A value ETF is an exchange-traded fund that holds stocks selected for value characteristics, such as lower valuation ratios, discounted market pricing, or fundamentals that appear inexpensive relative to a chosen benchmark or peer group.

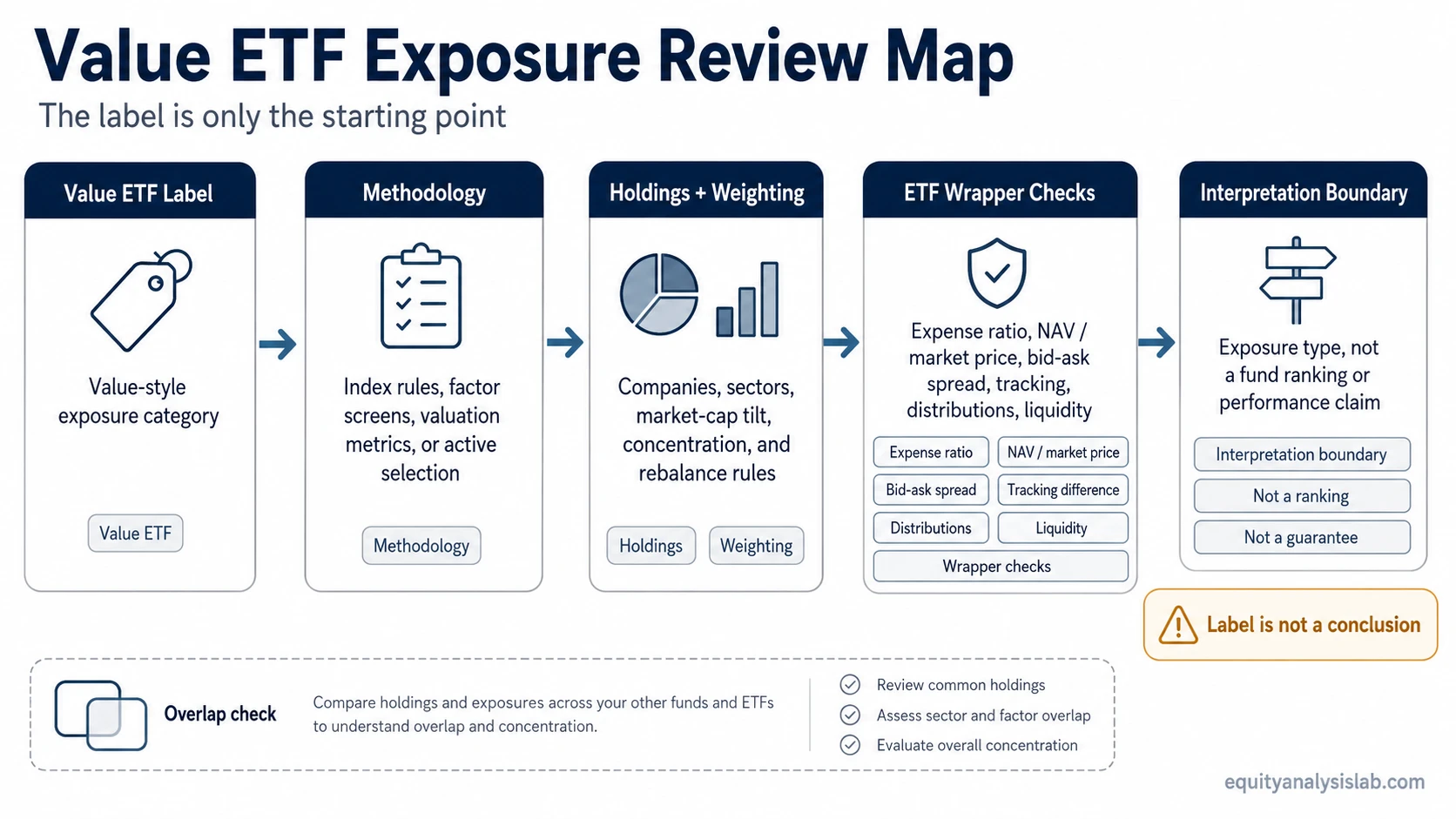

The value label is only the starting point. A value ETF still needs to be read through its methodology, holdings, weighting rules, costs, tracking behavior, distributions, liquidity, and tax context before the exposure is understood.

