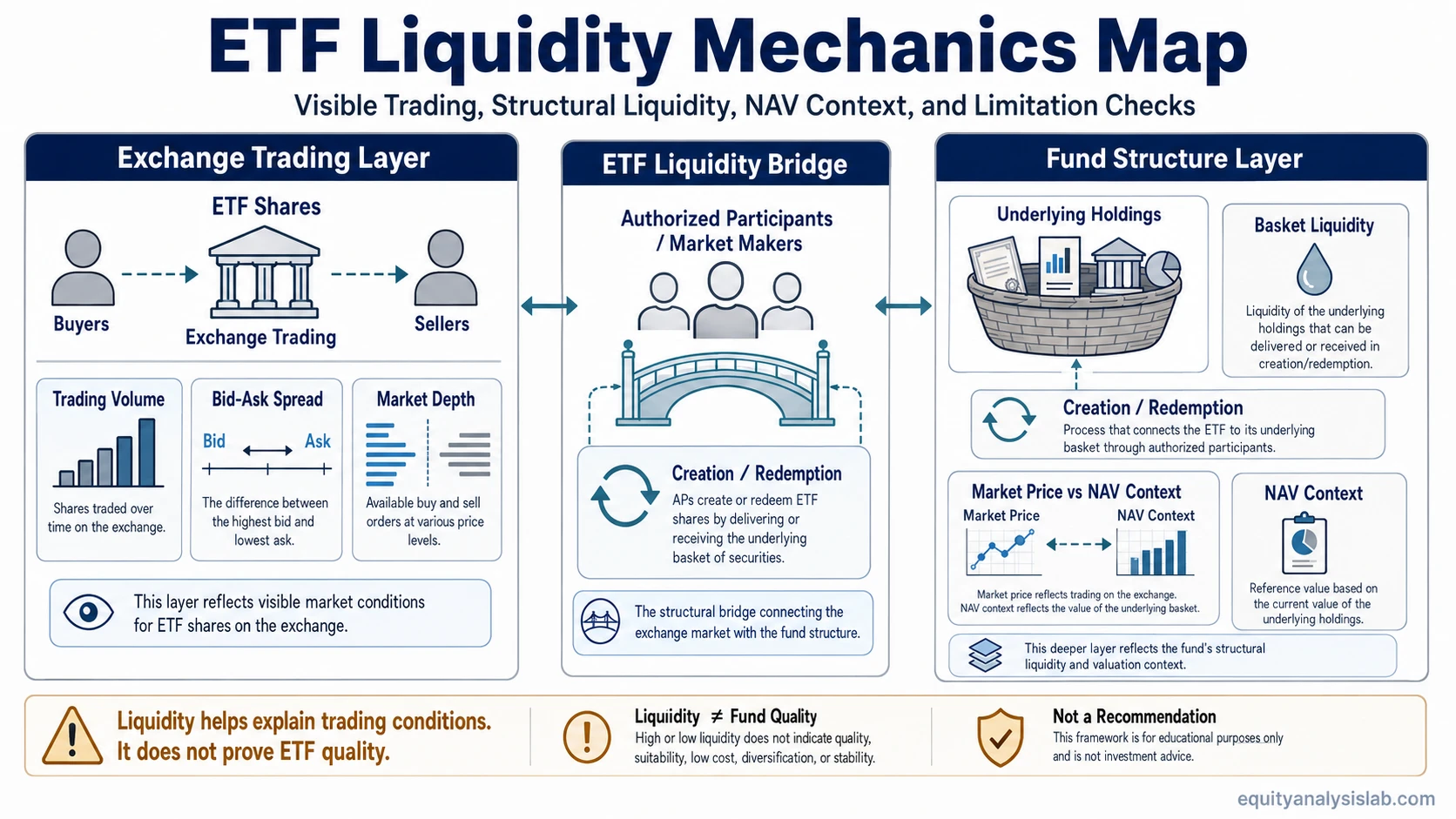

ETF liquidity is the ability to buy or sell ETF shares with limited price impact and reasonable transaction cost. For ETFs, liquidity has two layers: the exchange market where ETF shares trade and the deeper fund mechanism supported by underlying holdings and share creation or redemption.

This makes ETF liquidity different from the liquidity of an ordinary stock. A stock’s trading activity is mainly about the shares already available in the market. An ETF wrapper can also connect exchange trading with the securities, cash instruments, or other exposures held inside the fund.

