Ireland-domiciled ETF withholding tax is often treated as a simple tax-saving label, but the safer reading is narrower: ETF domicile can change how dividend withholding tax moves through the fund structure, while the investor’s final result still depends on the fund, income type, distribution policy, and local tax rules.

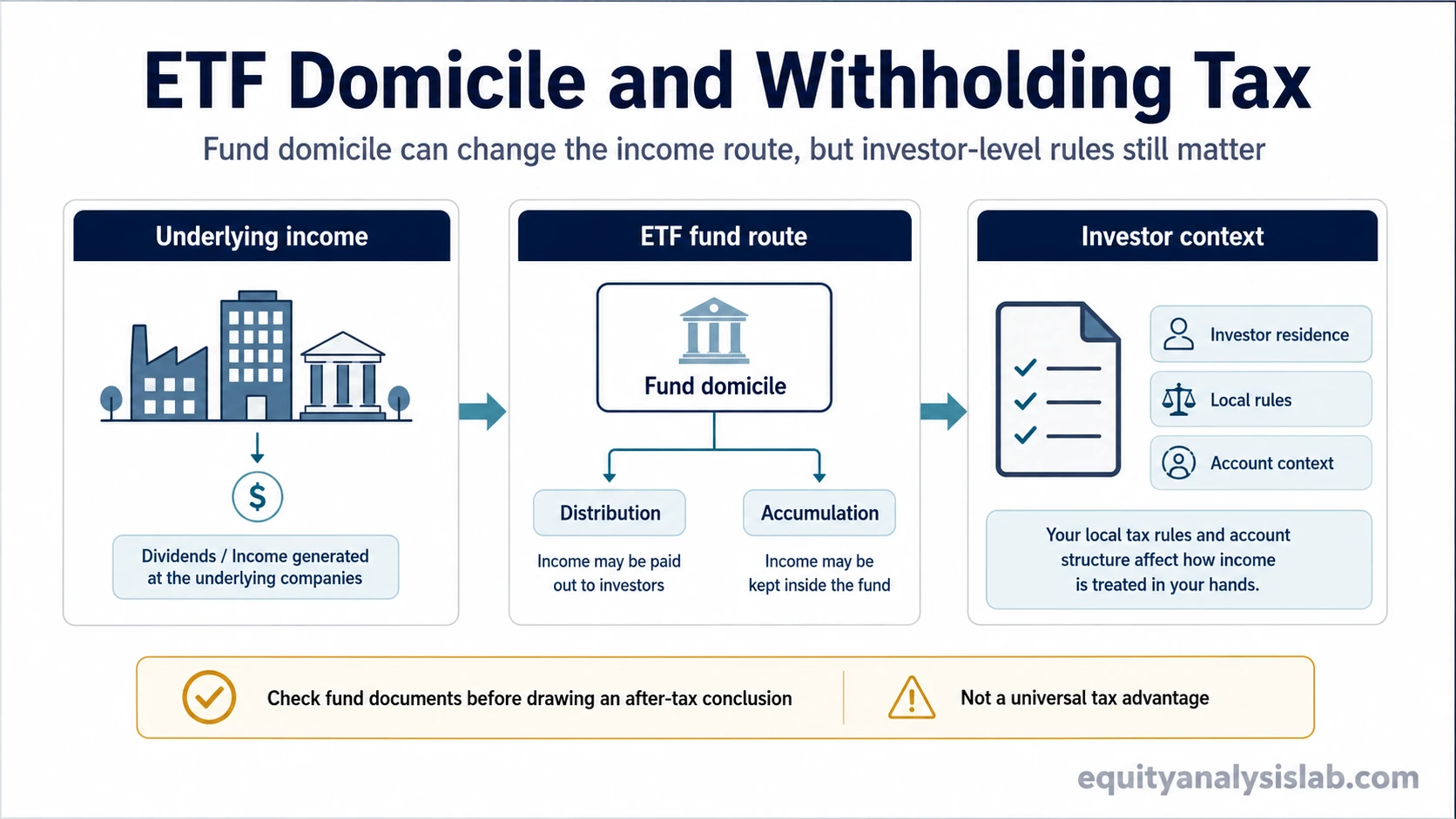

Definition: ETF domicile is the legal and tax residence of the ETF fund. Withholding tax becomes relevant because dividends and other income may face tax before income reaches the fund, before income reaches the investor, or when the investor applies local tax rules.

Domicile is one ETF-selection variable. It can affect the route that income takes through the fund wrapper, but it does not replace the need to compare exposure, expense ratio, tracking difference, bid-ask spread, liquidity, distribution policy, and investor-specific tax context.

Key Points

- ETF domicile is not the same as the exchange where the ETF trades.

- Withholding tax can appear at fund level, investor level, or both, depending on the structure and investor context.

- Ireland-domiciled ETFs are often compared with US-domiciled ETFs because the income route may differ.

- Domicile is not an automatic quality score or universal tax advantage.

- Fund documents and local rules matter before drawing an after-tax conclusion.

What ETF Domicile Changes

ETF domicile identifies where the fund is legally established and regulated. That location can influence the treaties, fund rules, and withholding-tax mechanics that apply before dividends or other income move through the fund structure.

The practical mistake is treating domicile as a shortcut for after-tax outcome. A lower fund-level drag can be offset or changed by other variables, including local dividend rules, share-class policy, fund costs, spreads, and tracking behavior.

