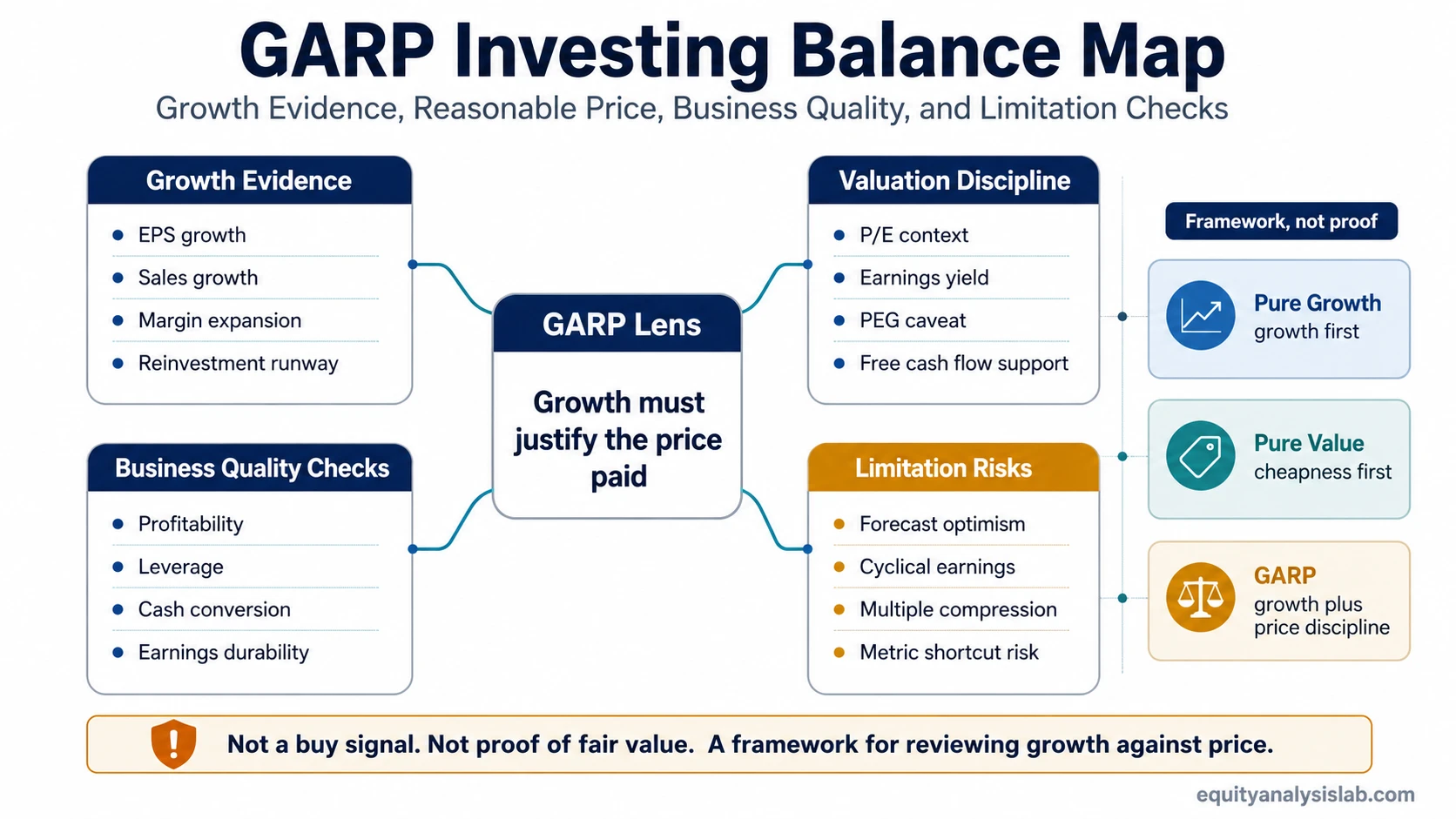

GARP investing stands for growth at a reasonable price. It changes the stock selection question from “Is this company growing?” or “Is this stock cheap?” to “Is the growth evidence strong enough to justify the valuation being paid?” The style looks for companies with credible growth while avoiding prices that already assume too much future success.

The balance is the point. A company can grow quickly and still be unattractive if expectations are already excessive. A company can look inexpensive and still fail the GARP lens if growth is weak, unstable, or unsupported by business quality. GARP sits between growth and value investing, but it is not a standalone buy rule.

What Is GARP Investing?

GARP investing means growth at a reasonable price. It is a stock selection lens that looks for companies with earnings or sales growth while still applying valuation discipline.

The framework starts with the idea that growth alone is not enough. Future growth must be judged against the price investors are paying today. A GARP investor may prefer a company that is growing steadily at a valuation that still leaves room for disappointment, rather than a faster-growing company priced for a nearly perfect future.

GARP is also not the same as searching only for statistically cheap stocks. The valuation must be reasonable relative to the company’s growth evidence, profitability, financial strength, and earnings durability. That makes GARP a hybrid style rather than a pure growth or pure value approach.