What Is a Value ETF?

A value ETF is an ETF that packages a portfolio of stocks with valuation-based characteristics. These characteristics are usually defined by an index provider, factor model, fundamental screen, or active manager rather than by a single universal rule.

One value ETF may emphasize low price-to-earnings ratios. Another may use book value, cash flow, dividend yield, sales, earnings quality, or a blended value score. A third may track a broad value index but still hold many large companies that also appear in broad market ETFs.

“Value ETF” describes an exposure category, not a complete investment conclusion. The useful question is how the value screen becomes actual portfolio exposure.

Key Points About Value ETFs

- A value ETF targets stocks with value characteristics, usually through index rules, factor screens, fundamental metrics, or active selection.

- The same label can produce different portfolios depending on methodology, weighting, rebalancing rules, and benchmark design.

- Holdings, sector exposure, company concentration, and market-cap tilt are often more revealing than the category name.

- ETF wrapper checks such as expense ratio, NAV, bid-ask spread, tracking difference, and distributions shape how the exposure is experienced.

- A value ETF is not automatically a dividend ETF, a cheaper ETF, a safer ETF, or a recommendation to own value stocks.

What the Value Label Does and Does Not Mean

The value label usually means the fund is designed to tilt toward stocks that look inexpensive under a defined set of metrics. It does not mean every holding is undervalued, that the fund is actively finding mispriced stocks, or that the ETF will outperform a growth or broad market fund.

A value ETF is different from a value investing strategy. A value investing strategy may involve company-by-company judgment, valuation work, margin-of-safety analysis, and qualitative business review. A value ETF normally turns value into a repeatable portfolio construction process.

A value ETF is also different from a dividend ETF. Some value portfolios may include dividend-paying companies, but dividend yield is not the same as value exposure. A fund can be value-oriented without being income-focused, and a dividend-oriented fund can hold companies that do not meet a strict value definition.

The distinction also matters when comparing value with growth. A growth ETF usually emphasizes companies with stronger growth characteristics, while a value ETF emphasizes lower valuation or value-style metrics. The full distinction belongs in a separate growth-vs-value ETF comparison, while this discussion stays focused on how value exposure is built and checked.

How Value ETFs Select Holdings

Value ETFs usually begin with a defined universe. That universe might be a broad market index, a large-cap index, a total market universe, a regional equity universe, or a narrower segment. The methodology then applies value-related rules to decide which stocks enter the portfolio and how much weight they receive.

| Methodology type | How it can define value exposure | What to check |

|---|---|---|

| Index-based value ETF | Tracks an index that separates value stocks from a broader equity universe. | Index provider rules, eligible universe, rebalancing schedule, and benchmark construction. |

| Factor-screened value ETF | Uses valuation ratios or composite factor scores to rank or filter holdings. | Which ratios are used, whether quality or profitability filters are included, and how scores are weighted. |

| Fundamental-weighted value ETF | Weights holdings by accounting or fundamental measures rather than only market capitalization. | Whether the weighting emphasizes earnings, book value, cash flow, dividends, sales, or another measure. |

| Actively managed value ETF | Uses manager discretion within an ETF wrapper to select or adjust value-oriented holdings. | Manager mandate, portfolio turnover, stated discipline, risk controls, and transparency level. |

An index ETF may define value through a rules-based benchmark, while an actively managed ETF may allow more discretion. Neither structure is automatically better. The important point is that the methodology determines what “value” means inside that fund.

