A stock due diligence checklist is a structured review investors use before making an investment decision. It tests whether a company’s business model, financial statements, valuation, management, risks, and thesis evidence support deeper research or reveal reasons to wait, revise, or reject the idea.

Public-stock due diligence is different from a legal diligence request list, an M&A document checklist, an ETF product review, a fund due diligence questionnaire, or a buy/sell signal. Its role is to reduce missing-information risk before capital is committed.

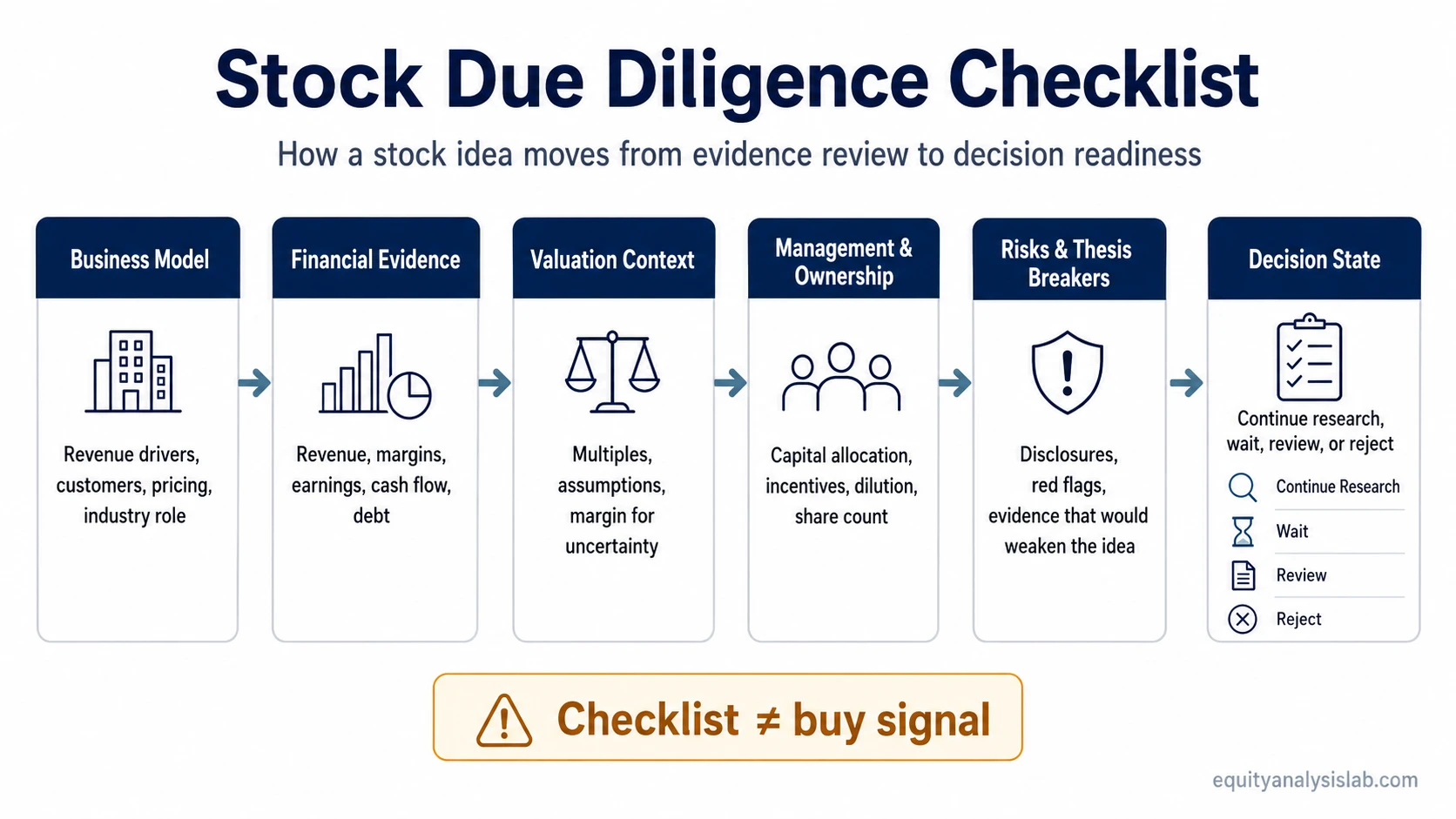

What Is a Stock Due Diligence Checklist?

