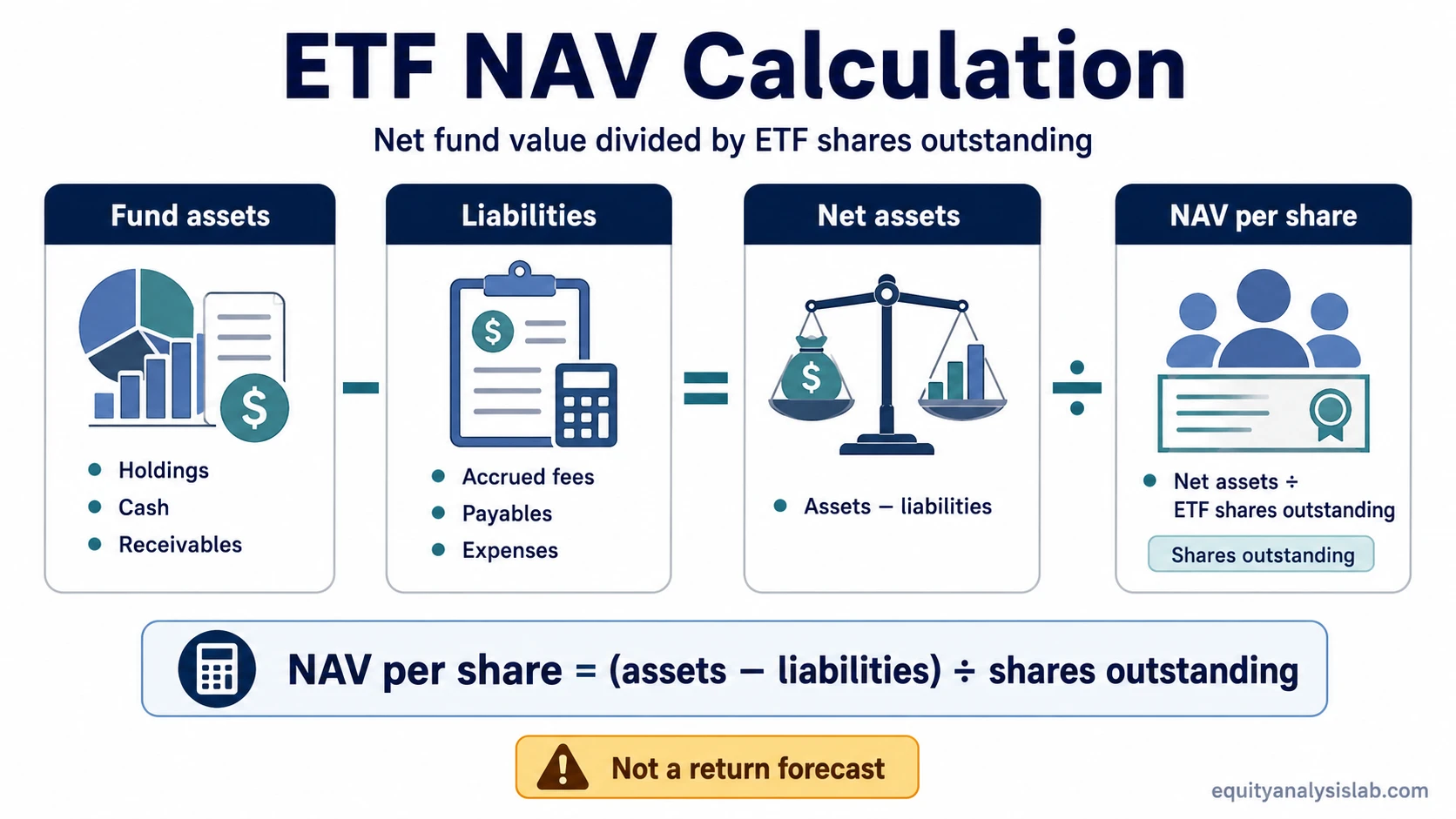

NAV in an ETF means net asset value: the fund’s net portfolio value per share after subtracting liabilities from assets and dividing by shares outstanding.

ETF NAV formula: NAV per share = (total fund assets − fund liabilities) ÷ ETF shares outstanding.

NAV is a reference value for the ETF’s underlying portfolio. It is not a quality rating, a return forecast, or a conclusion that the ETF is cheap or expensive.

