Treasury stock is a company’s own previously issued stock that it has repurchased and holds instead of leaving it outstanding. It is still issued, but it is not counted as outstanding while held by the company.

Definition: Treasury stock, also called treasury shares or reacquired stock, is stock that was issued to shareholders, bought back by the issuing company, and then held by that company instead of being retired immediately.

The boundary matters because treasury stock sits between two share-count ideas. It remains part of the issued share base, but it is excluded from outstanding shares while the company holds it. That makes treasury stock relevant for ownership percentages, per-share metrics, and the way investors read a company’s share structure.

Key Points

- Treasury stock is repurchased company stock held by the issuing company.

- It is issued, but it is not outstanding while held as treasury stock.

- It usually reduces the outstanding share count while the company continues to hold those shares.

- Treasury stock generally does not carry voting rights or receive dividends while held by the company.

- Treasury stock does not prove that a buyback was cheap, high quality, or shareholder-friendly by itself.

What Treasury Stock Means

Treasury stock begins with a share repurchase. A company has issued shares into the market, later buys back some of those shares, and holds them as treasury shares. The shares have not disappeared from the issued-share history, but they are no longer part of the current shareholder base while they are held by the company.

This is why treasury stock is not the same thing as simply “fewer shares ever issued.” The company may still report issued shares, treasury shares, and outstanding shares as different numbers. Treasury stock is the portion that separates the broader issued base from the narrower current ownership base.

Boundary: A buyback is the transaction that can create treasury stock. Treasury stock is the status of the repurchased shares after the company holds them.

Treasury Stock vs Outstanding Shares

The most important distinction is that treasury stock is issued but not outstanding. Outstanding shares are the shares currently held by outside shareholders and used in many ownership and per-share calculations. Treasury shares are held by the company itself, so they are excluded from that current outside-shareholder base.

| Concept | What it includes | How treasury stock affects it |

|---|---|---|

| Issued shares | Shares the company has issued historically, including shares later reacquired unless retired | Treasury stock can remain inside issued shares |

| Treasury stock | Issued shares repurchased and held by the company | It is the company-held portion of the issued base |

| Outstanding shares | Shares currently held by outside shareholders | Treasury stock is excluded while held by the company |