A stock due diligence checklist is a pre-investment research framework that helps investors review the evidence behind a stock idea before turning it into an investment decision. It organizes the main questions around business quality, financial durability, valuation context, management behavior, ownership structure, risk disclosures, and thesis-breaking evidence.

The checklist does not make the decision by itself. It helps separate a company story from the evidence that supports or weakens that story. A strong narrative may still fail diligence if cash flow is weak, debt pressure is rising, dilution is changing the per-share picture, or valuation leaves little room for error.

The useful output is not a simple pass/fail label. The useful output is a clearer decision state: continue research, wait for better evidence, move the stock back to review, or reject the idea because the thesis is not supported.

The Core Stock Due Diligence Framework

The core framework moves from company reality to decision readiness: business model, financial statements, cash flow quality, balance-sheet risk, valuation context, management and capital allocation, ownership structure, external risks, and thesis impact.

A stock idea usually begins with a reason to care: growth, profitability, quality, valuation, turnaround potential, industry position, or a perceived mismatch between price and fundamentals. Due diligence tests that reason against evidence.

The sequence matters because each layer can change the interpretation of the next one. Revenue growth means less if margins are deteriorating. Earnings mean less if cash flow does not support them. A low valuation multiple means less if the business is structurally weakening. A strong management narrative means less if capital allocation repeatedly dilutes owners or hides balance-sheet risk.

| Framework layer | Main question | Decision role |

|---|---|---|

| Business model | How does the company make money? | Clarifies what the thesis depends on. |

| Financial statements | Do revenue, margins, earnings, cash flow, and debt support the story? | Tests narrative against reported evidence. |

| Valuation context | Is the price reasonable relative to quality, growth, and risk? | Shows whether the thesis has enough margin for uncertainty. |

| Management and ownership | Are capital allocation, dilution, incentives, and share count aligned with the per-share story? | Tests whether business value can translate into shareholder value. |

| Risks and thesis breakers | What evidence would delay, weaken, or invalidate the idea? | Prevents the checklist from becoming confirmation bias. |

Stock Due Diligence Checklist: Questions, Evidence, and Thesis Impact

The checklist should connect every question to evidence and every evidence category to a decision consequence. A vague answer such as “the business looks good” is not enough. The review should show what was checked, what the evidence says, and what would weaken the investment thesis.

| Due diligence question | Evidence to review | Why it matters | What would weaken the thesis |

|---|---|---|---|

| Does the company have a clear business model? | Revenue sources, customer types, pricing model, product mix, segment reporting, and industry role. | The thesis needs a clear explanation of how the company creates and captures value. | The business depends on unclear revenue drivers, temporary demand, weak unit economics, or a story that cannot be tied to reported results. |

| Are revenue and margins durable enough to support the thesis? | Revenue growth, gross margin, operating margin, net margin, segment trends, backlog where relevant, and management commentary. | Growth is more useful when it can translate into durable profitability or operating leverage. | Revenue grows while margins compress, customer acquisition costs rise, pricing power weakens, or growth depends on one unstable source. |

| Does cash flow confirm or contradict reported earnings? | Operating cash flow, free cash flow, working capital, capital expenditure needs, receivables, inventory, and cash conversion. | Earnings quality improves when profits are supported by cash generation instead of only accounting presentation. | Reported earnings rise while cash flow weakens, working capital absorbs cash, capital intensity increases, or receivables grow faster than sales. |

| Is the balance sheet strong enough for the risk being taken? | Cash, debt, maturity schedule, interest expense, interest coverage, liquidity ratios, covenants where disclosed, and refinancing needs. | Balance-sheet pressure can reduce flexibility even when the income statement still looks acceptable. | Debt is high relative to cash flow, interest costs are rising, liquidity is thin, or refinancing risk could pressure the thesis. |

| Is valuation reasonable relative to growth, quality, and risk? | Valuation multiples, peer context, historical range, DCF assumptions if used, margin of safety, growth expectations, and downside scenarios. | Valuation gives context for how much future success may already be reflected in the price. | The stock looks inexpensive only because the business is weakening, or it looks attractive only under optimistic assumptions. |

| Does management allocate capital in a shareholder-aware way? | Buybacks, dividends, reinvestment, acquisitions, debt reduction, compensation incentives, and long-term capital allocation record. | Capital allocation affects whether business value becomes per-share value over time. | Management issues shares aggressively, buys back stock at poor prices, overpays for acquisitions, or prioritizes growth without return discipline. |

