ETF dividends are cash or reinvestable distributions an exchange-traded fund passes to shareholders after receiving income from the securities it holds. The amount, timing, and tax classification of those distributions depend on the ETF’s holdings, distribution policy, fund structure, and the investor’s own tax context.

Definition: ETF dividends are distributions paid by an exchange-traded fund from income received by its underlying holdings. They are not the same as total return, fund quality, or a guarantee that the ETF is attractive.

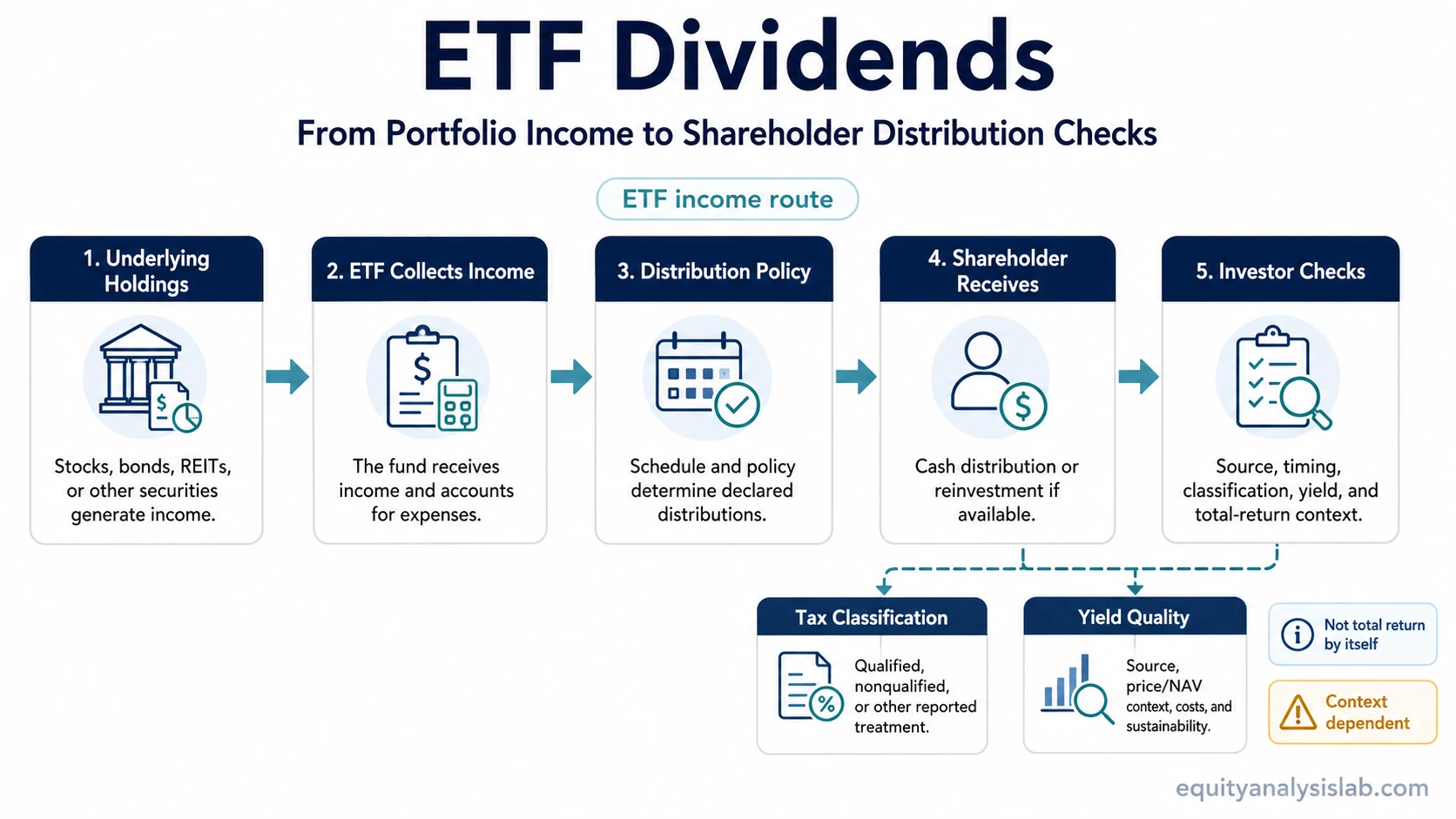

An ETF is a pooled fund. When companies, bonds, REITs, or other holdings inside the fund generate income, the ETF collects that income, accounts for fund expenses and policy rules, and may distribute part of it to shareholders. The shareholder receives the distribution as cash or, when available through the brokerage account, may reinvest it into additional shares.

