Quality investing is a stock-selection style that favors companies with evidence of durable business strength, reliable earnings, cash-flow support, disciplined balance sheets, and efficient capital use. That evidence becomes more useful when it is tested against valuation, dilution, cyclicality, accounting quality, and expectation risk.

Definition: Quality investing means looking for companies whose business results appear durable, well supported by cash flow, and less dependent on fragile financing, aggressive accounting, or one-time conditions. It is an evidence lens for stock selection, not a conclusion that a stock is attractive at any price.

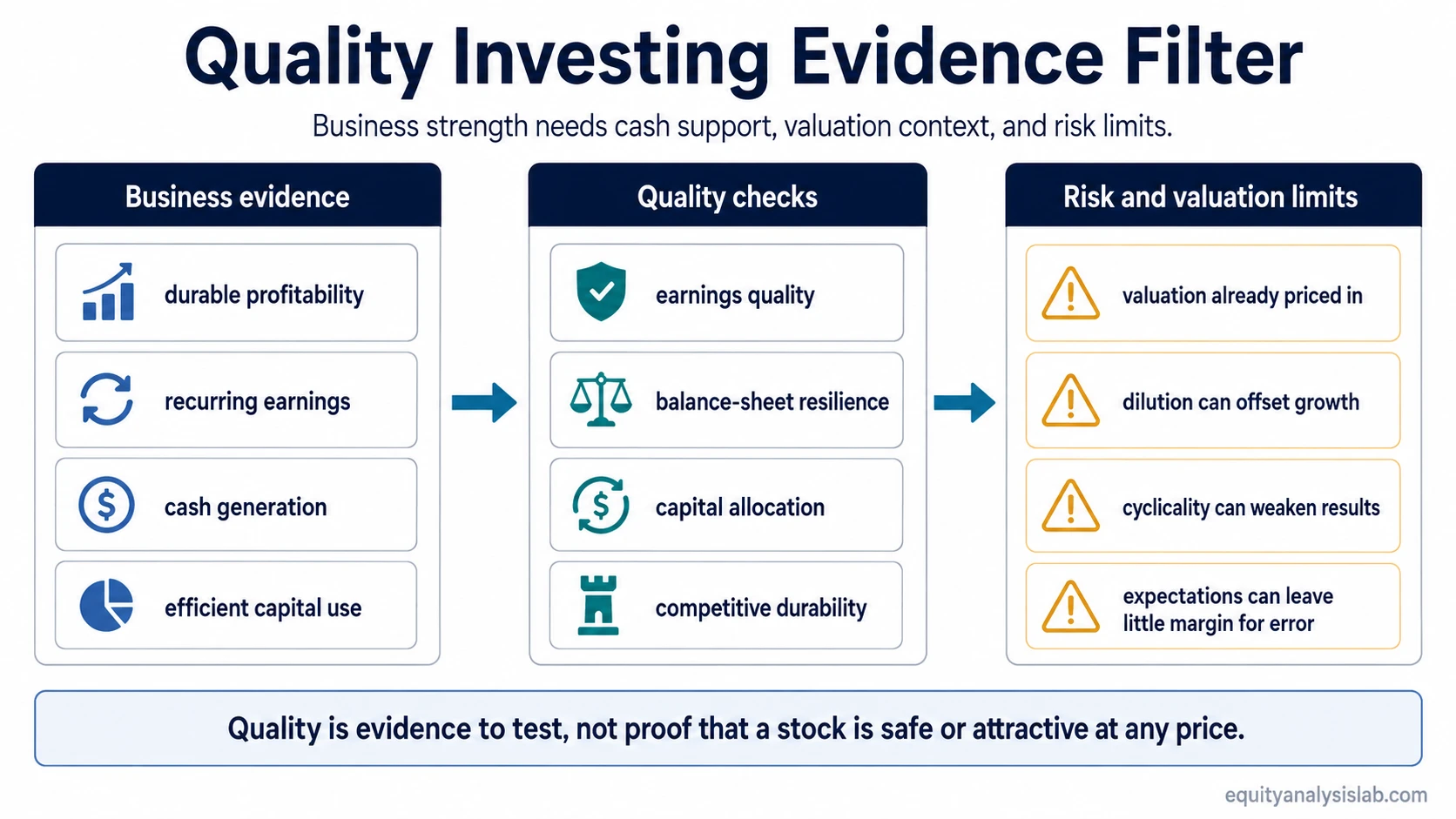

Key points about quality investing

- Quality investing focuses on business strength, earnings quality, cash conversion, balance-sheet resilience, and capital efficiency.

- Quality needs evidence from financial statements, not only a strong brand, stable narrative, or high market valuation.

- Quality does not remove valuation risk, downside risk, dilution risk, accounting risk, or cyclical risk.

- The strongest use of quality investing is diagnostic: it helps investors test whether a business deserves a higher level of confidence before valuation is considered.

What is quality investing?

Quality investing is an investment style that starts with the strength of the business rather than with price alone. It asks whether a company has durable profitability, reliable earnings, cash-flow support, prudent leverage, and a business model that can support results through changing conditions.

The style is often associated with companies that have strong margins, high returns on capital, stable earnings, conservative balance sheets, recurring demand, or disciplined capital allocation. Those traits can make a company easier to analyze, but they do not make the stock automatically safe or undervalued.

The practical boundary is simple: quality is evidence, not a verdict. A company can be high quality and still be overvalued, exposed to weakening demand, dependent on accounting adjustments, or priced for expectations that leave little room for error.

What evidence supports a quality investing label?

A quality reading becomes more useful when several types of evidence point in the same direction. A single high margin, strong brand, or stable earnings record is not enough if cash flow, leverage, dilution, or valuation tell a different story.

| Evidence area | What investors look for | What can weaken the quality reading |