What Holdings and Weighting Reveal

The holdings list is where the value label becomes concrete. Two funds can both be called value ETFs while holding different companies, different sector weights, different market-cap exposures, and different levels of concentration.

A large-cap value ETF may still be heavily exposed to mega-cap companies if those companies qualify under the index rules. Another fund may spread exposure across a larger number of holdings. A third may have a strong sector tilt because value screens can cluster in financials, energy, industrials, health care, or other areas depending on the market environment and methodology.

| Holding check | Why it matters | Interpretation boundary |

|---|---|---|

| Number of holdings | Shows whether exposure is broad or concentrated. | A larger holding count does not automatically mean better diversification if weights are still concentrated. |

| Top holding weight | Shows whether a few companies dominate the portfolio. | A fund can be labeled diversified while still relying heavily on a small group of stocks. |

| Sector exposure | Shows whether the value screen creates sector tilts. | Sector concentration may reflect methodology, not a separate sector call. |

| Market-cap exposure | Shows whether the fund is large-cap, mid-cap, small-cap, or blended. | Large-cap value and small-cap value can behave differently even when both use the value label. |

| Overlap with other ETFs | Shows whether the fund adds new exposure or reinforces existing positions. | A value ETF may overlap with broad market funds, dividend funds, or other style funds. |

Weighting rules often matter as much as selection rules. Market-cap weighting can give the largest qualifying companies the biggest influence. Equal weighting spreads weight more evenly but can increase turnover. Fundamental weighting may shift exposure toward companies with larger accounting measures. Score weighting may concentrate exposure in names with stronger value metrics.

ETF Wrapper Checks for a Value ETF

A value ETF is not only a value portfolio. It is also an ETF wrapper. The wrapper determines how the fund trades, how costs show up, how closely it follows its benchmark, and how investors experience distributions and taxable events.

| ETF wrapper check | What it tells you | Why it matters for a value ETF |

|---|---|---|

| Expense ratio | The ongoing fund fee charged by the ETF. | A value label does not mean the fund is automatically low-cost; the expense ratio still needs to be checked. |

| NAV and market price | The difference between the fund’s underlying value and its exchange-traded price. | NAV helps separate the portfolio’s underlying value from where the ETF trades during the market day. |

| Bid-ask spread | The gap between the price buyers offer and sellers ask. | A wider bid-ask spread can increase trading friction, especially in thinner or more specialized funds. |

| Premium or discount | Whether the ETF trades above or below its reported NAV. | Persistent or wide deviations can affect execution quality and interpretation of market price. |

| Volume and liquidity | How easily shares trade in the secondary market. | Liquidity should be reviewed separately from the value methodology because the exposure and the trading wrapper are different layers. |

These checks are not a product ranking. They keep the ETF wrapper visible beside the value methodology. A fund can have a clear value methodology and still require separate review of trading costs, liquidity, and fund mechanics.

Tracking, Distributions, and Tax Context

Many value ETFs are built to track a benchmark. The benchmark may be a large-cap value index, a broad market value segment, a factor index, or another rules-based portfolio. The fund’s actual results may differ from the benchmark because of fees, trading costs, replication choices, cash drag, securities lending, turnover, or timing differences.

Tracking difference is the gap between the ETF’s return and the return of the benchmark it is designed to follow. For benchmark-tracking value ETFs, this check matters because the investor is not only choosing a value screen; the investor is also choosing a fund that must implement that screen over time. For active value ETFs, review the mandate, holdings, turnover, and portfolio behavior rather than treating benchmark tracking as the whole analysis.

Distributions need separate interpretation. A value ETF may distribute dividends received from underlying holdings, but a higher distribution does not automatically mean stronger value exposure, better quality, or higher total return. Distribution yield can reflect sector composition, company payout policies, and the fund’s portfolio rules.

Tax Context Note

The general review point is structural: tax treatment depends on fund design and investor-specific circumstances, not on the value label alone. Specific tax questions require account-level and jurisdiction-specific review.