Key Points

- ETF dividends usually come from income received by the fund’s underlying holdings.

- Distribution schedules vary by fund and do not make the dividend amount guaranteed.

- Qualified and nonqualified dividend treatment can affect how distributions are taxed.

- Dividend yield needs source, sustainability, price, and NAV context before it is useful.

- Dividend distributions should be separated from capital gains distributions.

What Are ETF Dividends?

ETF dividends are the shareholder-facing result of income collected inside the fund. For an equity ETF, that income may come from dividends paid by companies in the portfolio. For a bond ETF, regular payments may be interest-like rather than stock dividends. For a REIT ETF, distributions may carry different tax characteristics than ordinary corporate dividends.

The word “dividend” can therefore hide several moving parts. The investor sees a distribution, but the source may differ across equity funds, bond funds, REIT funds, high-yield strategies, dividend-growth strategies, and income-oriented portfolios. The label alone does not answer whether the distribution is durable, tax-efficient, or supported by the fund’s underlying holdings.

Dividend ETFs are funds that emphasize dividend-paying holdings. That category is related to ETF dividends, but it is not the same concept. A dividend ETF describes a fund strategy or selection style; ETF dividends describe the actual distribution mechanics that move income from holdings, through the fund, and then to shareholders.

How ETF Dividend Distributions Work

The mechanics are easiest to read as a chain. Holdings generate income first. The ETF receives that income at the fund level. The fund applies its distribution policy, expense structure, and schedule. Shareholders then receive a distribution if the fund declares one.

| Step | What Happens | Investor Check |

|---|---|---|

| Underlying holdings | Stocks, bonds, REITs, or other securities generate income inside the portfolio. | Check what the fund actually owns, not only the headline yield. |

| Fund collection | The ETF receives income from those holdings and accounts for fund expenses. | Review expense ratio, index method, and fund reports. |

| Distribution policy | The ETF follows its stated schedule and policy for declaring distributions. | Check whether distributions are monthly, quarterly, annual, variable, or irregular. |

| Shareholder distribution | The investor receives cash or may reinvest through the account if reinvestment is available. | Separate cash received from total return and after-tax result. |

The distribution may feel simple at the account level, but the analytical work sits underneath it. A high cash payout may come from strong portfolio income, a concentrated yield strategy, changing market prices, or a distribution pattern that deserves closer inspection.

Qualified and Nonqualified ETF Dividends

ETF dividends may be classified differently for tax purposes. Some distributions may qualify for preferential dividend treatment, while others may be nonqualified or treated differently because of the fund’s holdings, holding-period rules, security type, account type, and jurisdiction.

The same cash amount can lead to different after-tax results. A distribution from a broad equity ETF, a bond ETF, a REIT ETF, and a high-yield income ETF may not receive the same tax treatment. Fund tax documents, brokerage tax forms, and local tax rules determine how the distribution is ultimately reported.

Tax boundary: ETF dividend tax treatment is context-dependent. Fund documents can clarify how distributions were reported, but personal tax consequences depend on account type, holding period, residence, and applicable rules. This is educational context, not tax advice.

Dividend ETFs, Yield, and Distribution Quality

A dividend ETF may focus on companies with high current yields, companies with a record of dividend growth, or an index methodology that blends income with quality, size, sector, or volatility screens. These approaches can produce very different distribution profiles even when the fund names sound similar.

High yield is not automatically better than lower yield. A high yield can reflect strong income, but it can also reflect price decline, sector concentration, weaker business quality, credit stress, or a payout pattern that may not be sustainable. Dividend growth strategies may offer lower current yield while focusing on companies that have increased dividends over time, but that does not remove valuation, concentration, or business-risk concerns.

