Free float is the portion of a company’s shares that is available for public trading after shares held by insiders, strategic owners, governments, lock-up holders, or other restricted holders are excluded.

Investors use free float to understand how much of a company’s equity is actually available in the public market. It is related to shares outstanding, but it is narrower because it focuses on tradable availability rather than the full legal share base.

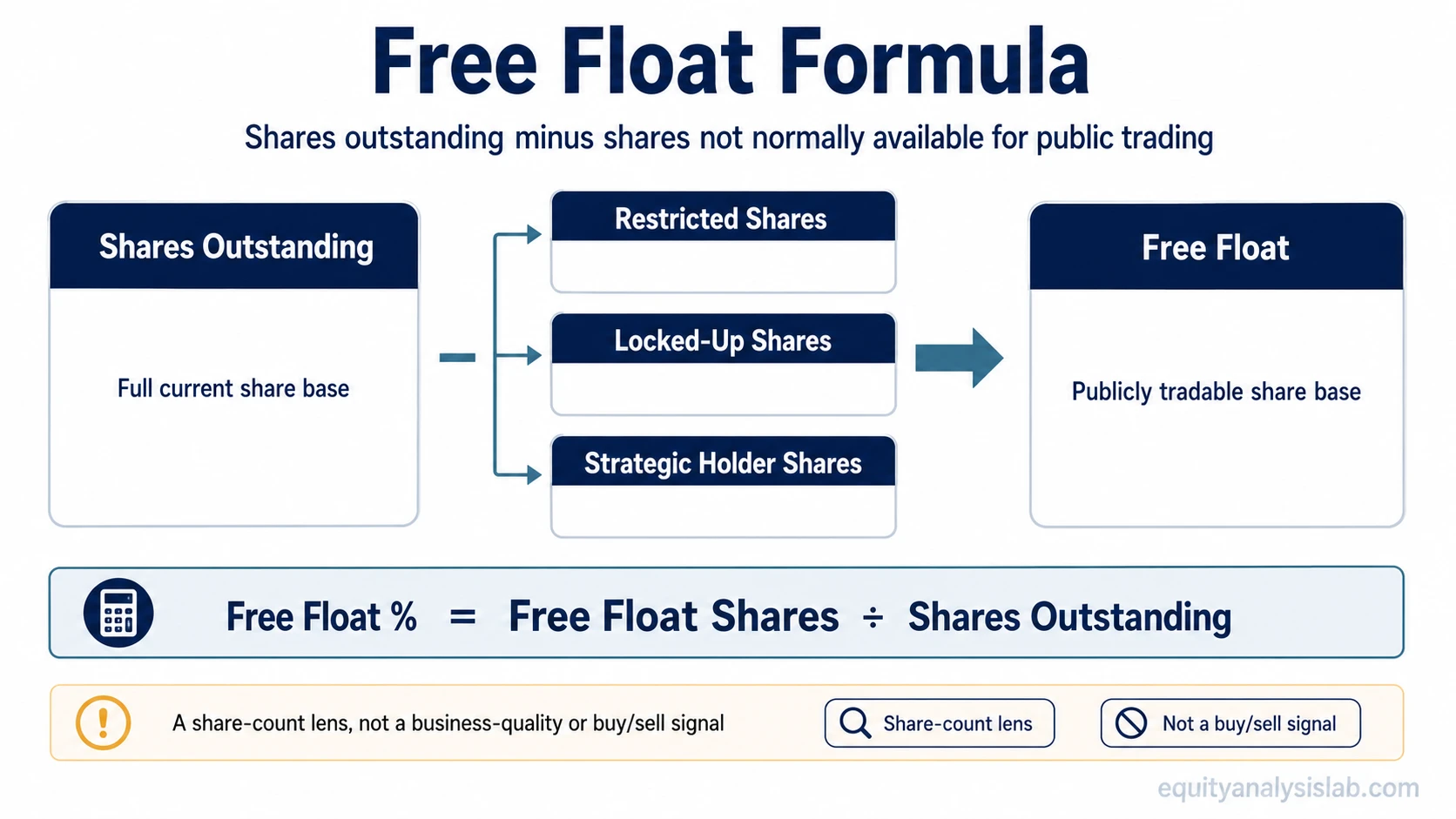

What Is Free Float?

Free float, also called public float, represents the shares that ordinary public-market investors can usually buy and sell. It excludes shares that are outstanding but not freely available for public trading because they are restricted, locked up, or held by long-term strategic owners.

The key distinction is availability. A company may have a large number of shares outstanding, but a smaller free float if a meaningful portion is held by founders, executives, controlling shareholders, governments, or other holders who are not part of the regular public trading supply.

Key Points About Free Float

- Free float measures publicly tradable shares, not the company’s full share count.

- Shares outstanding include both freely tradable shares and shares that may be restricted, locked up, or strategically held.

- Free float can affect liquidity context, index weighting, and how investors compare ownership availability across companies.

- Free float is not the same as dilution, valuation, business quality, or a buy-or-sell signal.

How Free Float Is Calculated

The common calculation starts with total shares outstanding and subtracts shares that are not freely available to the public market.

Free float shares = shares outstanding − restricted shares − locked-in shares − strategic holder shares

Some analysts also express free float as a percentage of shares outstanding. This shows how much of the company’s outstanding share base is available for public trading.