| Is dilution, share count, or ownership structure changing the per-share story? | Basic and diluted shares outstanding, stock-based compensation, convertible securities, insider ownership, major holders, and share issuance history. | Per-share value can weaken even when the company grows if ownership is diluted faster than value is created. | Diluted share count keeps rising, stock-based compensation is heavy, convertibles create future dilution, or ownership incentives are unclear. |

| Are industry, customer, or competitive risks visible? | Customer concentration, supplier dependence, competition, regulation, cyclicality, pricing pressure, substitution risk, and industry growth. | A company can look strong in isolation but face external pressure that changes future cash-flow durability. | One customer, supplier, product, region, or industry cycle carries too much of the thesis. |

| Do filings disclose risks that contradict the investment narrative? | Annual reports, quarterly filings, risk factors, footnotes, segment notes, related-party disclosures, legal proceedings, and management discussion. | Filings can reveal risks that are not obvious in headlines, summaries, or investor presentations. | Disclosures point to accounting uncertainty, legal exposure, customer loss, liquidity pressure, or assumptions that conflict with the thesis. |

| What evidence would invalidate or delay the decision? | Contradictory data, missing evidence, stale information, unresolved risks, valuation mismatch, and scenario assumptions. | A checklist is more useful when it defines what would stop the decision, not only what supports it. | The investor cannot name the evidence that would change the view, or weak evidence is ignored because the stock price is moving. |

Business Model and Competitive Position

Business-model diligence starts with a simple question: what has to keep working for the investment thesis to make sense? The answer should include how the company earns revenue, what drives demand, which customers matter, how pricing works, and where the company sits in its industry.

A useful review does not need to turn into a full business-model course. It should identify the main economic engine of the company and the conditions that could weaken it. For example, a company with high revenue growth may still deserve caution if that growth depends on one customer group, promotional pricing, a narrow product cycle, or an industry trend that may not persist.

Decision note: the business model should be clear enough that the investor can explain what would improve it, what would pressure it, and which evidence would show that the original story is no longer reliable.

Financial Statements and Cash Flow Quality

Financial-statement diligence uses the income statement, balance sheet, and cash flow statement as evidence sources. The goal is not to redefine each statement. The goal is to check whether reported performance supports the thesis.

The income statement shows revenue, margin, and profit trends. The balance sheet shows liquidity, debt, working capital, and financial flexibility. The cash flow statement shows whether earnings are converting into cash and how much reinvestment the business requires.

Cash flow deserves special attention because it can confirm or challenge the story told by earnings. If reported profits rise while operating cash flow weakens, receivables build, inventory rises, or capital expenditure needs increase, the thesis may need a more conservative review.

| Financial area | What to check | Why it changes diligence |

|---|---|---|

| Revenue | Growth rate, segment mix, recurring versus one-time drivers, customer concentration. | Shows whether the company’s top-line story is broad, durable, or fragile. |

| Margins | Gross margin, operating margin, net margin, cost pressure, pricing power. | Shows whether growth is becoming more profitable or more expensive to sustain. |

| Cash flow | Operating cash flow, free cash flow, capital expenditures, working capital. | Tests whether earnings are supported by cash generation. |

| Debt and liquidity | Cash balance, debt levels, interest expense, maturities, coverage ratios. | Shows whether financial risk could limit strategic flexibility. |

Valuation Context

Valuation is a context layer, not proof that a stock is attractive. A due diligence checklist should ask whether the valuation is reasonable relative to business quality, growth durability, balance-sheet risk, and the uncertainty around assumptions.

Multiples, peer comparisons, historical ranges, and DCF scenarios can all be useful, but none of them should be treated as a precise answer. A low multiple may reflect real deterioration. A high multiple may require unusually durable growth. A DCF output may change materially when growth, margins, discount rate, terminal value, debt, cash, or share count assumptions change.

Valuation limitation: valuation can show whether expectations are demanding or conservative, but it cannot remove uncertainty or create a buy signal. The checklist should document which assumptions matter most and what would make the valuation case weaker.

Management, Capital Allocation, and Ownership

Management diligence should focus on observable capital allocation behavior rather than personality judgments. The review should ask how management uses cash, whether reinvestment is disciplined, whether acquisitions make economic sense, and whether shareholder returns are supported by the company’s financial position.

Ownership structure matters because the investment thesis is ultimately a per-share thesis. Buybacks can support per-share value when they are funded responsibly and executed at sensible prices. Dilution can weaken the per-share story when new shares, stock-based compensation, or convertible securities grow faster than business value.