Key points about ETF NAV

- ETF NAV is the fund’s net portfolio value per share.

- The basic formula is assets minus liabilities, divided by shares outstanding.

- An ETF’s market price can trade above or below its NAV.

- NAV can be stale when underlying markets are closed or holdings are harder to price.

- NAV is useful, but a full ETF review also checks costs, tracking, liquidity, distributions, and tax details.

What NAV means in an ETF

ETF NAV is the per-share value of the fund’s net assets. It starts with the value of the ETF’s portfolio holdings, adds other fund assets such as cash or receivables, subtracts liabilities and accrued expenses, and then divides the result by the number of ETF shares outstanding.

For an ETF investor, NAV acts as a portfolio-value reference. It helps separate the value of the fund’s underlying basket from the price at which ETF shares trade on an exchange. That distinction matters because ETF shares can change hands during the trading day while the reported NAV is commonly based on portfolio values calculated after market close.

NAV is most useful when it is treated as a starting reference. It does not say whether the ETF’s strategy is attractive, whether the holdings are high quality, whether the expense ratio is reasonable, or whether the fund fits a portfolio objective.

How ETF NAV is calculated

The standard ETF NAV calculation follows a simple structure:

NAV per share = (assets − liabilities) ÷ shares outstanding

The simplicity of the formula can hide several practical details. The asset side depends on how the fund’s holdings are valued. The liability side can include accrued fees, payables, and other obligations. The share count can also change when ETF shares are created or redeemed through the fund’s primary-market process.

For most diversified equity ETFs, the headline calculation is straightforward. The interpretation becomes more nuanced when the ETF holds securities that trade in different time zones, bonds with less frequent pricing, derivatives, or assets where market quotes are less current.

What goes into ETF NAV

ETF NAV is not based only on the last quoted price of the ETF itself. It is based on the fund’s internal portfolio accounting.

| NAV input | What it represents | Why it matters |

|---|---|---|

| Portfolio holdings | Stocks, bonds, derivatives, or other assets held by the ETF | The largest driver of the fund’s asset value |

| Cash and receivables | Cash balances, dividends receivable, interest receivable, or settlement items | These can affect net assets even when holdings are unchanged |

| Liabilities | Payables, accrued management fees, operating expenses, or other obligations | Liabilities reduce the net value available to shareholders |

| Shares outstanding | The number of ETF shares currently outstanding | The net asset value is divided across this share count |

| Pricing methodology | The method used to value holdings when direct market prices are unavailable or less current | Pricing method can affect how current or representative the NAV appears |

The exact inputs depend on the ETF’s structure and holdings. A plain equity ETF, a bond ETF, a commodity-linked ETF, and an international ETF may all report NAV, but the pricing questions behind that number can differ.

When ETF NAV is calculated and why it can be stale

ETF NAV is commonly calculated after the market close using available portfolio values. That makes NAV a useful official reference, but it may not always match real-time trading conditions during the day.

Stale NAV risk appears when the reported portfolio value is based on prices that are no longer fully current. This can happen when an ETF holds international securities whose local markets closed before the ETF trades in the investor’s market. It can also matter for fixed-income holdings, thinly traded securities, or assets where pricing depends on estimates rather than continuous exchange trading.

Stale NAV does not mean useless NAV

A stale NAV can still be a valid fund-accounting reference. The limitation is interpretation. A gap between market price and NAV may reflect timing, liquidity, pricing estimates, or new information since the underlying holdings last traded.

