Share dilution is the reduction in an existing shareholder’s ownership percentage when a company’s share count increases. The same number of shares represents a smaller claim on the company after the share base expands.

Dilution belongs inside share structure analysis because it changes the denominator investors use to interpret ownership, voting exposure, and per-share financial results. It does not automatically mean the company is weaker or stronger. The key question is whether the new shares support future per-share value or simply spread the same economic claim across more shares.

What Share Dilution Means

Share dilution means existing shareholders own a smaller percentage of the company after additional shares are issued or become counted through conversion, exercise, or settlement. The investor may still own the same number of shares, but those shares represent a smaller slice of a larger equity base.

The mechanism is simple: when the share base expands and an investor’s share count stays unchanged, that investor’s percentage ownership falls.

Key Points About Share Dilution

- Share dilution occurs when a company’s share base expands and existing shareholders do not increase their holdings proportionally.

- Dilution can affect ownership percentage, voting exposure, EPS, and other per-share measures.

- Common sources include secondary offerings, stock-based compensation, options, warrants, convertibles, and stock-funded acquisitions.

- Dilution is not automatically good or bad; investors compare the share-count cost with the capital, assets, incentives, or flexibility the company receives.

- Useful checks include share-count disclosures, diluted share counts, equity compensation notes, convertible instruments, and issuance activity.

How Share Dilution Happens

Dilution usually appears when a company creates new shares or when existing instruments can become common shares. Some dilution is immediate, while other dilution is potential until the relevant securities are exercised, converted, or settled.

| Source of dilution | How it expands the share base | Investor interpretation |

|---|---|---|

| Secondary stock offering | The company sells additional shares to raise capital. | Ownership percentages fall unless existing holders participate in proportion to their prior ownership. |

| Stock-based compensation | Employees or executives receive shares, restricted stock units, or similar awards. | Compensation can align incentives, but it may still create recurring share-count pressure. |

| Options and warrants | Holders may buy shares at a set price if exercise conditions are met. | Potential dilution depends on exercise price, share price, vesting, and contract terms. |

| Convertible debt or preferred stock | Securities may convert into common shares under defined terms. | Debt or preferred financing can later become common equity dilution if conversion occurs. |

| Stock-funded acquisition | The company pays for an acquisition partly or fully with newly issued shares. | Dilution may be offset if the acquired business adds enough earnings, cash flow, or strategic value. |

| Option pools and equity incentive plans | Reserved shares may be used for future employee or executive awards. | The current share count may understate future dilution if planned awards are material. |

Why Dilution Changes Per-Share Analysis

Dilution matters because equity value is not only about the company’s total size. Investors also care about how much of that value belongs to each share. If the company earns more total profit but the share count grows faster, per-share progress can be weaker than the headline business growth suggests.

The most direct effect is ownership percentage. A shareholder who does not add shares owns less of the company after the share count expands. Voting exposure can also fall because each unchanged position represents fewer votes as a percentage of the total voting base, assuming the new shares carry similar voting rights.

Dilution can also affect EPS because earnings are divided by a larger share count. Investors often compare basic share counts, diluted share counts, and potential conversion effects to understand how the denominator used in per-share analysis may change.

Ownership Dilution vs Economic Value Dilution

Ownership dilution and economic value dilution are related, but they are not identical. Ownership dilution happens mechanically when the share count increases. Economic value dilution happens when the ownership issued is worth more than the value the company receives in return.

| Concept | What changes | What investors check |

|---|---|---|

| Ownership dilution | Existing shareholders own a smaller percentage of the company. | New shares issued, conversion terms, exercises, and total shares outstanding. |

| Economic value dilution | Per-share value weakens because the company gives up ownership without enough offsetting value. | Capital raised, acquisition quality, compensation cost, future earnings, cash flow, and return on the newly issued equity. |

A company may issue shares for an acquisition, balance-sheet repair, or long-term investment. Ownership still gets diluted, but the economic result depends on the quality of the tradeoff. Revenue can grow while per-share value lags if the larger share base absorbs too much of the benefit.

Where Investors Can See Dilution in Filings

Dilution is usually visible through share-count disclosures and footnotes rather than one standalone headline number. The goal is to see where the share base changed, what instruments could add more shares, and how per-share results are being calculated.

| Disclosure area | What to check | Why it matters |

|---|---|---|

| Shares outstanding | The current common share base at a point in time. | It gives the starting denominator for ownership and market capitalization analysis. |

| Basic and diluted weighted-average shares | The share counts used in basic EPS and diluted EPS calculations. | A widening gap can show that potential dilution is meaningful. |

| EPS share-count context | How earnings are divided across basic and diluted share counts. | It connects dilution to per-share earnings interpretation without turning the page into a diluted EPS method guide. |

| Equity compensation footnotes | Options, restricted stock units, performance awards, and vesting schedules. | Equity compensation can add shares over time even when the immediate cash impact differs from the share-count impact. |

| Convertible securities disclosures | Convertible debt, preferred stock, warrants, and conversion conditions. | These instruments can become common shares if contract conditions are met. |

| Share issuance notes | New stock offerings, acquisition consideration, employee plans, or financing activity. | They explain why the share count changed and what the company received for the new shares. |

