Diluted shares outstanding is the share count that includes common shares already outstanding plus potential shares from instruments that could become common stock. It gives investors a wider denominator for reading per-share figures, ownership percentage, and dilution risk than the basic share count alone.

The useful point is not that every potential share will definitely become common stock. The useful point is that a company may have a larger economic ownership base than the current common share count suggests.

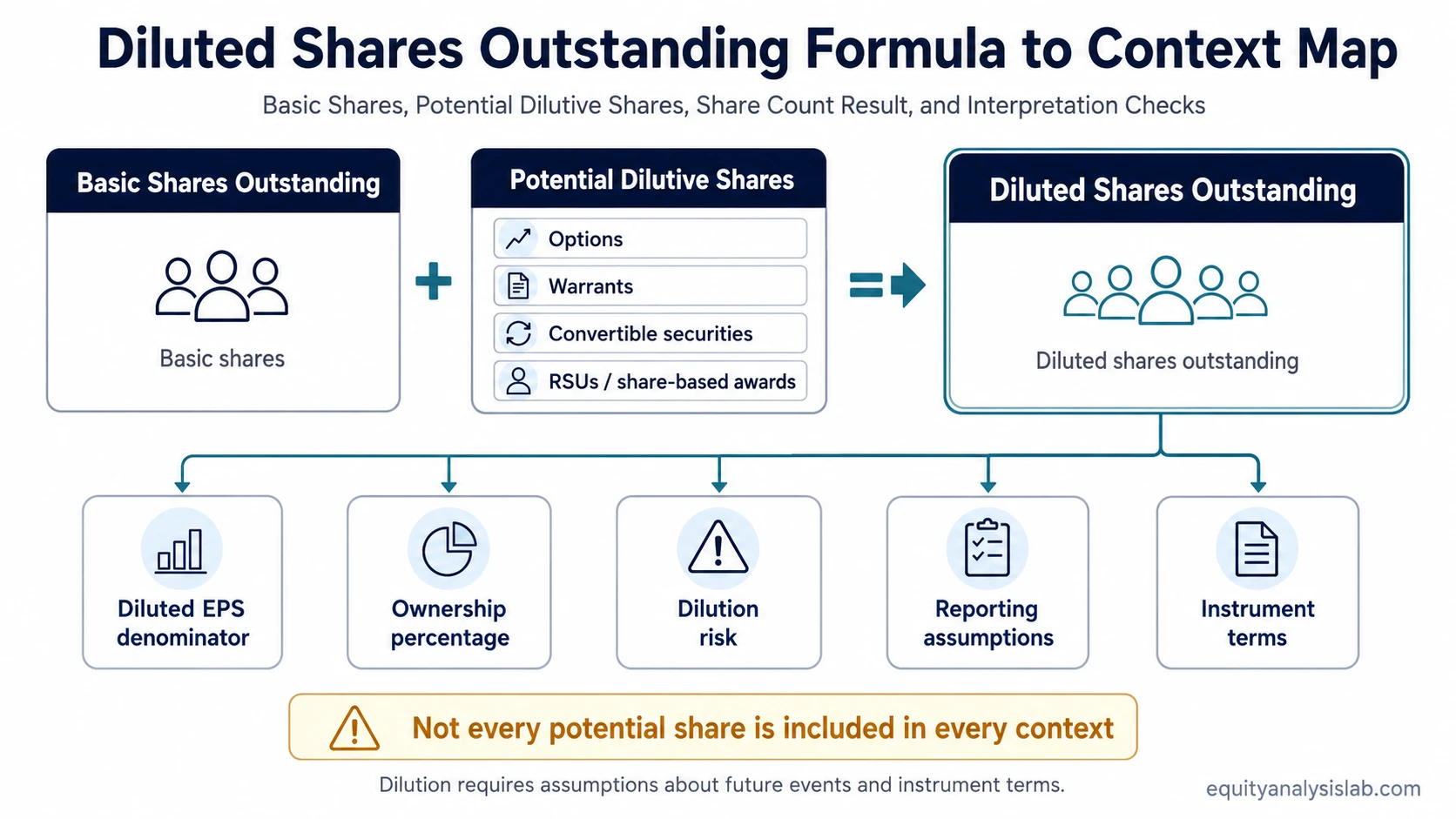

Definition: Diluted shares outstanding represents the total share count after assuming that dilutive instruments, such as options, warrants, restricted stock units, or convertible securities, are included when the relevant accounting or modeling assumptions treat them as dilutive.

Key Points About Diluted Shares Outstanding

- Diluted shares outstanding shows a broader share count than basic common shares outstanding.

- The count can include potential shares from stock options, warrants, convertible debt, convertible preferred stock, restricted stock units, and other share-based compensation.

- It is commonly used as a denominator for diluted EPS and for reading per-share ownership claims.

- A higher diluted share count is not automatically negative, because the instruments, conversion terms, cash proceeds, and business context still matter.