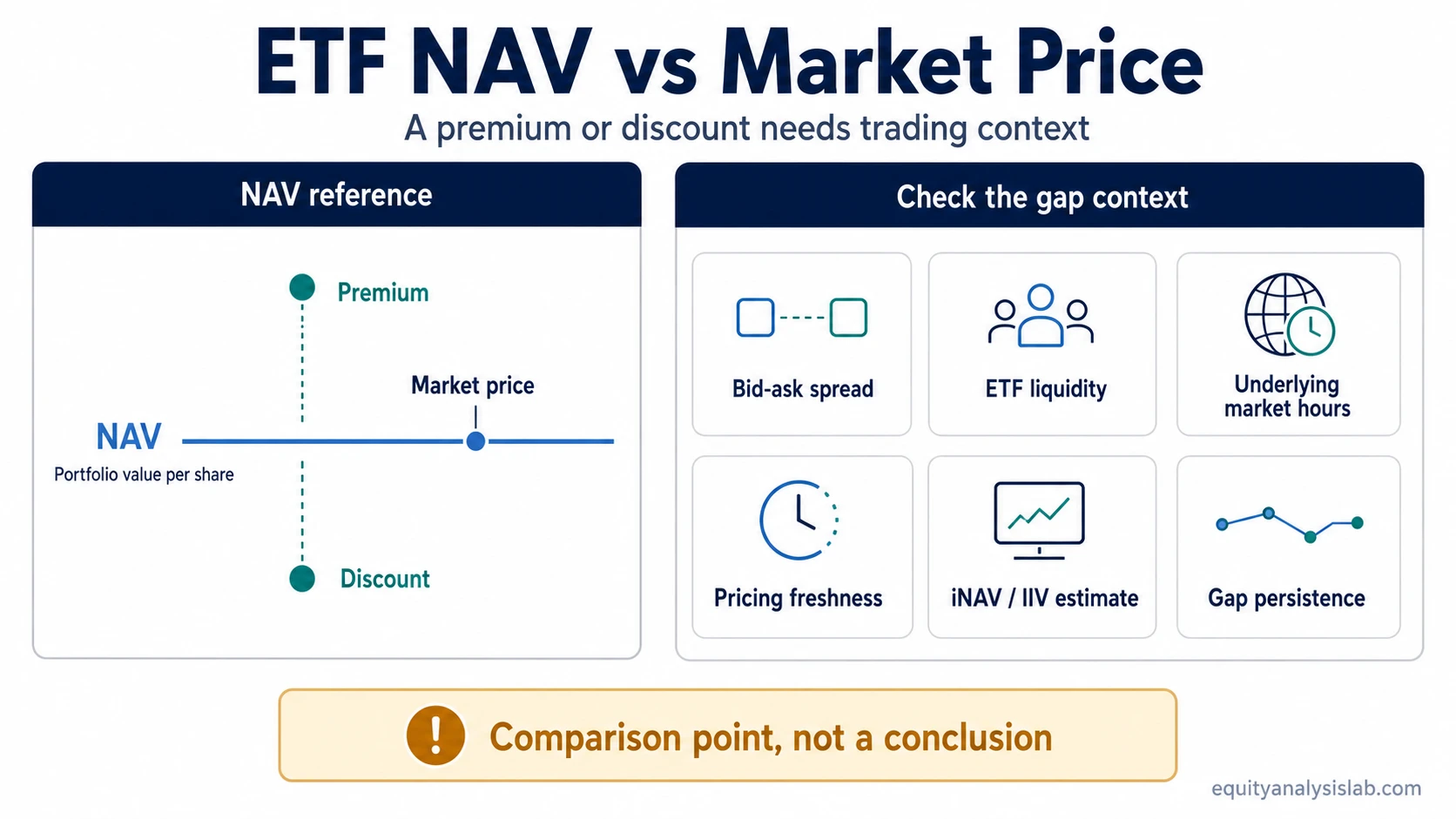

NAV vs market price in an ETF

ETF NAV and ETF market price are related, but they are not the same number. NAV is the fund’s calculated net portfolio value per share. Market price is the price at which ETF shares trade on an exchange.

| Item | What it measures | How it is used |

|---|---|---|

| NAV | The ETF’s net asset value per share | Reference point for the value of the underlying portfolio |

| Market price | The exchange-traded price of the ETF share | Price available to buyers and sellers during trading hours |

| Bid-ask spread | The gap between the price buyers bid and sellers ask | Transaction-cost context around the quoted market price |

The bid-ask spread can matter when comparing NAV with the price available in the market. A market price near NAV can still be costly to trade if the spread is wide, while a small premium or discount may be less meaningful when normal spreads, timing, and liquidity conditions are considered.

Premium, discount, and iNAV in context

An ETF trades at a premium when its market price is above NAV. It trades at a discount when its market price is below NAV. A premium or discount is a comparison point, not a complete investment conclusion.

A small gap can reflect normal trading conditions, timing differences, or bid-ask spread effects. A larger or persistent gap deserves more context: underlying market hours, fund liquidity, holdings transparency, creation/redemption conditions, and whether the ETF’s portfolio is easy to price.

