ETF tax efficiency describes how ETF structure can reduce or defer some fund-level taxable distributions, especially capital gains, but it does not remove investor taxes or make every ETF equally efficient.

The concept matters most in taxable accounts, where fund-level distributions can create tax events for shareholders. In tax-deferred or tax-exempt accounts, the same ETF mechanics may still matter for cost, tracking, liquidity, and portfolio exposure, but the tax-efficiency question usually has a different practical weight.

ETF tax efficiency should be read as a wrapper-and-portfolio behavior, not as a simple quality label. Structure, turnover, asset class, distribution policy, dividend treatment, liquidity, and account type all shape whether the tax-efficiency advantage is meaningful for a specific investor situation.

Key Points

- ETF tax efficiency usually means fewer or deferred fund-level taxable distributions, especially capital gains distributions.

- The main structural mechanism is the ETF creation and redemption process, including in-kind transfers through authorized participants.

- Tax efficiency does not eliminate dividends, investor-level taxes, jurisdiction differences, or strategy-specific tax effects.

- Turnover, asset class, distribution history, tracking, costs, liquidity, and account type still need to be checked before treating an ETF as tax efficient.

What ETF Tax Efficiency Means

ETF tax efficiency is the ability of an exchange-traded fund structure to reduce the frequency or size of taxable fund-level distributions compared with structures that must sell holdings more directly to meet shareholder activity. The strongest version of this advantage is usually tied to capital gains distributions, not to a promise that the investor will owe no tax.

A taxable event can still occur when an investor sells ETF shares for a gain, receives dividends, or holds a fund that distributes income or realized gains. The ETF wrapper can change how some fund-level events are handled, but it does not erase the tax character of the underlying holdings or the investor’s own account situation.

The useful distinction is between tax efficiency as a structural tendency and tax efficiency as a final investor outcome. A fund can have tax-efficient mechanics and still be a poor fit if its exposure, turnover, costs, liquidity, tracking behavior, or distribution profile does not match the investor’s broader analysis.

