a different per-share picture if the share count changes.

What Shares Outstanding Means

Shares outstanding are the issued shares that remain in the hands of shareholders. They normally include shares held by public investors, insiders, institutions, and other shareholders, but they exclude shares the company has repurchased and holds as treasury stock.

In plain terms, shares outstanding answer one question: how many shares currently divide the company’s ownership base?

Key Points About Shares Outstanding

- Shares outstanding are the shares currently held by investors, excluding treasury shares.

- The figure can change when a company issues shares, repurchases shares, retires shares, or completes a stock split.

- Investors use shares outstanding in market capitalization and per-share metrics such as earnings per share.

- Shares outstanding are different from free float and diluted shares outstanding.

- The number is an input, not a standalone signal of business quality, valuation, liquidity, or future returns.

What Shares Outstanding Includes and Excludes

Shares outstanding include shares that have been issued and are still held by shareholders. That can include common shares held by public investors, company insiders, institutions, employees, founders, and strategic holders.

Shares outstanding exclude shares held by the company itself as treasury stock. Treasury shares were issued at some point, but they are not currently treated as part of the outside shareholder ownership base while the company holds them.

| Share category | Included in shares outstanding? | Why it matters |

|---|---|---|

| Shares held by public investors | Yes | They are part of the current ownership base. |

| Shares held by insiders or institutions | Yes | They are still shareholder-owned shares, even if they are not actively traded. |

| Treasury shares held by the company | No | They are not counted as currently outstanding while held by the company. |

| Potential shares from options, warrants, or convertibles | Not in basic shares outstanding | They may matter in diluted analysis if they can become common shares. |

Shares Outstanding Formula

A compact way to express the relationship is:

Shares Outstanding = Issued Shares − Treasury Shares

This formula separates shares that have been issued from shares that remain outside the company’s own treasury. If a company repurchases shares and holds them as treasury shares, the outstanding share count can fall. If it issues additional shares, the outstanding share count can rise.

The formula is useful as a boundary, but investors should still check the company filing or data source being used. Some sources may present basic shares, weighted-average shares, diluted shares, or class-specific share counts in different places.

Where Investors Find Shares Outstanding

Investors usually find shares outstanding in a company’s annual report, quarterly report, investor relations materials, or financial data platforms. The exact label can vary, so the safest approach is to check what the number represents before using it in analysis.

| Source | What to check | Common issue |

|---|---|---|

| Annual report or 10-K | Common shares outstanding, weighted-average shares, and share-class notes | The filing may show several share-count figures for different accounting purposes. |

| Quarterly report or 10-Q | Recent share count and changes from issuance or repurchases | The latest quarter may differ from the annual figure. |

| Investor relations page | Capitalization, buyback updates, or share-count disclosures | Presentation figures should be matched against formal filings when precision matters. |

| Financial data provider | Whether the provider uses basic, diluted, weighted-average, or latest shares | Different providers may use different share-count definitions. |

The important habit is not only finding a share count, but identifying which share count the source is using. Latest share counts and weighted-average share counts can answer different questions, so they should not be treated as interchangeable.

How Shares Outstanding Changes

Shares outstanding can change when a company alters its share base. The main mechanisms are issuance, repurchases, treasury-share treatment, share retirement, and stock splits.

| Event | Typical effect on shares outstanding | Investor interpretation |

|---|---|---|

| New share issuance | Can increase the share count | May reduce each existing share’s ownership percentage unless offset by business value created from the capital raised. |

| Share repurchase | Can reduce the share count if shares are retired or held outside the outstanding base | May increase each remaining share’s ownership percentage, but value creation depends on price paid, business quality, and capital allocation. |

| Stock split | Increases the number of shares while proportionally adjusting per-share price | Usually changes the unit count, not the investor’s proportional ownership by itself. |

| Reverse stock split | Reduces the number of shares while proportionally adjusting per-share price | Usually changes the unit count, not the total ownership percentage by itself. |

| Conversion of securities | Can increase common shares if securities convert into stock | Requires attention to dilutive securities and potential future share count. |

A higher or lower share count is not automatically good or bad. The interpretation depends on why the count changed, what the company received or spent, and how the change affects each shareholder’s claim on the business.

