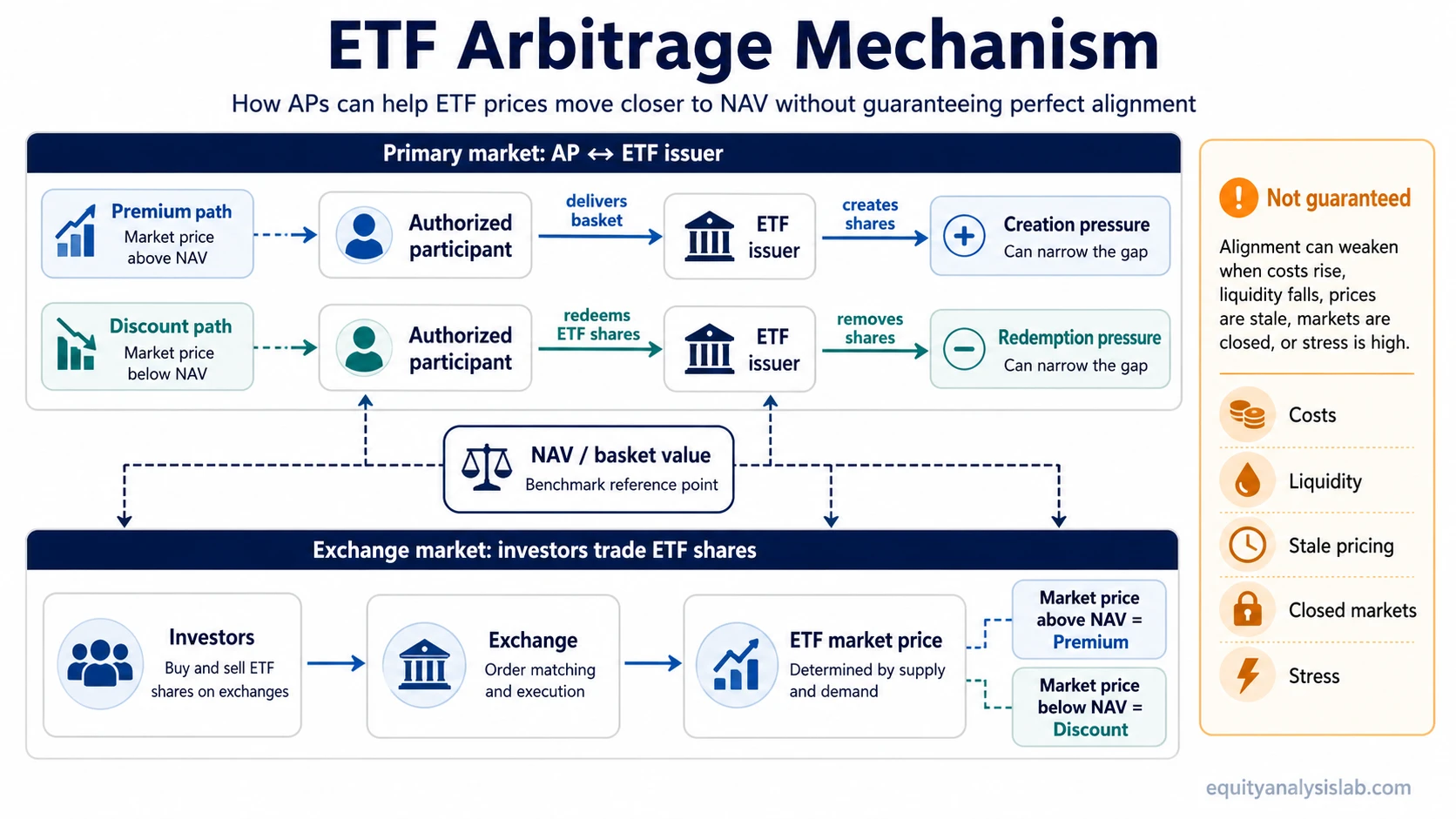

ETF arbitrage is the mechanism that can help an ETF’s market price stay close to the value of its underlying holdings. When an ETF trades above or below NAV, authorized participants may use creation and redemption to adjust ETF share supply, but the process does not guarantee perfect price alignment.

The important boundary is who can use the mechanism directly. Ordinary investors usually trade ETF shares on the exchange, while authorized participants operate in the primary market with the ETF issuer. That makes ETF arbitrage a structural pricing mechanism inside the ETF structure, not a simple retail trading strategy.

Key points about ETF arbitrage

- ETF arbitrage links the ETF’s exchange price with the value of the underlying basket.