Some ETFs also publish an intraday indicative value, often called iNAV or IIV. This is an estimated intraday reference based on available information. It can help investors compare market price with an updated value indication, but it is still an estimate and may be less reliable when holdings are illiquid, foreign markets are closed, or pricing inputs are incomplete.

What investors should check beyond NAV

NAV helps identify the fund-value reference, but it does not replace a broader ETF review. A better review compares the ETF’s reported value, traded price, costs, and structure together.

| Check | Question to ask | Why it matters |

|---|---|---|

| Holdings | What assets actually drive the NAV? | NAV only means something when the underlying exposure is understood |

| Index or strategy | What is the ETF designed to track or implement? | The same NAV number can represent very different exposures |

| Expense ratio and costs | How much value is lost to ongoing fund costs? | Costs can affect long-term investor outcomes even when NAV tracking looks clean |

| Tracking behavior | How closely does the ETF follow its benchmark or stated strategy? | NAV can be accurate while the strategy still tracks imperfectly |

| Liquidity and trading conditions | Can ETF shares be traded without unusually wide spreads or poor depth? | ETF liquidity conditions affect the practical price available to investors |

| Distributions | Are dividends, interest, or capital gains affecting the fund’s value path? | Distribution timing can change how NAV and returns are interpreted |

| Tax and structure notes | Are there fund-specific tax, distribution, or structural details? | Tax treatment can vary by investor and jurisdiction, so fund documents and qualified tax guidance matter |

A practical ETF NAV scenario

An investor sees an ETF trading slightly above its last reported NAV. The quick conclusion would be to call the ETF expensive, but the better diagnostic sequence is slower.

The investor first checks when the NAV was calculated. If the ETF holds foreign securities, the underlying market may have closed hours earlier. If the ETF holds bonds or less liquid securities, some holdings may not have fresh exchange prices. The investor then checks the current spread, available liquidity, any iNAV or IIV estimate, and whether the ETF’s holdings have moved since the last official NAV calculation.

The premium may still matter, especially if it is large or persistent. The point is that the NAV gap needs context before it becomes a judgment about the ETF.

What NAV can and cannot tell you

Common mistake: A lower ETF NAV does not mean the ETF is cheaper in a valuation sense. NAV is a per-share portfolio value, not a price-to-value ratio like a stock valuation metric.

| NAV can help with | NAV cannot tell you by itself |

|---|---|

| Understanding the fund’s net portfolio value per share | Whether the ETF is a good investment |

| Comparing market price with a portfolio-value reference | Whether a premium is automatically bad or a discount is automatically good |

| Identifying timing or pricing questions in the fund | Whether the fund’s holdings, strategy, or costs are attractive |

| Spotting when more context is needed | Whether future returns will be positive or negative |

The useful interpretation is diagnostic. NAV helps frame the next questions: what the ETF owns, how those holdings are priced, how the ETF trades, and whether the gap between NAV and market price is temporary, persistent, or explainable.

Related ETF concepts

NAV connects to several ETF mechanics, but each concept answers a different question.

| Concept | How it relates to NAV |

|---|---|

| ETF creation and redemption process | Explains how ETF shares can be created or redeemed through the primary market, which helps connect fund shares with underlying portfolio value. |

| ETF arbitrage mechanism | Explains how institutional activity can help reduce large gaps between ETF market price and portfolio value, without making the process a retail trading tactic. |

| ETF liquidity conditions | Explains why the ease of trading ETF shares and the liquidity of underlying holdings can affect how market price relates to NAV. |

| Bid-ask spread | Explains the transaction-cost gap around the ETF’s quoted market price. |

FAQ

Is ETF NAV the same as ETF price?

No. ETF NAV is the fund’s calculated net asset value per share. ETF price is the exchange-traded market price. The two are related, but they can differ during trading hours.

Does a low ETF NAV mean the ETF is cheap?

No. A lower NAV does not mean better value by itself. ETF NAV is a per-share accounting value for the fund’s portfolio, not a valuation multiple or return forecast.

Why can an ETF trade above or below NAV?

An ETF can trade above or below NAV because market price is set by buyers and sellers during trading hours, while NAV is calculated from portfolio values. Timing differences, spreads, liquidity, and underlying market conditions can all affect the gap.

Is iNAV a perfect real-time ETF value?

No. iNAV or IIV is an intraday estimate. It can be useful, but it may be less accurate when holdings are illiquid, markets are closed, or pricing inputs are incomplete.