|---|---|---|

| Profitability | Margins and returns that show the business can earn attractive profits without constant reinvention. | Margins that depend on temporary pricing, unusually low costs, or favorable cycle timing. |

| Earnings quality and stability | Reported earnings that appear recurring, understandable, and supported by the underlying business. | Earnings driven by adjustments, one-time gains, aggressive assumptions, or repeated exclusions. |

| Cash-flow support | Earnings that convert into operating cash flow or free cash flow over time. | Profit growth that is not matched by cash generation, especially when working capital or capital spending absorbs the reported earnings. |

| Balance-sheet strength | Debt levels, liquidity, and financing needs that allow the company to handle stress without fragile refinancing dependence. | High leverage, weak interest coverage, near-term refinancing pressure, or limited financial flexibility. |

| Capital efficiency | Returns on capital that suggest management can grow value without requiring excessive reinvestment. | Growth that consumes large amounts of capital while producing weak incremental returns. |

| Durability | A business model, customer base, competitive position, or cost structure that can support repeatable results. | Demand that fades, competitive pressure that rises, or returns that mean-revert after favorable conditions pass. |

| Capital allocation | Reinvestment, buybacks, dividends, or acquisitions that support per-share value without weakening the balance sheet. | Buybacks at stretched valuations, poor acquisitions, excessive stock compensation, or share issuance that dilutes owners. |

| Valuation context | Quality traits compared with the expectations already reflected in the share price. | A stock priced for flawless execution, leaving little margin for disappointment. |

How investors use quality investing

Investors use quality investing to separate stronger businesses from businesses that only look attractive because of a low price, a strong story, or a temporary earnings period. The style can help organize research around repeatability, financial resilience, and the connection between accounting profit and cash generation.

A quality-focused review usually asks whether earnings are durable, whether cash flow confirms the profit picture, whether leverage is manageable, and whether management decisions increase per-share value. These questions can narrow the research universe before deeper valuation work begins.