- Authorized participants can create or redeem ETF shares with the issuer when incentives are strong enough.

- A premium can create pressure for new ETF shares to be created, while a discount can create pressure for shares to be redeemed.

- The mechanism can weaken when underlying markets are illiquid, closed, stale, or stressed.

What ETF arbitrage means

ETF arbitrage is the process by which institutional participants can help reduce the gap between an ETF’s market price and the value of the assets it represents. The gap usually appears as a premium, when the ETF trades above estimated NAV, or a discount, when it trades below estimated NAV.

The word arbitrage can be misleading because it sounds like a guaranteed trade. In ETF mechanics, the term is better understood as an incentive system. If the ETF price moves too far away from the value of the portfolio, institutions that can access the primary market may have a reason to create or redeem ETF shares.

That incentive depends on real-world frictions. Transaction costs, liquidity, underlying asset pricing, and the availability of arbitrage capital can all affect whether the gap closes quickly, slowly, or only partly.

How authorized participants create the link

Authorized participants, often called APs, are institutions that have agreements allowing them to transact directly with the ETF issuer. They are different from ordinary investors, who normally buy and sell ETF shares in the secondary market through an exchange.

The AP connection links two markets. In the secondary market, ETF shares trade between investors. In the primary market, APs can exchange baskets of underlying securities or cash with the issuer through creation and redemption.

| Part of the mechanism | What happens | Why it matters |

|---|---|---|

| Secondary market | Investors trade ETF shares with each other on an exchange. | This is where the ETF market price is visible. |

| Primary market | Authorized participants transact with the ETF issuer. | This is where ETF share supply can be created or reduced. |

| Underlying basket | The ETF portfolio or creation basket provides the reference value. | This helps define whether the ETF appears rich or cheap relative to NAV. |

| Arbitrage incentive | The AP may act when the price gap is large enough after costs and risks. | The incentive can pressure the ETF price and NAV closer together. |

Premiums, discounts, and NAV pressure

A premium means the ETF trades above the estimated value of its underlying holdings. If that premium is large enough, an authorized participant may be able to deliver the required basket to the issuer, receive new ETF shares, and sell those shares into the market. The added share supply can put downward pressure on the ETF price relative to NAV.

A discount means the ETF trades below the estimated value of its underlying holdings. If that discount is large enough, an authorized participant may buy ETF shares, redeem them with the issuer, and receive the underlying basket or cash value. The reduction in ETF share supply can put upward pressure on the ETF price relative to NAV.

A visible price/NAV gap is not automatically an exploitable opportunity. The gap must be large enough to compensate for trading costs, hedging difficulty, settlement frictions, and uncertainty in the underlying basket value.

Why ordinary investors are not usually doing ETF arbitrage

Most investors participate in ETF pricing through the exchange. They see the ETF’s market price, the quoted spread, and sometimes an estimate of NAV or intraday value. They usually do not deliver baskets to the ETF issuer or redeem ETF shares directly.

This distinction matters because ETF arbitrage is sometimes described as if any price/NAV gap were a simple opportunity. For ordinary investors, the more practical use is interpretation: a premium or discount can point to liquidity, valuation timing, or market stress that deserves closer analysis.

ETF arbitrage explains how the ETF wrapper can stay connected to the underlying portfolio. It does not tell an investor that the premium or discount is automatically wrong.

What investors can observe

Investors cannot usually see every institutional arbitrage decision, but they can observe signs that affect how the mechanism should be interpreted. The most useful clues work best as a group rather than as isolated signals.

| Observable | What it can show | Interpretation limit |

|---|---|---|

| NAV or estimated intraday value | The reference value used to compare the ETF price with the underlying portfolio. | It can be less precise when underlying assets trade infrequently or markets are closed. |

| Premium or discount | Whether the ETF price is above or below estimated NAV. | A gap may reflect real liquidity, timing, or pricing conditions rather than an easy mispricing. |

| Bid-ask spread | The cost of trading ETF shares on the exchange. | A tight premium or discount can still be expensive if the bid-ask spread is wide. |

| Trading volume and depth | How easily ETF shares appear to trade in the secondary market. | Secondary-market volume does not always reveal the liquidity of the underlying basket. |

| Underlying market hours | Whether the assets inside the ETF are actively trading at the same time as the ETF. | International or bond ETFs may show gaps when underlying markets are closed or slow to reprice. |

When ETF arbitrage works best

The mechanism tends to work best when the ETF’s underlying holdings are liquid, transparent, and actively priced. In that setting, APs can estimate the basket value with more confidence and hedge or transact in the underlying assets more efficiently.

