Growth investing is a stock-selection style focused on companies expected to grow faster than peers or the broader market. The style depends on whether future growth is observable, durable, cash-supported, and reasonable relative to the valuation already attached to the stock.

Definition: Growth investing means analyzing businesses whose revenue, earnings, cash flow, or reinvestment opportunities may expand faster than comparable companies or the market average. A growth label describes the research lens, not proof that a stock is attractive.

Key Points

- Growth investing starts with expected business expansion, not with a low valuation multiple.

- Revenue growth is only one input. Earnings quality, cash support, margins, reinvestment returns, dilution, and balance-sheet stress can change the interpretation.

- A company can be growing quickly and still be unattractive if the stock price already assumes near-perfect execution.

- Growth investing is not a buy rule, return forecast, portfolio suitability test, or list of best growth stocks.

What is growth investing?

Growth investing focuses on companies whose business results are expected to expand faster than peers, the sector, or the broader equity market. The expected growth may come from rising revenue, expanding earnings, improving margins, larger addressable markets, successful reinvestment, or stronger competitive position.

Growth investing looks forward. The investor is not only asking what the company is worth based on current results. The harder question is whether future growth can justify today’s valuation, and whether the evidence behind that growth is strong enough to survive changes in margins, competition, financing conditions, or expectations.

How growth investing changes the stock-selection question

Value investing often begins with price compared with current or normalized value. Growth investing begins with the expected expansion path of the business. The focus moves from “is the stock cheap now?” toward “can the business grow enough, for long enough, and with enough quality to support the valuation?”

That shift creates a different evidence burden. A company with fast sales growth may still have weak investment quality if profits are not converting into cash, if margins depend on temporary conditions, if share dilution absorbs much of the gain, or if the valuation already assumes very high future success.

Research lens: Growth investing is strongest when growth is tied to observable business evidence. It becomes weaker when the case depends mostly on narrative, hype, or distant assumptions that cannot be checked against revenue quality, earnings quality, cash flow, and reinvestment results.

What investors examine in a growth-investing lens

A growth investor usually examines both the pace of growth and the quality of that growth. Fast expansion is more useful when it is recurring, profitable or moving toward profitability, supported by cash generation, and achieved without excessive dilution or balance-sheet strain.

Durability also matters. A business can grow quickly for a short period because of product cycles, temporary demand, easy financing, or sector enthusiasm. More durable growth is usually connected to repeat customers, pricing power, scalable economics, strong reinvestment opportunities, or a business model that can expand without needing proportionally higher capital.

