Value investing is a stock-selection lens that compares a company’s market price with an evidence-supported estimate of its business value.

Its decision role is to test whether the current price sits below a defensible value range after downside risks are counted. A low share price, low P/E ratio, or low price-to-book ratio is not enough by itself, because cheapness can reflect weaker earnings, poor cash conversion, leverage, dilution, or a business in structural decline.

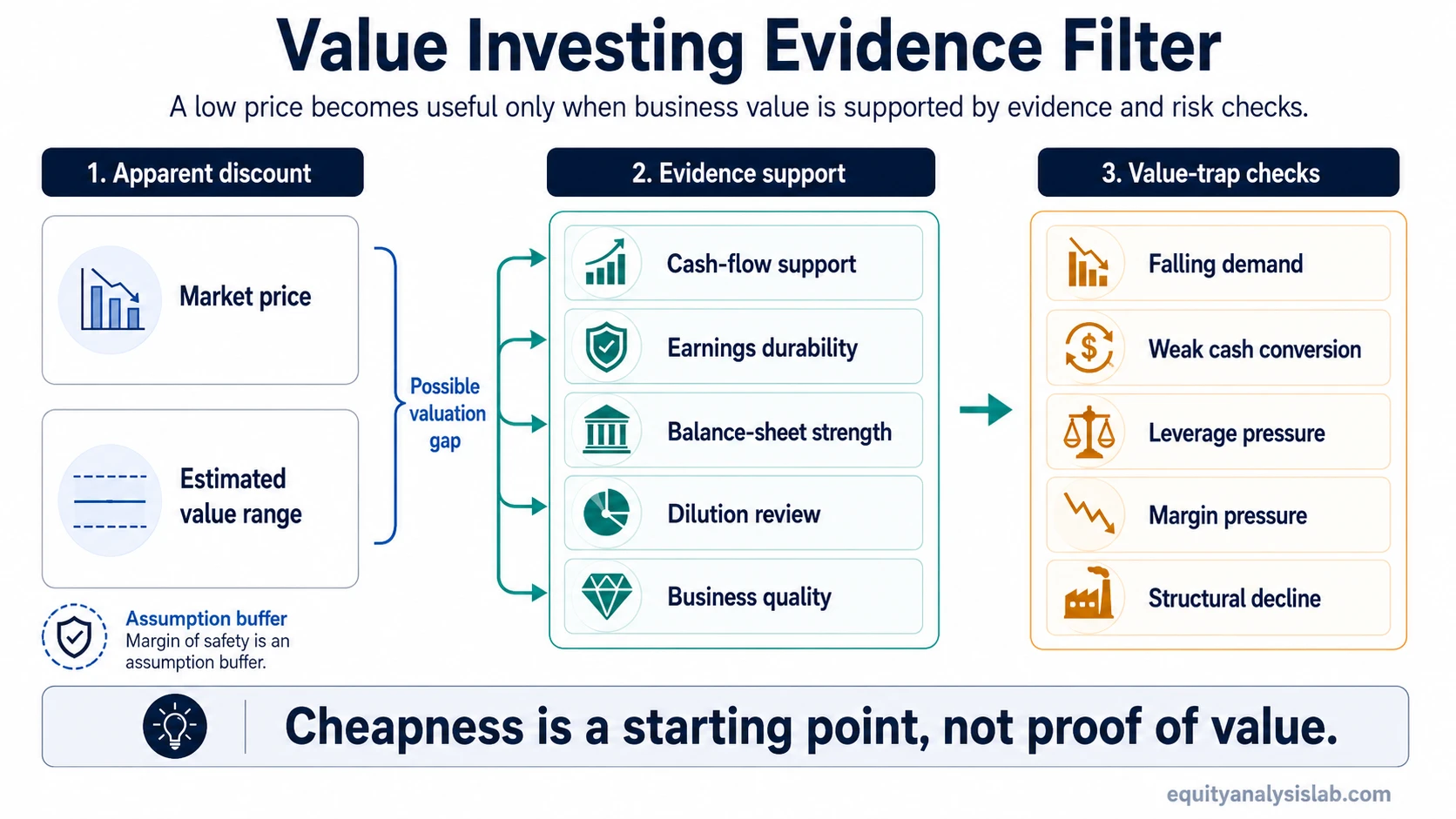

Definition: Value investing means looking for stocks that appear priced below a reasonable estimate of fundamental value, then testing whether the discount is supported by financial statements, cash flow, balance-sheet strength, business durability, and realistic forward expectations. The estimate should be treated as a range that depends on cash flow, durability, balance-sheet risk, and forward expectations, not as a precise target value.

Key Points

- Value investing compares market price with estimated fundamental value, not with price history alone.

- Low valuation multiples are starting points for analysis, not proof that a stock is undervalued.

- Margin of safety is an assumption buffer, not protection against loss or business deterioration.

- Value traps occur when cheapness reflects real damage to earnings, cash flow, balance-sheet quality, or future prospects.

What Value Investing Means

Value investing starts with the gap between price and estimated business value. The market price is observable, but the value estimate depends on assumptions about future cash flow, earnings durability, assets, liabilities, reinvestment needs, and the quality of management’s capital allocation.

The central question is not whether a stock looks cheap. The stronger question is whether the discount remains attractive after the weak parts of the business are counted honestly. A company can trade at a low multiple because investors are too pessimistic, but it can also trade there because the business deserves a lower valuation.

Intrinsic value is best treated as an estimate range, not a precise number. Different assumptions about margins, revenue durability, reinvestment, interest costs, and terminal value can produce different valuation ranges. Value investing depends on evidence quality as much as valuation math.