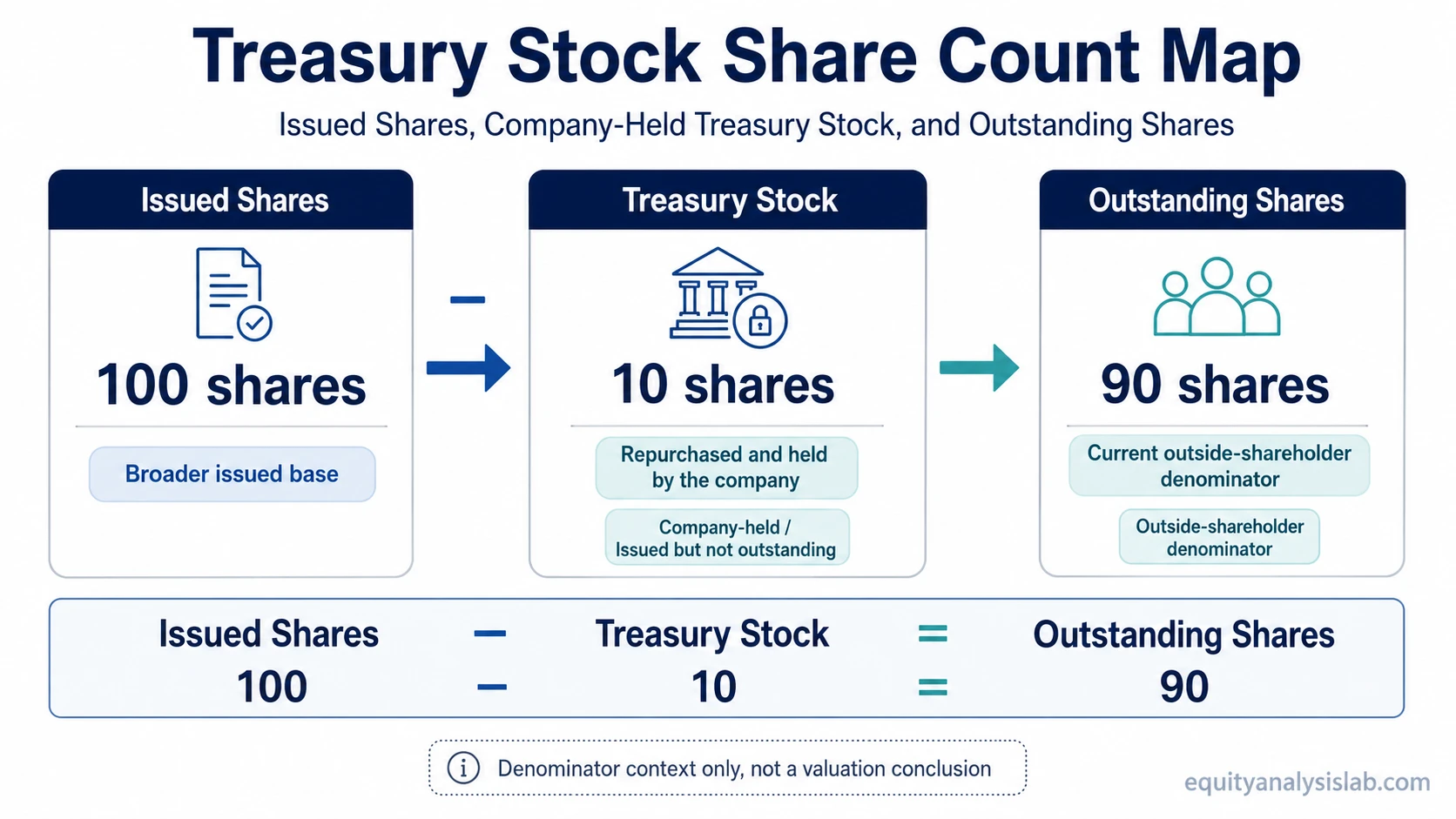

A simple way to read the relationship is: issued shares minus treasury shares equals outstanding shares, assuming there are no additional adjustments in the specific reporting presentation.

How Treasury Stock Affects Share Count

Treasury stock can reduce the outstanding share count because the repurchased shares are no longer held by outside shareholders. If a company repurchases shares and holds them as treasury stock, the current ownership base can become smaller even though the issued-share history remains broader.

For investors, the denominator effect is the useful part. Ownership percentages, earnings per share, book value per share, and other per-share metrics can change when the outstanding share count changes. That effect should be read alongside cash used for the repurchase, the trend in total share count, and whether future instruments could expand the denominator again.

Treasury stock is also separate from diluted shares outstanding, which reflects a broader denominator when potential shares are included. A company can reduce basic outstanding shares through treasury stock while still having a larger diluted denominator if options, convertibles, or other potentially dilutive instruments remain relevant.

Treasury Stock on the Balance Sheet

Treasury stock is usually presented as a reduction of shareholders’ equity rather than as an asset, although exact presentation depends on the reporting framework and company disclosures. The company used resources to repurchase its own shares, but it does not treat those shares like an outside investment asset in ordinary equity-accounting presentation.

This is often described as contra-equity treatment. The practical investor reading is straightforward: treasury stock reduces reported equity presentation, while the share-count effect depends on whether the shares remain held, are retired, or are later reissued.

Accounting limit: The investor-level point is the equity reduction and share-count boundary. A full journal-entry treatment depends on the company’s accounting framework and reporting details, so the concept should not be reduced to one universal entry format.

Voting Rights, Dividends, Retirement, and Reissue

Treasury stock generally does not carry voting rights or receive dividends while it is held by the issuing company. The company is not an outside shareholder of itself in the same economic sense as public investors, so treasury shares do not participate in voting or dividend distribution while they remain in treasury.

The company can later retire treasury shares or reissue them, depending on its policy, legal framework, compensation plans, and financing choices. Retirement permanently removes the shares from the relevant share structure. Reissue can move shares back into circulation, which may increase the outstanding share count again.