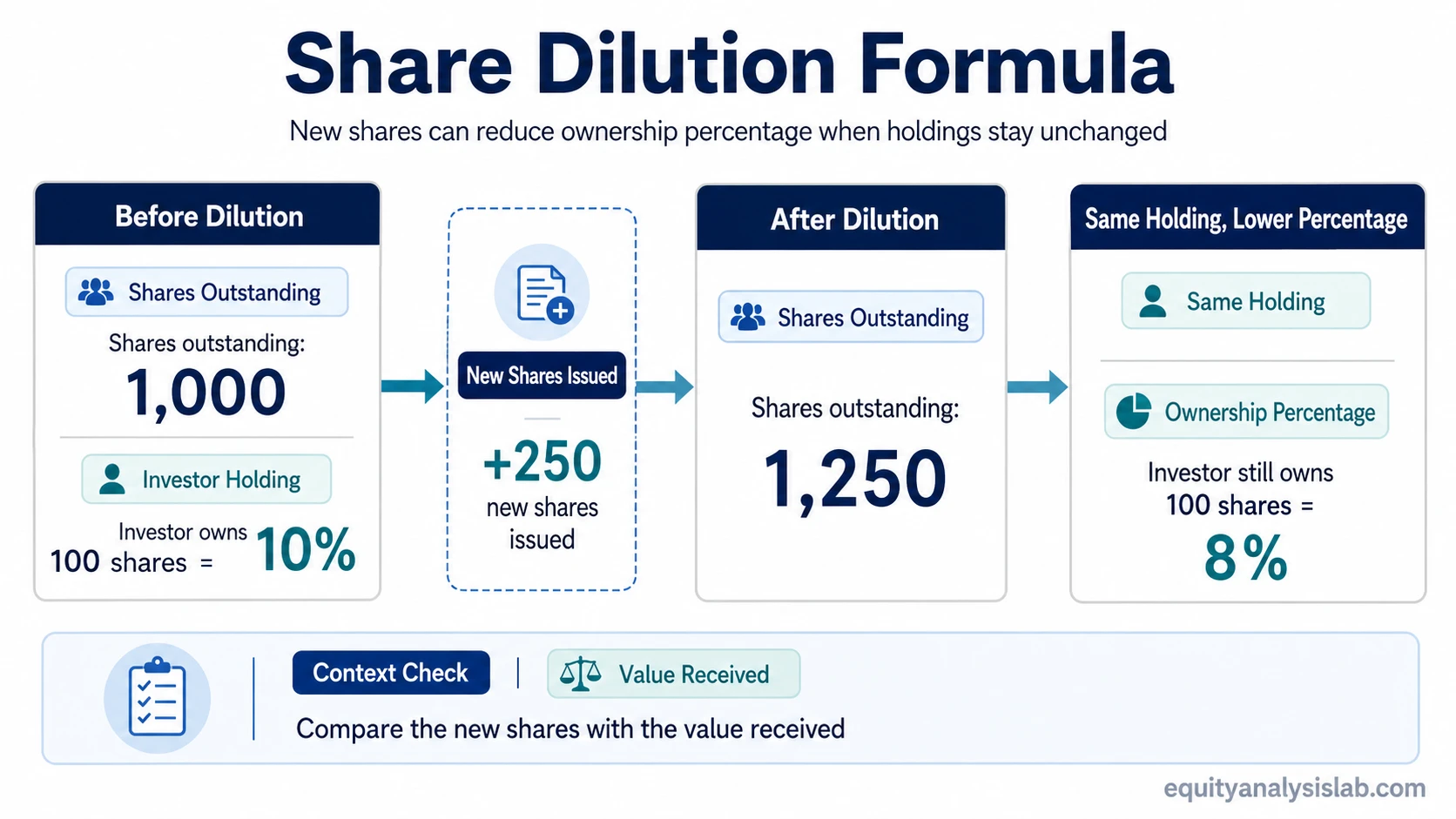

Simple Share Dilution Example

Assume a company has 1,000 shares outstanding. An investor owns 100 shares, equal to 10% ownership.

The company then issues 250 new shares. Total shares rise to 1,250. If the investor still owns 100 shares, the ownership percentage becomes 100 divided by 1,250, or 8%.

The investor did not sell any shares, but the ownership percentage fell because the company created more shares. The next analytical question is whether the company received enough value for the 250 new shares to support future value per share.

When Share Dilution Can Be Misread

A common mistake is treating every increase in share count as automatically negative. Dilution reduces ownership percentage, but the economic result depends on the exchange. Issuing shares to fund a high-return investment can differ from issuing shares to cover recurring losses or excessive compensation.

The opposite mistake is ignoring dilution because the company’s total revenue, earnings, or market value is growing. Per-share analysis matters because shareholders own shares, not the whole company in isolation. Growth that is repeatedly offset by a larger share base may create less value for each share than headline numbers suggest.

Share dilution also should not be read as a stock-price prediction. Markets may react differently depending on valuation, use of proceeds, company quality, capital needs, and investor expectations. Dilution is a share-structure and per-share analysis issue, not a standalone bullish or bearish signal.

Related Share-Count Concepts

Diluted shares outstanding: the potential or conversion-adjusted share-count lens used when instruments such as options, warrants, convertibles, or stock awards may affect the denominator.

Dilutive securities: the instruments that may create additional shares if they are exercised, converted, or settled into common stock.

Free float: the publicly tradable share-count lens. It is useful for liquidity and trading availability, but it is not the same as ownership dilution.

FAQ

Is share dilution always bad for shareholders?

No. Share dilution reduces existing ownership percentage if the investor does not buy more shares, but the economic effect depends on whether the new shares support stronger future value per share.

What is the difference between share dilution and free float?

Share dilution is about ownership percentage falling as the share base expands. Free float is about how many shares are normally available for public trading. A company can have dilution without the same change being explained by free float.