Liquidity is useful because it affects trading friction and price behavior, but it is not proof that an ETF is high quality, suitable, diversified, low cost, tax efficient, or likely to deliver a specific return.

What Is ETF Liquidity?

ETF liquidity describes how easily ETF shares can trade without a large gap between expected price and actual execution price. It depends on visible exchange conditions, such as quoted spreads and trading volume, and on structural conditions, such as the liquidity of the fund’s holdings and the ability of market participants to create or redeem ETF shares.

The useful distinction is simple: visible liquidity shows what can be observed on the exchange, while structural liquidity explains why ETF trading can sometimes be deeper or more fragile than screen volume alone suggests.

ETF Liquidity Is Not Just Trading Volume

Trading volume is one ETF liquidity signal, but it is not the whole liquidity picture. A heavily traded ETF may still face wider spreads or weaker underlying liquidity during stressed conditions. A lightly traded ETF may have more available liquidity than its on-screen volume suggests if the underlying holdings are liquid and the creation/redemption process is functioning normally.

This does not mean low volume should be ignored. Low volume can still matter because it may coincide with wider quotes, thinner displayed depth, less frequent trading, or less reliable price discovery. The point is narrower: volume is a starting clue, not a complete answer.

| Liquidity layer | What to review | What it can show | What it cannot prove |

|---|---|---|---|

| Visible exchange liquidity | Trading volume, quoted spread, displayed depth, trade frequency | How ETF shares are trading in the secondary market | It cannot prove the ETF is suitable, low cost, or easy to trade in every condition. |

| Quote-cost signal | Bid and ask quotes | The visible gap between buyer-side and seller-side pricing | It cannot explain all fund costs or replace expense-ratio analysis. |

| Structural fund liquidity | Underlying holdings, basket liquidity, creation/redemption conditions | Whether deeper liquidity may exist beyond screen volume | It cannot guarantee smooth trading during stressed or illiquid markets. |

| Price/NAV context | Market price, NAV, premium or discount behavior | Whether ETF shares are trading close to or away from fund value context | It cannot guarantee permanent price/NAV alignment. |

Secondary-Market ETF Liquidity

Secondary-market ETF liquidity refers to ETF shares trading between buyers and sellers on an exchange. This is the most visible liquidity layer because investors can usually observe recent volume, quoted prices, and the gap between the bid and ask.

The bid-ask spread matters because it is a visible transaction-cost signal. A narrower spread usually means buyers and sellers are quoting prices closer together. A wider spread can signal weaker liquidity, higher trading friction, or more uncertainty about the ETF’s fair value.

Market depth also matters. An ETF may show a tight spread for a small number of shares, but larger orders can still move through multiple price levels. That is why volume, spread, and depth should be read together instead of treated as separate proof points.

Primary-Market Liquidity and Creation/Redemption

ETF liquidity can also come from the primary market, where authorized participants can help create or redeem ETF shares through the fund’s basket mechanism. This is one reason ETF liquidity may not be fully captured by the number of shares traded on the exchange during a normal session.

The creation and redemption mechanism can allow ETF share supply to expand when demand rises or contract when shares are redeemed. This can support liquidity when the underlying basket is tradable and the market-making ecosystem is functioning normally.

That mechanism is not unlimited. If the underlying holdings are hard to trade, if market stress widens hedging costs, or if authorized participants become less willing to intermediate, the structural liquidity layer can become less reliable.

Underlying Holdings and Basket Liquidity

The liquidity of an ETF often depends on what the fund owns. An ETF holding highly liquid large-cap stocks may have a different liquidity profile from an ETF holding thinly traded bonds, small-cap securities, bank loans, niche commodities exposure, or less liquid international holdings.

Basket liquidity matters because market makers and authorized participants often look through the ETF wrapper to the cost and feasibility of trading or hedging the underlying exposure. If the basket is easy to trade, the ETF may support more liquidity than recent exchange volume alone suggests. If the basket is hard to trade, screen liquidity can look better than the deeper liquidity reality.