This is where treasury stock connects to future dilution without being the same thing as future dilution. Treasury shares already exist; potentially dilutive securities are instruments that may create or add shares to the denominator under certain conditions.

Why Treasury Stock Matters for Investors

Treasury stock matters because it changes the share-count base investors use to interpret ownership and per-share results. If fewer shares are outstanding, each outside share may represent a larger percentage claim on the current shareholder base. That share-count change still has to be read with price paid, cash used, and business quality.

The stronger reading combines treasury stock with the cash cost of the repurchase, the reason shares were bought back, the company’s reinvestment needs, and whether the reduced denominator improves per-share metrics without weakening balance-sheet quality. A lower share count can make earnings per share look better, but the quality of that improvement depends on business performance and capital allocation context.

Treasury stock also does not tell an investor how much stock is freely tradable. Public trading availability is closer to the idea of tradable public float, which excludes certain restricted or closely held shares rather than focusing only on company-held treasury shares.

Simple Treasury Stock Example

Example: A company has 100 issued shares. It repurchases 10 shares and holds them as treasury stock. Issued shares remain 100, treasury shares are 10, and outstanding shares are 90.

| Share-count item | Amount | Meaning |

|---|---|---|

| Issued shares | 100 | Total shares issued before considering the treasury-stock subtraction |

| Treasury stock | 10 | Repurchased shares held by the company |

| Outstanding shares | 90 | Shares currently held outside the company |

The 90-share figure is the current outside-shareholder denominator in this simplified example; it is not a valuation conclusion by itself.

If a shareholder owns 1 share, the current outside ownership base is measured against 90 outstanding shares, not against the 10 shares the company holds in treasury. If those treasury shares are later reissued, the outstanding-share denominator can expand again.

Common Mistakes When Reading Treasury Stock

- Mistake 1: Treating treasury stock as proof that a buyback was good. A repurchase can reduce shares outstanding, but the quality of the decision depends on price paid, cash used, balance-sheet strength, and alternative uses of capital.

- Mistake 2: Reading EPS improvement as automatically higher-quality earnings. EPS can rise when the denominator falls, even if operating performance has not improved at the same rate.

- Mistake 3: Ignoring reissue risk. Treasury shares can return to the outstanding share count if the company reissues them, including for compensation plans, acquisitions, or financing needs.

- Mistake 4: Confusing treasury stock with float. Treasury stock is company-held stock; float is about shares available for public trading after other ownership restrictions are considered.

Related Share-Structure Concepts

Treasury stock is easiest to interpret when it is separated from nearby share-count concepts. The same company can have issued shares, treasury stock, outstanding shares, diluted shares, and float measures that each answer a different question.

| Concept | Main question it answers | Boundary against treasury stock |

|---|---|---|

| Issued shares | How many shares has the company issued? | Treasury stock may remain part of issued shares unless retired |

| Outstanding shares | How many shares are currently held outside the company? | Treasury stock is excluded while held by the company |

| Diluted shares | What broader denominator may apply if potential shares are included? | Treasury stock is about reacquired existing shares, not potential future shares |

| Free float | How many shares are broadly available for public trading? | Float focuses on trading availability, not only company-held shares |

FAQ

What is treasury stock?

Treasury stock is a company’s own previously issued stock that it has repurchased and holds. It is still issued, but it is not counted as outstanding while the company holds it.

Is treasury stock the same as outstanding stock?

No. Outstanding stock is held by outside shareholders. Treasury stock is held by the issuing company, so it is excluded from outstanding shares while held as treasury stock.

Does treasury stock receive dividends?

Treasury stock generally does not receive dividends while it is held by the issuing company. It also generally does not carry voting rights while held in treasury.

Is treasury stock an asset?

Treasury stock is usually shown as a reduction of shareholders’ equity rather than as an asset. The investor-level point is that it reduces equity presentation and affects the share-count base.

Can treasury stock be reissued?

Yes. Treasury stock may be retired or reissued depending on company policy and applicable rules. If reissued, it can increase the outstanding share count again.