Large, liquid equity ETFs often have tighter trading conditions because the underlying securities are easier to value and trade. That does not mean every trade is costless, but it usually gives the arbitrage mechanism more room to operate.

For investors, the practical question is not whether arbitrage exists in theory. The better question is whether the ETF, its underlying basket, and the market environment make that arbitrage mechanism reliable enough for the observed premium or discount to be meaningful.

Why the mechanism can weaken

ETF arbitrage is not a guarantee because every part of the mechanism has costs and constraints. The ETF price may move toward NAV when arbitrage incentives are strong, but it can remain away from NAV when those incentives are too weak or too risky.

| Friction | How it affects arbitrage | Investor takeaway |

|---|---|---|

| Transaction costs | Costs can make a small premium or discount uneconomic for APs. | Not every visible gap is worth closing. |

| Underlying liquidity | Hard-to-trade holdings make basket creation or redemption more expensive. | ETF liquidity should be judged alongside underlying-market liquidity. |

| Stale pricing | NAV may reflect old or estimated prices instead of real-time value. | The ETF price may be incorporating new information faster than reported NAV. |

| Closed markets | The ETF can trade while some underlying assets are not trading. | Premiums or discounts can reflect timing differences rather than abnormal pricing. |

| Market stress | Volatility, funding pressure, or uncertainty can reduce arbitrage appetite. | Gaps can widen when the mechanism is most needed. |

Limitation: ETF arbitrage is a pressure mechanism, not a promise. It can help narrow the distance between market price and NAV, but it cannot remove all trading costs, timing differences, valuation uncertainty, or liquidity stress.

A simple ETF arbitrage scenario

Imagine an ETF whose underlying basket is estimated at $100 per share while the ETF trades at $101. If the premium is large enough after costs, an authorized participant may deliver the basket to the issuer, receive ETF shares, and sell those shares into the market. That added supply can help reduce the premium.

Now imagine the ETF trades at $99 while the basket is estimated at $100. An authorized participant may buy ETF shares, redeem them with the issuer, and receive the basket or cash value. The reduced ETF share supply can help narrow the discount.

The same logic does not mean every premium or discount is a guaranteed profit. The AP still faces trading costs, hedging risk, settlement timing, and uncertainty about the true value of the underlying basket.

How ETF arbitrage connects to ETF liquidity

ETF arbitrage and ETF liquidity are related, but they are not the same thing. Liquidity describes how easily ETF shares and underlying assets can be traded. Arbitrage describes the incentive and process that can connect the ETF’s market price with the value of the portfolio.

A liquid ETF with liquid underlying holdings usually gives arbitrage participants more confidence that they can create or redeem shares efficiently. An ETF with thinly traded underlying assets may still have an arbitrage mechanism, but the cost and uncertainty of using it can be higher.

That is why premiums and discounts should be read with the ETF’s structure, holdings, spreads, and market environment in mind. The arbitrage mechanism matters, but it is only one part of ETF price interpretation.

Common mistakes when reading ETF arbitrage

| Mistake | Why it is misleading | Better interpretation |

|---|---|---|

| Assuming every premium is an opportunity | The premium may be smaller than trading costs or may reflect stale NAV. | Check whether the gap is meaningful after costs and market conditions. |

| Assuming arbitrage always closes gaps immediately | APs are not forced to act, especially in stressed or illiquid markets. | Treat arbitrage as an incentive, not an automatic correction. |

| Ignoring underlying assets | The ETF may look liquid while the underlying basket is harder to trade. | Review both ETF trading conditions and underlying-market liquidity. |

| Confusing retail trading with primary-market access | Ordinary investors usually cannot create or redeem shares directly. | Separate exchange trading from AP/issuer creation-redemption activity. |

FAQ

Is ETF arbitrage a strategy for ordinary investors?

Usually no. ETF arbitrage is mainly a structural mechanism used by authorized participants that can create or redeem ETF shares with the issuer. Ordinary investors usually trade ETF shares on the exchange and use premiums, discounts, spreads, and liquidity as interpretation factors.

Does ETF arbitrage guarantee that an ETF trades at NAV?

No. ETF arbitrage can help move ETF prices toward NAV, but the mechanism depends on costs, liquidity, pricing accuracy, market access, and stress conditions. Gaps can persist when those frictions are meaningful.

Why can an ETF trade at a premium or discount?

An ETF can trade at a premium or discount when exchange demand, underlying basket value, trading hours, liquidity, stale pricing, or market stress cause the ETF share price to differ from estimated NAV. The gap may narrow through arbitrage, but it is not automatically a simple mispricing.