Free float percentage = free float shares ÷ shares outstanding

For example, if a company has 100 million shares outstanding and 30 million shares are held by insiders, strategic holders, or restricted holders, the free float would be 70 million shares. The free float percentage would be 70%.

What Is Included and Excluded From Free Float?

Free float focuses on the shares that can normally trade in public markets. The exact classification can vary by data provider or market convention, but the analytical boundary is consistent: freely tradable public shares are included, while unavailable or strategically locked shares are excluded.

| Share category | Usually included in free float? | Investor interpretation |

|---|---|---|

| Publicly tradable shares | Yes | These shares form the main public trading supply. |

| Restricted shares | No | These shares may be outstanding but unavailable for regular public trading. |

| Locked-up shares | No | These shares may become relevant later if restrictions expire. |

| Strategic holder shares | Usually no | These shares are often treated as outside the normal public float because the holder is not expected to trade them freely. |

| Treasury stock | No | Treasury stock is held by the company and is not part of the public trading float. |

Free Float vs Shares Outstanding

Shares outstanding is the broader share-count measure. Free float is the tradable subset of that measure. The two numbers answer different investor questions.

| Measure | What it answers | What it does not answer |

|---|---|---|

| Shares outstanding | How many common shares currently exist and are outstanding. | How many of those shares are freely available to public investors. |

| Free float | How many outstanding shares are available for regular public trading. | How many shares could exist after future conversion, option exercise, or issuance. |

| Free float percentage | How much of the outstanding share base is publicly tradable. | Whether the stock is cheap, high quality, or likely to move in a specific direction. |

A company can have the same shares outstanding as another company but a very different free float. That difference can matter when investors compare trading availability, ownership concentration, and index-related demand.

Why Free Float Matters for Investors

Free float helps investors separate the full ownership base from the portion of shares that is actually available in the public market. Public trading activity happens inside the float, not across every share that legally exists.

A smaller free float can make the available trading supply more concentrated. That does not automatically make a stock better, worse, or more predictable, but it can change how investors think about liquidity, ownership availability, and the sensitivity of public-market trading to changes in demand.

Free float is also used in float-adjusted market capitalization. In that approach, only freely tradable shares are counted for certain market-cap and index-weighting purposes, rather than using the full shares outstanding figure. This can affect how institutional benchmarks represent a company, but the detailed rules depend on the index or data provider.

What Can Change Free Float?

Free float can change when the boundary between restricted ownership and public availability changes. Lock-up expirations, insider sales, buybacks, new issuance, ownership reclassifications, and changes in strategic holdings can all alter the number of shares treated as publicly tradable.

The direction of the change is not enough by itself. Investors need to understand why the float changed, whether shares outstanding also changed, and whether the change affects ownership availability, dilution risk, or only classification of existing shares.

Free Float Is Not the Same as Dilution

Free float describes current public trading availability. Dilution describes how ownership percentages can change when the share base expands. These are related share-structure concepts, but they are not interchangeable.

A company can have a low free float without creating new shares. A company can also face future dilution risk even if its current free float looks large. Investors should separate the current tradable share base from possible future share creation through convertibles, options, warrants, or other securities.

That distinction matters because dilution changes ownership economics, while free float changes how much of the existing share base is available to trade publicly.

Common Mistakes When Reading Free Float

Mistake 1: Treating free float as business quality. A high free float does not prove that a company has strong earnings, durable cash flow, or good capital allocation. Those questions require separate company analysis.

Mistake 2: Treating low free float as a trading signal. A smaller float can affect liquidity context, but it does not predict price direction by itself. Demand, valuation, fundamentals, risk appetite, and market conditions still matter.

Mistake 3: Confusing free float with dilution. Free float focuses on available existing shares. Dilution risk focuses on whether the share base may expand in the future.

Mistake 4: Reading float changes without context. A change in free float should be interpreted through its cause, not treated as an automatic insider signal or company-quality signal.

A Simple Free Float Example

Consider a company with 200 million shares outstanding. If 80 million shares are held by founders and strategic investors, and another 20 million shares are restricted, then 100 million shares remain in the public float.

In that scenario, the company’s shares outstanding are 200 million, but its free float is 100 million. An investor looking only at shares outstanding would see the full ownership base. An investor looking at free float would see the portion of shares available for normal public trading.

Related Share-Structure Concepts

Free float is one share-count lens, but it does not answer every ownership question. For future-share-count risk, investors can compare the current float with diluted shares outstanding. For the instruments that may expand the share base, see dilutive securities. For the ownership impact of new share creation, use share dilution.

How to Use Free Float in Company Analysis

Free float is most useful as a share-structure lens. It helps investors ask whether the public market is trading a broad share base or a smaller available subset of ownership.

For company analysis, free float should be read alongside shares outstanding, ownership concentration, treasury stock, potential dilution, capital allocation, and liquidity context. It can clarify how the stock trades, but it does not replace analysis of earnings quality, balance-sheet strength, valuation, or business durability.

FAQ

Is free float the same as public float?

Yes. Free float and public float are often used to describe the same idea: the portion of shares available for public trading after restricted, locked-in, or strategic holder shares are excluded.

Does free float include restricted shares?

No. Restricted shares are normally excluded from free float because they are not freely available for regular public trading.

Is a higher free float always better?

No. A higher free float can mean more publicly available shares, but it does not automatically mean better liquidity, stronger business quality, or a more attractive investment. It must be interpreted with ownership structure, valuation, fundamentals, and market context.