How to Review ETF Liquidity

A practical ETF liquidity review should combine visible market signals with structural fund checks. No single metric is enough because each one answers a different question.

| Check | Question it answers | Useful interpretation |

|---|---|---|

| Trading volume | How often are ETF shares changing hands? | Higher volume can support easier execution, but it does not fully measure underlying liquidity. |

| Bid-ask spread | How wide is the visible quote gap? | A wider spread can signal higher transaction friction or weaker quote confidence. |

| Market depth | How much size is available near the best quotes? | Displayed depth can matter for larger trades, especially when the top quote is thin. |

| Underlying holdings | Can the basket itself be traded efficiently? | Liquid holdings can support structural liquidity beyond ETF share volume. |

| Creation/redemption conditions | Can ETF share supply adjust through the primary market? | The mechanism may support liquidity, but it depends on authorized participants and market conditions. |

| Market price vs NAV | Are ETF shares trading near fund value context? | Premiums or discounts can show pressure between exchange price and NAV context. |

Common Misreadings of ETF Liquidity

Misreading 1: Low ETF volume automatically means poor liquidity. Low volume can be a warning sign, but it does not always capture the liquidity of the underlying basket or the ability to create and redeem shares.

Misreading 2: High ETF volume is enough to prove strong liquidity. High volume can help, but it does not guarantee tight spreads, stable market depth, or smooth trading during stressed conditions.

Misreading 3: ETF liquidity is the same as the spread. The spread is a visible liquidity cost signal. ETF liquidity also includes trading depth, underlying holdings, market-maker activity, creation/redemption conditions, and price/NAV behavior.

Misreading 4: ETF liquidity proves fund quality. Liquidity can affect transaction friction, but it does not prove valuation quality, portfolio fit, tax efficiency, diversification, expense efficiency, or future return potential.

A Simple ETF Liquidity Scenario

Consider two ETFs with similar recent share volume. One holds highly liquid large-cap stocks. The other holds less liquid bonds or niche securities. On the exchange, both may appear similar if only volume is checked. Structurally, they may behave very differently because the underlying baskets are not equally easy to trade.

This is why ETF liquidity review should not stop at screen volume. Volume shows recent share activity; the basket helps explain whether additional liquidity may be available or whether trading could become more fragile under pressure.

ETF Liquidity, NAV, and Market Price

ETF liquidity connects closely with market price and NAV, but those ideas are not the same. The ETF market price is the exchange price where shares trade. NAV is the fund’s per-share value based on the underlying holdings. Liquidity affects how efficiently the market price can trade around that value context.

The ETF arbitrage process can help reduce gaps between market price and NAV, especially when underlying holdings are liquid and the creation/redemption process is functioning. However, premiums and discounts can still appear, especially during market stress, thin trading periods, or when underlying assets are difficult to price or trade.

Limits of ETF Liquidity

ETF liquidity is a trading-condition concept, not a quality label. A liquid ETF can still be expensive, concentrated, poorly suited to an investor’s objective, exposed to volatile holdings, or subject to tracking error. A less liquid ETF can still represent a valid exposure for some investors if the risks and trading costs are understood.

Liquidity should therefore be treated as one review layer inside ETF analysis. It belongs alongside expense ratio, holdings, tracking behavior, distribution policy, tax considerations, portfolio role, and the investor’s time horizon.

Related ETF Concepts

ETF liquidity overlaps with several ETF mechanics, but each one answers a different question. The spread shows the visible quote-cost layer. Creation and redemption explains how ETF share supply can adjust through the primary market. NAV and market price context explains why ETF shares can trade close to, above, or below underlying value. The broader ETF structure explains why a fund can trade on an exchange while still representing an underlying exposure.

Keeping those concepts separate makes liquidity easier to interpret. Visible quotes show one cost signal, primary-market mechanics explain share supply adjustment, and underlying holdings show whether deeper liquidity can support the ETF structure.

FAQ

Does low ETF volume mean poor ETF liquidity?

Low ETF volume can be a warning sign, but it does not automatically prove poor ETF liquidity. The liquidity of the underlying holdings and the creation/redemption mechanism can also affect how much liquidity is available beyond visible exchange volume.

Is ETF liquidity the same as bid-ask spread?

No. The bid-ask spread is one visible cost signal inside ETF liquidity. ETF liquidity also depends on trading volume, market depth, underlying holdings, creation/redemption conditions, and price/NAV behavior.

How do creation and redemption affect ETF liquidity?

Creation and redemption can allow ETF share supply to expand or contract when market demand changes. This can support ETF liquidity, but it still depends on market makers, authorized participants, basket liquidity, and market conditions.