- The metric is a share-structure input, not proof that a stock is attractive, unattractive, cheap, expensive, high quality, or low quality.

What Diluted Shares Outstanding Means

Diluted shares outstanding answers a denominator question: how many shares would the company have if currently dilutive potential shares were included in the share count? That makes it different from a simple count of common shares already issued and outstanding.

In many investor and modeling contexts, fully diluted shares outstanding is used as a close label for the broader share count that includes potentially dilutive common-share equivalents.

For investors, the metric changes how per-share numbers are read. Net income, cash flow, equity value, or ownership percentage can look different when the denominator expands. The metric does not decide whether those numbers are good or bad; it only changes the share base used to interpret them.

Interpretation boundary: diluted shares outstanding is mainly a share-structure and per-share analysis concept. It should not be used by itself as a company-quality score, valuation conclusion, or investment decision rule.

What Is Included in Diluted Shares Outstanding

Diluted shares outstanding can include common shares plus potential shares from dilutive securities. The exact treatment depends on the instrument, accounting rules, reporting period, and whether the instrument is actually dilutive under the relevant assumptions.

| Potential source | How it can affect diluted shares | Important caveat |

|---|---|---|

| Stock options | May add shares if exercise is assumed and the options are treated as dilutive. | The treasury stock method or similar treatment can reduce the net added share count. |

| Warrants | May increase the diluted share count if warrant exercise would create additional common shares. | Out-of-the-money or anti-dilutive treatment may change inclusion. |

| Convertible debt | May add shares if debt conversion into common stock is assumed. | The related interest expense and accounting method can affect diluted EPS treatment. |

| Convertible preferred stock | May add shares if preferred stock conversion into common stock is assumed. | The preferred dividend and conversion terms still matter. |

| Restricted stock units and share-based compensation | May add shares when awards are expected to settle in common stock. | Vesting, settlement terms, and anti-dilutive treatment can affect the count. |

The reported diluted share count is therefore not just a raw list of every possible instrument. It is a filtered count shaped by assumptions about dilution, conversion, exercise, and accounting presentation.

Diluted Shares Outstanding vs Shares Outstanding

The core distinction is timing and scope. The current outstanding share count usually refers to common shares that already exist. Diluted shares outstanding adds the potential common shares that could expand the ownership base if relevant instruments are included.

| Metric | What it measures | Best use |

|---|---|---|

| Basic shares outstanding | Common shares currently outstanding. | Reading the current common share base. |

| Diluted shares outstanding | Common shares plus potential shares treated as dilutive. | Reading per-share figures under a broader ownership denominator. |

| Authorized shares | The maximum number of shares a company is allowed to issue under its governing documents. | Understanding legal issuance capacity, not current dilution by itself. |

| Tradable float | The portion of shares generally available for public trading. | Reading market liquidity and tradable supply, not the full diluted ownership base. |

How Investors Use Diluted Shares Outstanding

Diluted shares outstanding is most useful when an investor is trying to understand per-share claims. A company with strong total earnings can still show weaker per-share economics if the share base expands. A company with a stable basic share count can still have meaningful potential dilution if options, warrants, convertibles, or stock compensation add shares under diluted treatment.

The metric also helps separate company-level economics from shareholder-level economics. Revenue, operating income, and free cash flow describe the business. Diluted share count helps translate those business results into a claim per share.

Denominator model: diluted shares outstanding changes the ownership base used for per-share analysis. It does not change the company’s revenue, margin, cash balance, debt load, or competitive position by itself.

Short Example of Diluted Shares Outstanding

Assume a company has 100 million basic shares outstanding. It also has options, warrants, and restricted stock units that could add 10 million shares if they are treated as dilutive under the relevant assumptions. In that simplified case, the diluted share count would be 110 million shares.

| Item | Illustrative share count |

|---|---|

| Basic shares outstanding | 100 million |

| Potential dilutive shares | 10 million |

| Diluted shares outstanding | 110 million |

The example does not mean every potential share will convert. It shows why the denominator used for per-share analysis can be larger than the current basic share count. If the same total net income is divided by 110 million diluted shares instead of 100 million basic shares, the per-share figure is lower even though total company income has not changed.

Where to Find Diluted Shares Outstanding

Investors can usually find diluted shares outstanding near the earnings-per-share section of a company’s income statement or financial statement notes. The label may appear as diluted weighted-average shares, diluted shares, weighted-average diluted shares, or a similar phrase depending on the filing and accounting presentation.

The number should be read with the period and context attached. A quarterly diluted weighted-average share count, an annual diluted weighted-average share count, and a point-in-time modeled fully diluted share count may not be identical.

Reporting caution: diluted weighted-average shares are period-based. A cap table or valuation model may use a different share-count view if it is trying to estimate ownership under a different set of assumptions.

Why Diluted Shares Outstanding Can Mislead

Diluted shares outstanding can mislead when it is read as a simple good-or-bad signal. A rising diluted share count may reflect employee compensation, acquisition consideration, convertible financing, warrant exercise, or other capital-structure choices. Some are costly to existing holders; some may be paired with cash proceeds or business expansion.