Why ETF Structure Can Reduce Capital Gains Distributions

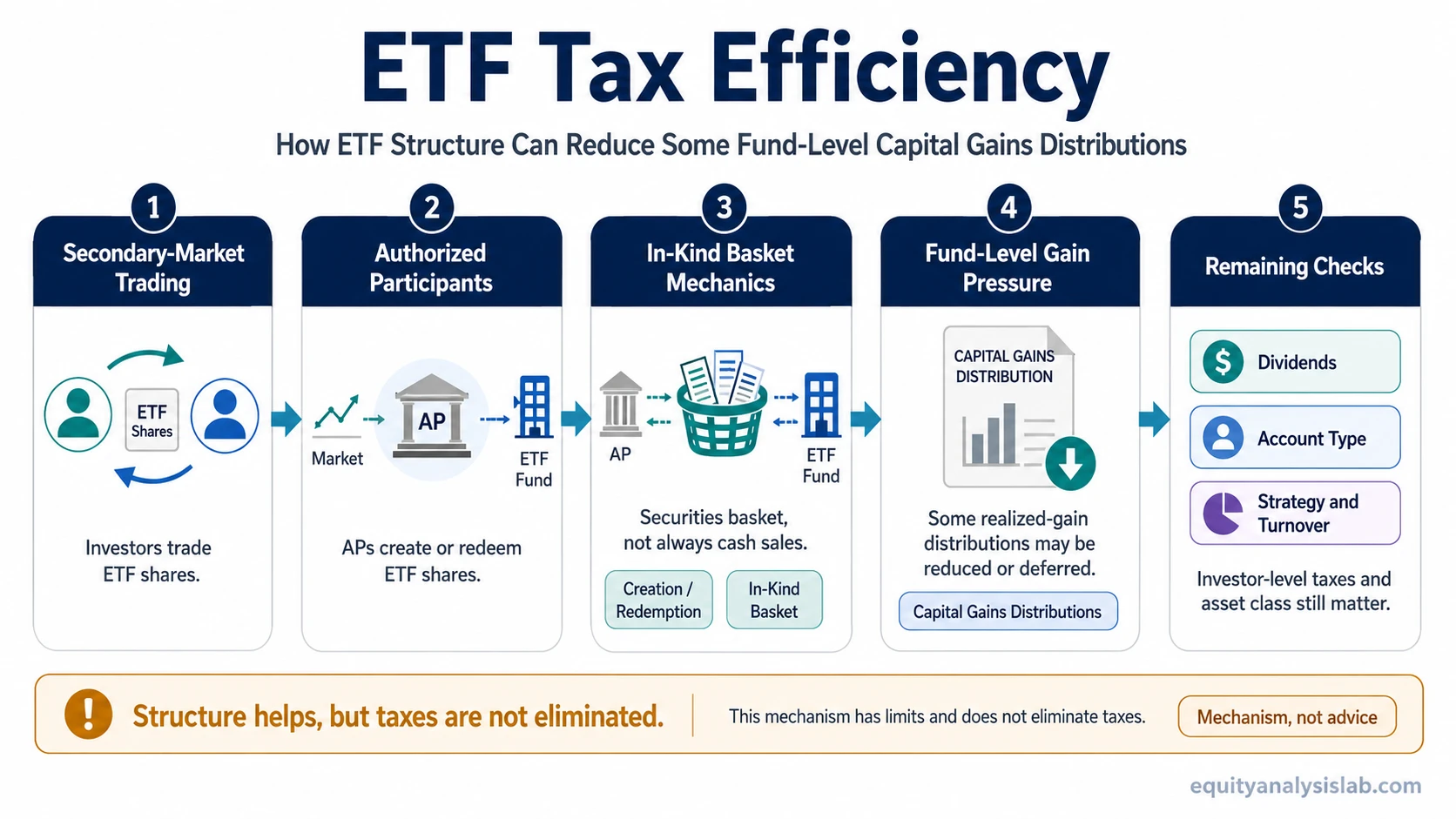

ETF shares trade on an exchange between buyers and sellers during the market day. Many shareholder transactions therefore happen in the secondary market, without requiring the fund itself to sell portfolio holdings each time an investor enters or exits.

The primary market is different. Large institutional participants, commonly called authorized participants, can create or redeem ETF shares in large blocks. In many ETF structures, this process can involve in-kind transfers of securities rather than a simple cash sale of the fund’s holdings.

That structure can help the ETF manage portfolio adjustments without realizing the same pattern of fund-level gains that might occur if the fund had to sell appreciated securities directly to meet ordinary investor redemptions. The result can be fewer taxable capital gains distributions passed through to shareholders, although the exact result depends on the fund’s structure, holdings, strategy, and applicable tax rules.

This is why ETF capital gains distributions are central to the tax-efficiency discussion. The key question is not whether the ETF can ever distribute gains, but whether its structure and portfolio behavior make those distributions less frequent, smaller, or more deferred than they otherwise might be.

How Secondary-Market Trading and In-Kind Redemptions Work Together

ETF tax efficiency comes from the interaction between two layers. The first layer is secondary-market trading, where investors buy and sell ETF shares with each other. The second layer is the creation and redemption process, where authorized participants interact with the fund to keep ETF share supply aligned with market demand.

| Layer | What happens | Why it matters for tax efficiency |

|---|---|---|

| Secondary-market trading | Investors trade ETF shares with other market participants. | The ETF does not have to sell portfolio holdings for every shareholder transaction. |

| Creation | Authorized participants deliver a basket of securities or cash to receive ETF shares. | This helps align ETF share supply with demand without ordinary investors forcing portfolio sales. |

| Redemption | Authorized participants return ETF shares and may receive a basket of securities. | In-kind redemptions can reduce the need for the fund to sell appreciated holdings directly. |

| Portfolio management | The ETF can manage baskets, holdings, and cash positions within the fund structure. | The actual tax outcome depends on turnover, holdings, strategy, and fund rules. |

The structural point is not that ETF taxation disappears. It is that the ETF wrapper can separate many shareholder trades from direct fund-level sales. When redemptions can be handled through in-kind baskets, some appreciated securities may leave the fund without creating the same taxable distribution pattern for remaining shareholders.

What Can Affect ETF Tax Efficiency

ETF tax efficiency is not identical across all funds. The wrapper matters, but the portfolio inside the wrapper also matters. A low-turnover equity index ETF may behave differently from an actively managed ETF, a bond ETF, a commodity-linked ETF, or a fund using derivatives or frequent rebalancing.

| Driver | Why it matters | What to check |

|---|---|---|

| Turnover | More buying and selling inside the fund can create more opportunities for realized gains. | Portfolio turnover, strategy style, rebalancing frequency, and distribution history. |

| Asset class | Equity, bond, commodity, option, and derivative-based funds can have different tax and distribution profiles. | Underlying exposure, income type, structural rules, and fund documentation. |

| Dividends and income | Tax-efficient capital gains mechanics do not eliminate income produced by holdings. | Dividend yield, interest income, distribution schedule, and reported tax character. |

| Account type | Taxable, tax-deferred, and tax-exempt accounts can change how distributions affect the investor. | Whether the investor is evaluating after-tax outcomes in a taxable account or a tax-advantaged account. |

| Fund structure | Not every exchange-traded product has the same structure or tax treatment. | ETF type, legal structure, use of cash redemptions, derivatives, and fund disclosures. |

The tax-efficient label is only a starting point. Two ETFs can share the same wrapper while producing different distribution patterns because their holdings, turnover, strategy, liquidity, and account context differ.