How Value Investing Works

The process often starts with a valuation gap. An investor sees a stock trading below what the business might be worth under reasonable assumptions, then checks whether the discount is justified by the company’s fundamentals.

Fundamental analysis gives the discount thesis its evidence base. Income statements show revenue, margins, and earnings patterns. Cash-flow statements test whether reported profits convert into cash. Balance sheets show debt, liquidity, asset quality, and financial flexibility. Share-count data shows whether dilution is reducing each investor’s claim on future earnings.

Margin of safety is the gap between the purchase price and the estimated value range. It exists because valuation is uncertain. The gap can help absorb forecast error, but it does not remove business risk, market risk, or the possibility that the valuation estimate was too optimistic.

Evidence discipline: A low multiple is an invitation to test the business, not a conclusion. Cash flow, earnings quality, balance-sheet risk, dilution, and durability decide whether the valuation gap has support.

What Value Investors Look At

Value investing uses valuation inputs as clues. Each input can suggest a possible discount, but each one can also hide a weakness that breaks the value case.

| Valuation input | What it can suggest | What can break the value case |

|---|---|---|

| Low P/E ratio | The market is paying less for each dollar of reported earnings. | Earnings may be cyclical, declining, one-time, or weakly supported by cash flow. |

| Low price-to-book ratio | The stock trades near or below stated net asset value. | Book value may include impaired assets, weak returns on equity, or balance-sheet risks. |

| Free cash flow yield | The business may generate meaningful cash relative to its market value. | Cash flow may depend on underinvestment, working-capital timing, or unsustainable cost cuts. |

| Book value and tangible assets | Asset backing may support part of the valuation setup. | Assets may be hard to realize, overvalued, restricted, obsolete, or tied to a weak business model. |

| Earnings durability | Stable profits can make a low valuation more meaningful. | Customer loss, margin pressure, cyclicality, or competitive decline can reduce future earnings power. |

| Balance-sheet strength | Low leverage and liquidity can give the company more time to recover. | Debt maturities, refinancing costs, pension obligations, or off-balance-sheet risks can absorb value. |

| Dilution and share count | A stable or falling share count can preserve each share’s claim on value. | New issuance, stock-based compensation, or convertible securities can reduce per-share upside. |

Why Cheap Is Not Enough

A value trap is a stock that looks inexpensive on surface metrics but stays cheap or becomes cheaper because the underlying business is deteriorating. The apparent discount can disappear once lower future earnings, weaker cash flow, higher debt costs, or structural pressure are included in the analysis.

Cheap is not enough: A low valuation becomes more useful only when the business can support the estimated-value argument. Weak cash conversion, falling demand, leverage, dilution, poor capital allocation, or permanent margin pressure can make a low multiple misleading.

The practical risk is treating valuation as separate from quality. A lower price can make the valuation setup more attractive only if the value estimate is realistic and the business risks have been counted honestly. If the business is weaker than the estimate assumes, the discount may be a warning rather than an opportunity.

Quality checks do not replace value investing. They test whether the value estimate deserves confidence. Earnings quality, recurring cash generation, competitive position, and balance-sheet resilience help separate a possible bargain from a business whose lower valuation reflects real damage.

Value Investing Compared With Nearby Styles

Value investing begins with price versus estimated fundamental value. Growth investing begins more directly with expected business expansion, future earnings growth, and the durability of reinvestment opportunities.

Value and growth are not always opposites. GARP investing looks for a balance between growth potential and valuation discipline, so the valuation question remains important even when the business is still expanding.

Bottom-up investing starts with the individual company and builds the research sequence from business evidence first. Value investing can use that company-first sequence, but its defining lens is the discount between price and estimated value.

Quality analysis is a test inside the value case. A low valuation looks more credible when earnings quality, cash-flow support, balance-sheet strength, and business durability do not explain the discount away.

A Simple Value Investing Scenario

A company trades at a lower earnings multiple than similar businesses after a period of weak sentiment. The first read is tempting because the stock appears inexpensive, but the discount remains unresolved until cash flow and earnings durability support the value estimate.

Fundamental support improves when cash flow remains positive, margins stabilize, debt is manageable, dilution is limited, and the business still has a credible path to durable earnings. The setup deteriorates when the low multiple reflects shrinking demand, recurring write-downs, poor cash conversion, rising refinancing risk, or a business model losing relevance.

The useful distinction is between a temporary valuation discount and a permanently weaker business. Value investing requires both the discount and a defensible reason the business value has not fallen as much as the market price implies.

Common Mistakes in Value Investing

| Mistake | Safer interpretation |

|---|---|

| Equating low P/E with value | A low P/E ratio can reflect temporary pessimism, but it can also reflect falling earnings quality or lower future earnings power. |

| Ignoring cash flow | Reported earnings are weaker evidence when they do not convert into operating cash flow or free cash flow over time. |

| Treating margin of safety as a guarantee | A discount only helps if the value estimate is reasonable and the business risk has been counted honestly. |

| Underestimating deterioration | A stock can remain cheap when revenue quality, margins, leverage, or competitive position keep getting worse. |

FAQ

Is value investing the same as buying cheap stocks?

No. Value investing starts with apparent cheapness, but a valid value case also needs support from fundamentals, cash flow, balance-sheet quality, and realistic expectations.

What is intrinsic value in value investing?

Intrinsic value is an estimate of what a business may be worth based on its assets, earnings power, cash flow, durability, and future prospects. It is an estimate range, not a guaranteed number.

What makes a stock a value trap?

A stock can become a value trap when low valuation reflects real business deterioration, such as falling earnings, weak cash conversion, excessive debt, dilution, or structural decline.