The opposite can also mislead. A company may report little current dilution while still having authorization, incentive plans, convertible instruments, or financing needs that could matter later. The reported diluted count is useful, but it is not the full share-structure story.

Common mistake: treating diluted shares outstanding as a verdict instead of a denominator. The metric should lead to questions about instrument terms, dilution history, per-share economics, and future issuance risk.

Diluted Shares Outstanding and Diluted EPS

Diluted shares outstanding is closely connected to diluted earnings per share because diluted EPS uses a diluted share denominator. If the denominator rises while net income is unchanged, diluted EPS is lower than it would be under the basic share count.

That does not make diluted shares outstanding a complete EPS analysis by itself. Diluted EPS also depends on net income, preferred dividends, interest adjustments for convertibles, tax effects, and the accounting method applied to each instrument.

Use boundary: diluted shares outstanding helps explain the denominator side of diluted EPS. It does not replace a full earnings-quality, accounting, or valuation review.

How to Interpret Diluted Shares Outstanding

A useful interpretation starts with the spread between basic and diluted shares. A small spread may suggest limited current dilution under the reporting assumptions. A large spread can suggest that potential shares are meaningful enough to affect per-share analysis.

The next step is to read the source of the spread. Options and RSUs are different from convertible debt. Warrants are different from preferred stock. A one-time acquisition-related issuance is different from repeated share-based compensation that expands the denominator year after year.

| Question | Why it matters |

|---|---|

| How large is the gap between basic and diluted shares? | It shows whether potential dilution is small or material under current assumptions. |

| Which instruments create the gap? | Different instruments have different economics, proceeds, incentives, and conversion terms. |

| Is the diluted count rising over time? | A persistent increase can weaken per-share economics even when total company results improve. |

| Are anti-dilutive instruments excluded? | Excluded instruments can still matter later if price, profitability, or conversion assumptions change. |

Basic Share Count, Potential Shares, and Reporting Assumptions

The basic share count is the starting point. Potential shares are the instruments that could become common stock. Reporting assumptions decide which of those instruments appear in diluted shares outstanding for the period.

This is why diluted shares outstanding should be read with both the income statement and the notes. The headline number tells the investor the denominator. The notes help explain how that denominator was formed.

Interpretation sequence: start with basic shares, identify potential common-share equivalents, check whether they are dilutive or anti-dilutive, then compare the final diluted count with per-share metrics and ownership context.

Anti-Dilutive Treatment and Treasury Stock Method Boundaries

Not every potential share is included in diluted shares outstanding. Some instruments may be anti-dilutive under accounting rules for a given period, meaning including them would not reduce EPS or would otherwise fail the relevant dilution test.

Anti-dilutive treatment can make the reported diluted share count look smaller than a simple list of all possible shares. That does not mean the instruments disappeared. It means they were not included in the reported diluted denominator for that period.

Modeling caution: a valuation model may still review excluded instruments if they could become dilutive under different share-price, earnings, or conversion assumptions.

The treasury stock method is another boundary. It can affect how options and warrants are included, but a full treasury-stock-method model is a separate calculation topic. The important point is that diluted share count depends on assumptions, not just on the face amount of every instrument.

Diluted Shares Outstanding and Nearby Share-Structure Terms

Diluted shares outstanding sits near several share-structure concepts, but each one answers a different question.

| Concept | Main question it answers | Boundary |

|---|---|---|

| Diluted shares outstanding | What share count is used if dilutive potential shares are included? | Best for per-share denominator analysis. |

| Dilutive securities | Which instruments can create additional common shares? | Best for identifying the inputs that may expand the share count. |

| Shares outstanding | How many common shares currently exist? | Best for reading the current common share base. |

| Free float | How many shares are generally available for public trading? | Best for tradable supply and market-liquidity context, not full dilution. |

| Share dilution | How does ownership percentage decrease when new shares are issued? | Best for the process and effect of ownership reduction. |

The distinction from free-float shares is especially important. A company can have a large diluted share count while only part of its shares are actively tradable in the public market.

FAQ

What does diluted shares outstanding mean?

Diluted shares outstanding means the share count after including common shares plus potential shares from instruments that are treated as dilutive, such as options, warrants, convertibles, or stock-based compensation.

Is diluted shares outstanding the same as shares outstanding?

No. Shares outstanding usually refers to common shares that already exist, while diluted shares outstanding includes potential common shares when they are treated as dilutive under the relevant assumptions.

Does a higher diluted share count always mean more dilution?

No. A higher diluted share count shows that the per-share denominator may be larger under the relevant assumptions. The investor still needs to read the instruments, conversion terms, anti-dilutive treatment, business results, and dilution history.

Where can investors find diluted shares outstanding?

Investors can often find diluted weighted-average shares in the earnings-per-share section of a company’s financial statements. The exact label and presentation can vary by filing and accounting context.