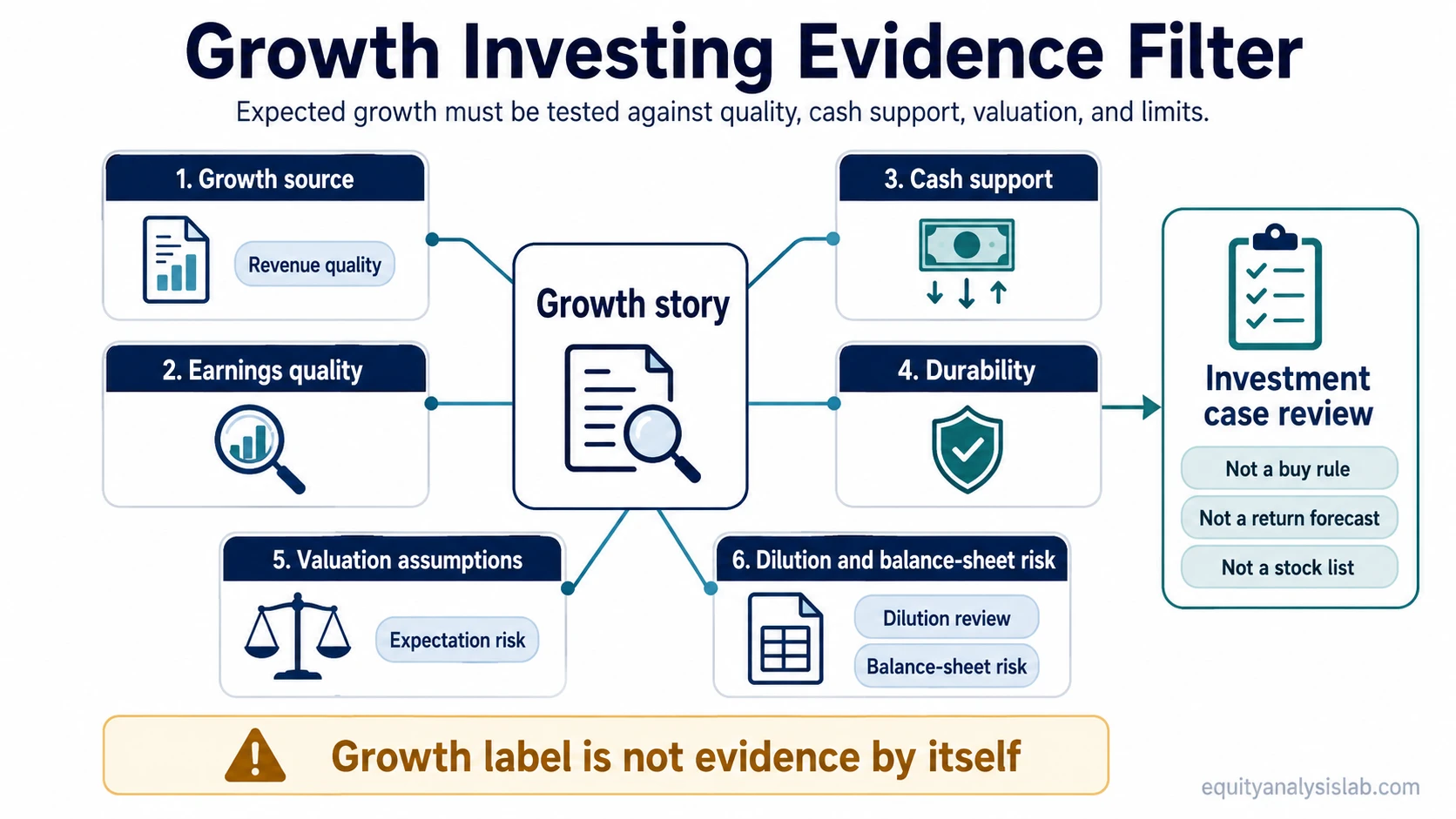

Growth Investing Evidence Filter

The evidence filter separates a growth story from a growth investment case. Each row tests whether the expected expansion is visible in the business, supported by financial statements, and not already fully priced into the stock.

| Evidence area | What to examine | Why it matters |

|---|---|---|

| Growth source | Revenue growth, unit growth, pricing, market share, customer growth, product expansion | Identifies whether growth comes from real business expansion or from temporary conditions. |

| Earnings quality | EPS growth, operating profit, recurring profit, one-time gains, margin trend | Shows whether growth is reaching shareholders through repeatable earnings rather than accounting noise. |

| Cash support | Operating cash flow, free cash flow, working-capital needs, capital expenditure intensity | Tests whether reported growth is supported by cash or depends on constant external funding. |

| Reinvestment runway | ROIC, incremental returns, new markets, product depth, capital allocation | Shows whether the company can reinvest at attractive rates instead of growing only by spending more. |

| Durability | Business model strength, competitive position, customer retention, pricing power | Separates short growth bursts from growth that may persist across cycles and competitive pressure. |

| Valuation assumptions | Revenue multiple, earnings multiple, margin assumptions, terminal growth, discount-rate sensitivity | Checks whether the market already prices in a demanding growth path. |

| Dilution and balance-sheet risk | Share count, stock-based compensation, debt, refinancing needs, liquidity pressure | Growth may not benefit shareholders if ownership is diluted or financing risk rises. |

| Expectation risk | Consensus growth, guidance dependency, margin expectations, execution assumptions | High expectations can leave little room for normal business volatility. |

Growth investing vs adjacent styles

Growth investing overlaps with several nearby investing styles, but each lens starts from a different question. The same company can look attractive through one lens and incomplete through another.

| Style | Main question | Boundary against growth investing |

|---|---|---|

| Value investing | Is the stock priced below a reasonable estimate of value? | Value starts with discount or mispricing. Growth starts with future expansion and then tests whether the valuation can be justified. |

| GARP investing | Is growth available at a reasonable price? | GARP narrows the growth lens by making valuation discipline more explicit at the start. |

| Quality investing | Does the business have durable economics? | Quality can support growth, but strong business quality does not automatically mean high future growth. |

| Bottom-up investing | What does company-level evidence say before macro or theme arguments? | Bottom-up research can be used inside a growth approach, but it is a broader company-first process rather than a growth-only style. |

| Top-down investing | Which sectors or themes may benefit from broad economic conditions? | Top-down investing starts with outside context. Growth investing still has to prove the company-specific growth case. |

Where growth investing can mislead investors

Future growth can be overestimated. Growth investing relies on expectations, and expectations can be wrong. Revenue growth can slow, margins can compress, competitors can copy the model, or reinvestment opportunities can become less attractive.

High growth may already be priced in. A strong business can still disappoint shareholders if the valuation already assumes exceptional future results. The business can perform well while the stock performs poorly if expectations were too high.

The growth label is not evidence by itself. A stock does not become attractive because it belongs to a growing industry, appears in a growth-stock list, or has a high revenue growth rate. The evidence must connect growth, profitability, cash support, dilution, balance-sheet risk, and valuation assumptions.

A simple growth-investing scenario

A company reports rapid revenue growth for several years, and the market begins treating it like a clear growth stock. The first read is tempting because the top line is expanding and the addressable market sounds large.

The evidence becomes less convincing if operating cash flow remains weak, share count keeps rising, margins are deteriorating, and the valuation assumes years of smooth execution. The evidence becomes stronger when cash conversion improves, margins stabilize or expand, dilution stays disciplined, and reinvestment returns support the growth story. Without those pieces, revenue growth alone is incomplete.

Related concepts

Bottom-up investing helps frame the company-first research process behind a growth case.

GARP investing adds a stricter price-discipline lens when growth expectations need valuation control.

Quality investing focuses on durability, business strength, and economic resilience that can support or challenge a growth thesis.