ETF Tax Efficiency, Dividends, and Other Distributions

Capital gains distributions are only one part of the tax-efficiency discussion. ETFs may also distribute dividends, interest, or other income generated by the securities they hold. Those payments can still create taxable income for shareholders in taxable accounts.

This is why ETF dividend distributions should be separated from capital-gains efficiency. A fund can be efficient at limiting capital gains distributions while still passing through income from the portfolio.

Qualified dividend treatment is a separate classification question. It can depend on the nature of the dividend, fund reporting, account type, investor context, and applicable rules. It should not be collapsed into the broader claim that an ETF is tax efficient.

A Simple Taxable-Account Scenario

Suppose two funds hold similar appreciated stocks. One fund must sell securities directly to meet redemptions, while the ETF can handle some large redemptions through an in-kind process. The first fund may be more likely to realize gains that are distributed to shareholders. The ETF may be able to reduce or defer some of that fund-level gain pressure.

That scenario does not mean the ETF investor avoids tax. If the ETF distributes dividends, those payments can still be taxable. If the investor later sells ETF shares above cost, the investor may still realize a capital gain. The structural advantage is mainly about how some fund-level gains may be managed before they become shareholder distributions.

When ETF Tax Efficiency Can Be Limited

ETF tax efficiency weakens when the structural advantage is offset by the fund’s holdings, strategy, or account context. The ETF wrapper can help, but it does not turn every fund into a low-tax outcome.

- High portfolio turnover can create more realized gains inside the fund.

- Income-heavy holdings can still generate taxable distributions.

- Some asset classes and product structures may have different tax treatment.

- Cash redemptions or unusual portfolio conditions can reduce the in-kind advantage.

- Tax-advantaged accounts can change the relevance of distribution efficiency.

- Investor-level sale decisions still determine whether the investor realizes gains or losses on ETF shares.

The practical mistake is treating ETF tax efficiency as a guarantee rather than a feature to examine. A careful review still needs the fund’s distribution history, strategy, holdings, turnover, structure, and account context.

ETF Tax Efficiency vs Mutual Fund Tax Efficiency

ETF tax efficiency is often discussed in contrast with mutual funds because the two structures can handle shareholder activity differently. Traditional mutual funds may need to sell holdings to meet shareholder redemptions, which can create realized gains that are distributed across remaining shareholders. ETFs often rely more heavily on secondary-market trading and authorized participant activity.

That contrast is useful, but it should remain limited. Some mutual funds can be managed with tax awareness, and some ETFs can still distribute taxable gains or income. The comparison should not be reduced to “ETF good, mutual fund bad.” The relevant distinction is how structure, strategy, holdings, distribution behavior, and account context affect the tax profile.

Related Concepts to Separate

| Concept | How it differs from ETF tax efficiency |

|---|---|

| Capital gains distributions | These are taxable distributions from realized fund-level gains. ETF tax efficiency often focuses on reducing or deferring this specific distribution type. |

| Dividends | Dividends come from income generated by underlying holdings. They can still be paid even when capital gains distributions are low. |

| Expense ratio | Expense ratio is a fund cost measure, not a tax-efficiency measure. A low-cost fund can still have taxable distributions. |

| Tracking difference | Tracking difference measures how closely the fund follows its benchmark after costs and operations. It is related to implementation quality, not the same as tax efficiency. |

| After-tax return | After-tax return depends on the investor’s account type, tax rules, holding period, sale decision, distributions, and fund behavior. ETF tax efficiency is only one input. |

FAQ

Is ETF tax efficiency the same as avoiding taxes?

No. ETF tax efficiency usually refers to reducing or deferring some fund-level taxable distributions, especially capital gains. Investors may still owe tax on dividends, other distributions, or gains when they sell shares, depending on account type and applicable rules.

Does ETF tax efficiency matter in tax-deferred accounts?

It usually matters less than it does in taxable accounts because the account wrapper can change how taxes are handled. ETF costs, exposure, tracking, liquidity, and distribution behavior can still matter for investment analysis.

Are ETFs always more tax efficient than mutual funds?

No. ETFs often have structural advantages, but tax efficiency depends on the fund’s holdings, turnover, strategy, redemption mechanics, distributions, and investor context. Some ETFs can still distribute taxable income or capital gains.

Why do ETFs still pay dividends?

ETFs hold underlying assets. If those assets generate dividends, interest, or other income, the fund may pass that income through to shareholders. Capital-gains efficiency does not remove the income profile of the holdings.