How Investors Use Shares Outstanding

Shares outstanding are used as a denominator in several common equity-analysis calculations. The number helps translate company-level value or profit into per-share terms.

| Use case | How shares outstanding are used | What investors should check |

|---|---|---|

| Market capitalization | Share price multiplied by shares outstanding | Whether the share count is current and matches the market-cap calculation. |

| Earnings per share | Net income divided by a share-count denominator | Whether the figure uses basic, diluted, or weighted-average shares. |

| Cash flow per share | Cash flow divided by shares outstanding or a related average share count | Whether share-count changes distort the per-share comparison. |

| Ownership percentage | Investor shares divided by total shares outstanding | Whether issuance, repurchases, or conversions changed the ownership base. |

The practical use is simple: company-level numbers describe the business, while per-share numbers describe how much of that business is represented by each share.

Simple Ownership Example

Suppose an investor owns 1,000 shares and the company has 10 million shares outstanding. That holding represents 0.01% of the company’s outstanding share base.

If the investor still owns 1,000 shares but the company later has 12 million shares outstanding, the same holding represents about 0.0083% of the outstanding share base. The example shows the ownership-base mechanism. It does not mean the share-count change was automatically good or bad.

Shares Outstanding vs Related Share Counts

Shares outstanding are one share-count lens. Investors often need nearby concepts, but each one answers a different analytical question.

| Concept | Main question answered | How it differs from shares outstanding |

|---|---|---|

| Shares outstanding | How many shares are currently held by shareholders? | It is the current ownership base excluding treasury shares. |

| Free float | How many shares are normally available for public trading? | It narrows the view to tradable shares and may exclude insider, locked-up, or strategic holdings. |

| Diluted shares outstanding | What could the share count look like if potential shares became common shares? | It includes possible dilution from instruments such as options, warrants, and convertibles when relevant. |

| Treasury stock | How many shares are held by the company itself? | Treasury shares are excluded from the outstanding share count while held by the company. |

The boundary matters because the wrong denominator can distort analysis. A liquidity question may need float. A dilution question may need diluted shares. A current ownership-base question usually starts with shares outstanding.

Common Mistakes and Limitations

Mistake: treating shares outstanding as a valuation signal by itself. A share count does not say whether a company is cheap, expensive, high quality, or low quality. It only tells you how the ownership base is divided.

Mistake: assuming issuance is always bad or buybacks are always good. Issuance can be useful if the capital creates more value than the ownership cost. Buybacks can be useful or wasteful depending on price, business quality, balance-sheet condition, and opportunity cost.

Mistake: comparing per-share figures without checking the denominator. EPS, cash flow per share, and valuation ratios can change because the business changed, because the share count changed, or because both changed.

Mistake: confusing outstanding shares with float. Shares outstanding measure the current ownership base. Float focuses on shares normally available for public trading.

Mistake: ignoring potential dilution. Basic shares outstanding may not show what happens if options, warrants, convertibles, or other instruments become common shares.

When Shares Outstanding May Be the Wrong Number to Use

Shares outstanding may be the wrong denominator for questions about potential dilution, public tradability, or average share count during a reporting period.

- Use diluted shares when the analysis is about how potential conversion could affect the common share base.

- Use float when the analysis is about how many shares are normally available for trading in the public market.

- Use weighted-average shares when the calculation is tied to an income-statement period such as EPS.

- Use class-specific share counts when a company has multiple share classes with different rights or economics.

The best share count depends on the analytical question. The number should match the decision being made.

FAQ

Is shares outstanding the same as float?

No. Shares outstanding measure the current shares held by shareholders. Float is narrower because it focuses on shares normally available for public trading.

Are treasury shares included in shares outstanding?

No. Treasury shares are held by the company itself and are excluded from shares outstanding while they remain in treasury.

Is shares outstanding the same as diluted shares outstanding?

No. Shares outstanding describe the current share base. Diluted shares outstanding estimate the share base after including potential shares from instruments such as options, warrants, or convertibles when they are relevant.

Where can investors find shares outstanding?

Investors can usually find share-count information in annual reports, quarterly reports, investor relations materials, and financial data platforms. They should check whether the source is showing basic, diluted, weighted-average, or latest shares.

Related Share-Structure Concepts

Use shares outstanding for the current ownership base. Use diluted shares for potential expansion of that base. Use float for public tradability.

- Diluted shares outstanding explains the potential share count after dilutive instruments are considered.

- Free float explains the share count normally available for public trading.

- Share dilution explains how ownership percentage can change when the share base expands.