How GARP Combines Growth and Valuation

GARP combines two questions that are often separated. The first question is whether the company is producing real growth. The second is whether the market price already reflects too much of that growth. The framework becomes useful only when both sides are examined together.

Growth evidence can include earnings growth, sales growth, margin expansion, reinvestment opportunities, or improving returns on capital. Valuation discipline can include price-to-earnings, earnings yield, enterprise value multiples, free cash flow measures, or the PEG ratio. None of these inputs is decisive by itself.

The PEG ratio is often associated with GARP because it compares valuation to expected growth. A lower PEG can make a company look more reasonably priced relative to its growth rate, but it does not prove that the stock is cheap. The ratio can break down when earnings are negative, forecasts are unreliable, growth is cyclical, or accounting earnings are not supported by cash flow.

What Investors Look For in a GARP Stock

GARP analysis usually reviews several observable inputs rather than relying on one metric. The goal is to check whether growth, valuation, and business evidence point in the same direction.

| Observable input | What it can suggest | What it cannot prove |

|---|---|---|

| EPS growth | Whether earnings are expanding over time | That future earnings growth will continue |

| Sales growth | Whether demand or business scale is increasing | That growth is profitable or shareholder-friendly |

| Valuation multiple | How much investors are paying for current or expected results | That the stock is fairly valued |

| PEG ratio | How valuation compares with expected growth | That growth estimates are accurate or durable |

| Profitability | Whether growth is supported by margins or operating strength | That the business has a durable advantage |

| Leverage | Whether debt risk could weaken the growth story | That the balance sheet is safe under stress |

| ROE or returns on capital | Whether the company earns attractive returns on its capital base | That high returns are sustainable |

| Earnings-to-price or earnings yield | Whether earnings are meaningful relative to market price | That the stock offers a margin of safety |

| Cash-flow support | Whether reported earnings are backed by cash generation | That reported growth is high quality in every period |

| Earnings durability | Whether growth appears repeatable rather than one-off | That future estimates will be met |

A simple example shows the boundary. A company with moderate earnings growth and a moderate valuation may fit the GARP lens better than a company with explosive growth but a valuation that assumes years of flawless execution. The point is not that the first company is automatically better. The point is that GARP asks whether the price paid leaves enough room for the growth evidence to matter.

GARP vs Growth, Value, and Quality Investing

GARP differs from growth-focused investing because it does not treat expansion as sufficient by itself. A fast-growing company can fail a GARP review if the valuation already prices in unrealistic expectations.

GARP also differs from value investing. A traditional value lens may focus more heavily on undervaluation, asset value, earnings yield, or a margin-of-safety concept. GARP accepts growth as a central part of the thesis, but still requires price discipline.

GARP can overlap with business quality checks, but it should not replace them. A company can look reasonable on growth and valuation numbers while still having weak cash conversion, high leverage, customer concentration, or earnings that depend on one temporary condition.

GARP can also sit inside bottom-up investing. The bottom-up process starts with company-level research, while GARP is a style lens that helps frame the relationship between growth and price.

Where GARP Investing Can Mislead

GARP is weakest when the growth input is unstable, the valuation input is incomplete, or the business-quality check is skipped. A stock can look reasonable on a growth-adjusted metric and still be risky if estimates are too optimistic, earnings are cyclical, or cash flow does not support reported profit.

The most common problem is treating PEG as proof. A PEG ratio depends on the growth rate used in the calculation. If that growth rate is based on optimistic forecasts, temporary earnings recovery, or a cyclical upswing, the stock can look more reasonable than it really is.

Negative or inconsistent earnings can also make the framework less useful. If earnings are not stable enough to compare against price, the growth-to-valuation relationship becomes harder to interpret. In those cases, revenue growth, cash flow, leverage, and business model durability may matter more than a single valuation-to-growth ratio.

GARP can also understate risk when valuation multiples compress. A company may keep growing, but the stock can still perform poorly if investors decide that the old multiple was too high. This is why reasonable price should be treated as a judgment about expectations, not a mechanical threshold.

What GARP Is Not

GARP is not a buy signal. It is a way to organize the relationship between growth evidence and valuation discipline. It does not prove that a stock is attractive, undervalued, high quality, or likely to produce a future return.

GARP is not only a fund or index category. Funds and indexes may use GARP-style rules, but the concept itself is broader: it describes a stock selection lens that can be applied to company analysis, screening, or portfolio review.

GARP is not a full stock screener tutorial. Screening may help identify candidates, but the investment decision still needs company research, financial statement review, valuation work, competitive analysis, and risk assessment.

GARP is not a replacement for judgment. A company with growth, a reasonable multiple, and a favorable PEG ratio can still disappoint if growth quality weakens, debt risk rises, margins compress, or future estimates reset lower.

Related Stock Selection Concepts

Use GARP as the concept for balancing growth and valuation. Use growth investing when the main question is how investors evaluate expansion potential. Use quality investing when the main question is whether the business can sustain returns, margins, cash flow, and competitive strength.

Use bottom-up investing when the broader process starts from company-level research rather than macro, sector, or index-level allocation. GARP can fit inside that process, but it does not replace the full research workflow.