The style is most useful when it prevents false comfort. A business may look stable on the surface while free cash flow is weakening, share count is rising, or margins are peaking. In that case, the quality claim becomes a question to test rather than a reason to stop the analysis.

What quality investing is not

Not a valuation conclusion: A high-quality company can still trade at a price that already assumes years of strong execution.

Not a safety guarantee: Durable businesses can suffer from lower demand, weaker margins, management errors, leverage stress, or multiple compression.

Not a product screen: Quality investing can overlap with factor investing, but an investor-analysis approach should look beyond a simple factor label or fund category.

Not a recommendation: Quality evidence can support research, but it does not decide suitability, portfolio weight, expected return, or whether a stock should be purchased.

Not a trading signal: Quality investing is about business and financial evidence, not short-term entry timing or price-pattern confirmation.

Why quality still needs valuation and risk context

Quality can become expensive when many investors agree that a company is exceptional. A strong business may still produce a weak investment outcome if the starting valuation leaves no room for slower growth, margin pressure, weaker cash conversion, or a change in market expectations.

Limits of the quality label:

- Quality companies can be overpaid for when expectations become too optimistic.

- Quality does not remove downside risk from valuation compression, weaker earnings, or changing investor preferences.

- Earnings quality can be overstated when adjusted figures hide recurring costs or aggressive assumptions.

- Strong revenue growth can be diluted away if share issuance grows faster than per-share value.

- Cash flow matters more than narrative because reported profit is less useful when cash generation does not support it.

- Cyclical companies can look high quality near cycle peaks when margins, demand, and returns are temporarily elevated.

- Quality can lag lower-quality or higher-beta stocks during phases when markets reward risk appetite more than resilience.

- A quality label is an evidence input, not a final investment decision.

When a quality label becomes incomplete

A company may report stable earnings and high returns on capital for several years. At first glance, that looks like a quality profile. The interpretation changes if free cash flow is weakening, share count is rising, and the valuation already assumes flawless execution.

In that scenario, the quality label is not useless, but it is incomplete. The stronger question is whether the evidence still supports durability after cash conversion, dilution, balance-sheet resilience, and expectations are tested together.

Quality investing vs related investment styles

Quality investing overlaps with several stock-selection styles, but it asks a different first question. It starts with the strength and durability of the business, then checks whether the stock price and risk profile still make sense.

| Style | Main starting question | How it differs from quality investing |

|---|---|---|

| Growth investing | How much can the company expand? | Growth investing focuses on expansion expectations. Quality investing asks whether the business evidence is durable, cash-supported, and resilient enough to make those results credible. |

| GARP investing | Can growth be bought at a reasonable price? | GARP combines growth with valuation discipline. Quality investing focuses first on business and earnings quality, while still requiring valuation context before any conclusion. |

| Bottom-up investing | What does the company-level evidence show? | Bottom-up investing is a company-first research sequence. Quality investing is one style lens that can be used inside that sequence. |

| Value investing | Is price low relative to worth? | Value investing focuses on price versus estimated value. Quality investing focuses on business strength, but still cannot ignore price. |

| Factor investing | Does the stock fit a defined factor exposure? | Factor investing may treat quality as a measurable screen. A company-analysis approach also examines cash conversion, accounting quality, dilution, durability, and expectations. |

Quality investing FAQ

Is quality investing the same as buying safe stocks?

No. Quality investing looks for stronger business evidence, but strong companies can still face valuation risk, earnings disappointment, balance-sheet pressure, or changing market expectations.

Which metrics are common in quality investing?

Common metrics include margins, return on invested capital, return on equity, earnings stability, free cash flow, leverage ratios, and share-count trends. Metrics are more useful when they are interpreted together rather than treated as a simple screen.

Can a quality company be a poor investment?

Yes. A quality company can become unattractive if the stock price already assumes flawless execution, if cash flow weakens, if dilution offsets growth, or if the business is near a cyclical peak.