The checklist should also review incentives. Compensation metrics, insider ownership, and capital allocation commentary can help investors understand whether management is focused on durable value creation or short-term optics.

Risks, Red Flags, and Thesis Breakers

A stock due diligence checklist is incomplete unless it defines what could break the thesis. Risk review should not be a generic list placed at the end of the process. It should be connected to the specific reason the investor is considering the stock.

| Risk area | What to look for | Thesis-breaker question |

|---|---|---|

| Accounting quality | Large adjustments, weak cash conversion, unusual working-capital movement, aggressive assumptions. | Are reported results less durable than they appear? |

| Debt pressure | High leverage, rising interest expense, maturity concentration, limited liquidity. | Could financial obligations restrict the company before the thesis has time to play out? |

| Dilution | Rising diluted share count, stock-based compensation, convertibles, equity financing needs. | Can business growth still create per-share value? |

| Customer or supplier concentration | Dependence on a narrow customer base, one channel, one supplier, or one geography. | Could one relationship materially change revenue or margins? |

| Competitive erosion | Margin pressure, market-share loss, product substitution, weaker pricing power. | Is the company’s advantage narrowing? |

| Valuation mismatch | High expectations, narrow margin of safety, optimistic assumptions, peer multiple risk. | Does the price already require too much to go right? |

The strongest risk review names the evidence that would change the decision. If the investor cannot describe what would invalidate the thesis, the checklist may be functioning as justification rather than diligence.

When the Checklist Should Send the Stock Back to Review

A stock idea should go back to review when the evidence is incomplete, stale, contradictory, or too dependent on optimistic assumptions. Sending a stock back to review is not the same as rejecting it permanently. It means the idea is not decision-ready yet.

Failure condition: the checklist becomes unsafe when it is used mechanically, when the investor fills it out to justify a decision already made, when weak evidence is ignored because the price is moving, or when missing information is treated as confirmation.

A practical review state can be simple: continue research if the evidence is improving, wait if the evidence is mixed, move the idea back to the watchlist if timing or information is incomplete, and reject the idea if the core thesis is contradicted by financials, valuation, risk, or disclosures.

Limits of a Stock Due Diligence Checklist

A stock due diligence checklist can reduce omission risk, but it does not remove uncertainty, predict returns, or replace investor judgment. A stock can pass many checklist items and still be unattractive if valuation, risk, thesis quality, or portfolio fit does not support the decision.

The checklist cannot turn a weak thesis into a strong one, make valuation precise, or guarantee that strong historical results will continue. Position size, time horizon, and portfolio fit still need the broader investment process.

The checklist is most useful when it creates friction before action. It should slow down decisions driven by narrative, recent price movement, fear of missing out, or pressure to deploy capital before the evidence is strong enough.

Stock Due Diligence in the Investment Research Process

Stock due diligence belongs after a stock idea exists and before an investment decision is made. It is not a scanner, a watchlist manager, a legal diligence list, a target-price model, or a trade timing tool.

Inside the broader investment research process, due diligence acts as the evidence gate. It checks whether the company idea is supported well enough to move toward a thesis, valuation work, portfolio-fit review, or deeper monitoring.

If the evidence is promising but incomplete, the idea can return to a stock watchlist instead of becoming an immediate decision. That keeps the company visible while separating “worth monitoring” from “ready to own.”

Stock Due Diligence Checklist FAQ

Is stock due diligence the same as stock analysis?

No. Stock analysis is the broader process of studying a company and forming an investment view. Stock due diligence is a control step inside that process that checks whether the evidence is complete, consistent, and strong enough before a decision is made.

Does a due diligence checklist tell you whether to buy a stock?

No. A due diligence checklist does not create a buy signal or recommendation. It helps investors identify evidence, risks, gaps, and thesis breakers so the decision can be made with more discipline.

What should investors check before buying a stock?

Investors should review the business model, revenue drivers, margins, earnings quality, cash flow, debt, valuation, management, capital allocation, dilution, ownership structure, industry risks, filings, and the evidence that could weaken or invalidate the thesis.

When should a stock idea go back to the watchlist instead of becoming an investment?

A stock idea should go back to review when the evidence is incomplete, mixed, stale, or too dependent on optimistic assumptions. It can also return to review when valuation, risk, disclosures, or cash-flow quality do not yet support the thesis.