A dividend label is only the starting point. The next review is the distribution source, portfolio holdings, costs, tracking behavior, liquidity, and tax reporting.

| Check | Why It Matters | Common Misread |

|---|---|---|

| Holdings | Dividend quality starts with the securities producing the income. | Judging the fund only by its yield percentage. |

| Yield source | Yield can rise because income increases or because price falls. | Treating a higher yield as automatic improvement. |

| Distribution schedule | Monthly, quarterly, and annual schedules change cash-flow timing. | Assuming every ETF distributes on the same pattern. |

| Expense ratio | Costs reduce the fund return available to shareholders. | Ignoring the drag between portfolio income and investor result. |

| Tracking behavior | The fund may not perfectly match its index or stated strategy. | Assuming the label fully describes the outcome. |

| Liquidity | Trading spreads and fund size can affect implementation quality. | Looking only at income and ignoring execution friction. |

| Tax documents | Final classification may differ from a simple dividend label. | Assuming all distributions are taxed the same way. |

ETF Dividends vs Capital Gains Distributions

ETF dividends usually relate to income received by the fund’s holdings. ETF capital gains distributions relate to realized gains that the fund passes through after selling securities or otherwise recognizing gains at the fund level.

The distinction matters because two distributions can arrive in the same account and still come from different sources. One may reflect dividend or interest income from holdings. Another may reflect realized gains inside the ETF. The investor needs to separate source, timing, and tax reporting before interpreting the distribution.

ETF Dividends and Tax Efficiency Context

Dividend distributions are one part of the broader ETF tax picture. Fund structure, turnover, creation-redemption mechanics, dividend classification, capital gains distributions, account type, withholding tax, and jurisdiction can all affect after-tax results.

That broader lens belongs to ETF tax efficiency context, where the focus shifts from one distribution source to the overall relationship between fund design, taxable events, and investor account conditions.

Important boundary: An ETF can be efficient in one context and less efficient in another. Dividend treatment, fund turnover, account wrapper, withholding rules, and investor location can change the final result.

Simple ETF Dividend Example

An equity ETF owns a basket of dividend-paying companies. Several holdings pay dividends during the quarter. The ETF collects that income, accounts for fund expenses, and declares a quarterly distribution to shareholders according to its policy.

The shareholder receives cash or reinvests through the brokerage account if reinvestment is available. That cash distribution does not by itself prove that the ETF is higher quality, more tax-efficient, or likely to produce a better total return. The next checks are the holdings, yield source, price or NAV behavior, distribution classification, and fit within the investor’s account context.

Limits Investors Should Check

ETF dividends are useful to understand, but they are easy to overread. A dividend can support cash-flow planning, but it does not eliminate market risk, business risk, interest-rate risk, concentration risk, or tax uncertainty.

Common mistake: Reading dividend yield as a complete answer. Yield is a distribution measure, not a full return measure, quality score, or tax conclusion. A cash distribution can be offset by price decline, NAV decline, weak underlying holdings, higher costs, or less favorable tax treatment.

A stronger review separates four questions: what generated the income, how the ETF distributed it, how the distribution was classified, and whether the fund’s total behavior still fits the investor’s objective. Those questions keep the dividend label from replacing the actual analysis.

FAQ

Do all ETFs pay dividends?

No. Some ETFs distribute income regularly, some distribute only when holdings generate distributable income, and some may have little or no dividend income depending on their strategy and holdings.

Are ETF dividends guaranteed?

No. ETF dividends depend on the income generated by the fund’s holdings, the fund’s distribution policy, and market conditions. Distribution amounts can change.

Are ETF dividends always qualified dividends?

No. Qualification depends on the underlying securities, holding-period rules, fund structure, and tax reporting. Bond ETF payments, REIT ETF distributions, and other income types may be treated differently.

Is dividend yield the same as total return?

No. Dividend yield measures cash distributions relative to price. Total return also includes price or NAV changes and can be reduced by costs, taxes, and market declines.