Common Mistake: Treating the Label as the Analysis

The most common mistake is assuming that “value ETF” already answers the important questions. It does not reveal which stocks qualify, how they are weighted, how often the fund rebalances, what sectors dominate, how much overlap exists with other funds, or what the wrapper costs are.

A second mistake is assuming that low valuation metrics automatically mean lower risk. Value screens can identify companies that are temporarily out of favor, but they can also include companies facing weak growth, cyclical pressure, balance-sheet stress, or business-model deterioration. A fund methodology may try to control for some of these issues, but the label cannot confirm that it does.

The value ETF label defines an exposure type. It does not determine suitability, attractiveness, or preference over another exposure.

Example Scenario: Same Label, Different Exposure

Consider two value ETFs that both use the same broad label. The first tracks a large-cap value index and weights holdings mostly by market capitalization. Its largest positions may dominate the fund, and its sector mix may look similar to a broad equity benchmark with a value tilt.

The second uses a deeper value screen with more emphasis on cash flow, book value, or earnings yield, then rebalances more aggressively. It may hold a different mix of companies, show higher turnover, and carry different tracking behavior even though the headline category is still “value ETF.”

The tempting shortcut is to treat both funds as interchangeable because the label matches. The stronger review separates the layers: value methodology first, then holdings and weighting, then ETF wrapper checks, then portfolio overlap and interpretation boundary.

How to Review a Value ETF Without Turning It Into a Ranking

A neutral review starts with structure, not preference. The goal is to understand what the ETF owns and how the wrapper works, not to declare a best fund.

| Review step | Question to ask | What the answer clarifies |

|---|---|---|

| Define the value methodology | Which metrics or rules decide what enters the fund? | Whether the fund is really a valuation screen, a style index, a blended factor fund, or an active value strategy. |

| Check the holdings | Which companies, sectors, and market caps dominate? | Whether the actual exposure matches the expected value category. |

| Review the weighting | Does the fund weight by market cap, equal weight, fundamentals, score, or manager discretion? | Which holdings drive the fund’s behavior. |

| Review wrapper costs | What are the recurring costs and trading frictions? | How implementation may affect investor experience. |

| Check tracking and distributions | How closely does the fund follow its benchmark, and what does it distribute? | Whether performance differences, dividends, or tax context need further review. |

| Check overlap | How much does the fund duplicate existing ETF exposure? | Whether the fund adds a new exposure or reinforces a position already present elsewhere. |

Related ETF Concepts

These related concepts clarify nearby ETF categories without repeating the same internal links already used in the article.

| Related concept | How it differs from a value ETF |

|---|---|

| Growth ETF | Targets growth-style characteristics rather than value-style characteristics. |

| Dividend ETF | Focuses on dividend-related characteristics; it may overlap with value but is not the same category. |

| Index ETF | Describes a rules-based tracking structure; a value ETF may be an index ETF if it follows a value index. |

| Actively managed ETF | Describes a manager-directed ETF structure; a value ETF may be active if a manager selects holdings rather than tracking a fixed index. |

| Growth-vs-value ETF | Owns the full comparison between the two style categories; value ETF analysis defines and interprets the value side. |

Value ETF FAQ

Is a value ETF the same as a cheap ETF?

No. A value ETF targets stocks with value-style characteristics. A cheap ETF usually refers to a fund with a low expense ratio. Those are different ideas.

Is a value ETF the same as a dividend ETF?

No. Some value ETFs may hold dividend-paying stocks, but dividend exposure and value exposure are not identical. A dividend ETF focuses on payout characteristics, while a value ETF focuses on valuation or value-style methodology.

Can two value ETFs hold different stocks?

Yes. Different value indexes, factor screens, weighting rules, and active management processes can produce different holdings even when the funds share the same value label.

Does a value ETF always outperform a growth ETF?

No. Performance depends on market conditions, methodology, holdings, costs, timing, and broader equity behavior. The value label does not guarantee better returns.