Misread: An Ireland-domiciled ETF is automatically better because it may follow a different withholding-tax route.

Safer interpretation: Domicile can change one tax-mechanics layer, but ETF selection still requires comparing exposure, structure, total cost, tracking, liquidity, distribution policy, and the investor’s own tax position.

Domicile, Listing Venue, and Investor Residence

Three labels often get mixed together: where the fund is domiciled, where the ETF is listed, and where the investor is tax resident. They are related, but they answer different questions.

| Check | What it clarifies | Common mistake |

|---|---|---|

| Fund domicile | The legal and tax residence of the ETF fund. | Assuming the trading exchange determines the fund’s tax residence. |

| Listing venue | The exchange where the ETF share class trades. | Assuming a London or European listing automatically explains all tax treatment. |

| Trading currency | The currency used to quote and trade a share class. | Confusing quote currency with fund domicile or underlying income currency. |

| Investor residence | The local tax rules that may apply to the investor. | Assuming the fund’s domicile determines the investor’s final after-tax result. |

| Distribution policy | Whether the share class distributes income or accumulates it inside the fund. | Assuming accumulation or distribution automatically explains the investor’s tax result. |

| Underlying exposure | The countries, sectors, or assets generating income inside the ETF. | Ignoring where the dividends or income originate. |

| Fund documents | The prospectus, KID or KIID, factsheet, tax disclosure, and distribution notes that describe fund-specific mechanics. | Inferring tax treatment only from the ticker, listing venue, or trading currency. |

Cross-border exposure and fund access can also matter when an investor compares an international ETF with a domestic wrapper, but domicile should still be checked separately from listing venue and trading currency.

Where Withholding Tax Can Appear

Withholding tax is easiest to understand as a sequence of possible layers rather than a single number. The same ETF can involve income generated by underlying holdings, income received by the fund, and income distributed or accumulated for the investor.

| Layer | What may happen | What to check |

|---|---|---|

| Underlying company to ETF fund | Dividends or income from underlying holdings may face withholding before reaching the ETF. | Fund domicile, underlying market, treaty treatment, and fund disclosures. |

| ETF fund to investor | The ETF may distribute income, accumulate it, or report it according to the share-class structure. | Distribution policy, share class, fund documents, and ETF dividends mechanics. |

| Investor local tax context | The investor’s country may apply its own rules to distributions, deemed income, reporting, or credits. | Investor residence, local tax rules, account type, and qualified tax review where needed. |

Accumulating and distributing share classes can change how income appears to the investor, but they do not automatically remove tax considerations. The relevant question is how the fund handles income and how local rules treat that income.

US-Domiciled vs Ireland-Domiciled ETF Route

The common comparison is between a US-domiciled ETF and an Ireland-domiciled UCITS ETF that target similar exposure. The comparison is useful, but it should stay focused on mechanics rather than turning domicile into a recommendation.

| Comparison point | US-domiciled ETF route | Ireland-domiciled ETF route |

|---|---|---|

| Fund domicile | The ETF fund is established in the United States. | The ETF fund is established in Ireland, commonly as a UCITS ETF for many non-US investor markets, depending on the fund and listing framework. |

| Income route | Dividends and distributions may be handled under the US fund wrapper and investor-specific rules. | Underlying income may pass through an Irish fund wrapper before distribution or accumulation. |

| Investor interpretation | May be simpler for some investors and less suitable for others, depending on residence, access, account type, and local rules. | May offer different withholding-tax mechanics, but the final result still depends on the investor’s local context. |

| Selection risk | Focusing only on domicile can ignore expense ratio, tracking, spread, fund size, and liquidity. | Focusing only on withholding tax can ignore implementation cost, distribution policy, and fund-specific documents. |

Broader ETF tax efficiency depends on more than domicile. Fund turnover, securities lending, replication method, distribution policy, local rules, and investor account structure can all affect the practical result.

A Practical ETF Comparison Scenario

Two ETFs track similar equity exposure. One is US-domiciled, and the other is an Ireland-domiciled UCITS ETF. The Ireland-domiciled fund may have a different withholding-tax route for dividends from the underlying holdings, but that is only the start of the comparison.

A sharper review starts with the exposure and index, then checks the fund wrapper, distribution policy, expense ratio, tracking difference, bid-ask spread, trading liquidity, fund size, and fund documents. The tax-mechanics question then sits beside the implementation question: whether the structure, costs, and tradability still make sense for the investor’s circumstances.

A cleaner conclusion is narrower: domicile changes a specific income route, so it should be checked in the fund documents and then weighed beside costs, tracking, liquidity, spreads, and distribution policy.

What to Check in Fund Documents

ETF domicile and withholding-tax mechanics should be checked through fund-specific documents rather than inferred from a listing exchange, ticker suffix, or trading currency. A prospectus, KID or KIID, factsheet, tax disclosure, and distribution policy can provide the details needed for a cleaner comparison.

| Document or field | Why it matters |

|---|---|

| Fund domicile | Identifies the fund’s legal and tax residence. |

| Index and holdings | Shows where income-generating assets are located. |

| Distribution policy | Clarifies whether income is distributed, accumulated, or handled through a specific share-class structure. |

| Tax disclosure | May describe withholding-tax treatment, reporting notes, and investor responsibilities. |

| Expense ratio and tracking | Helps compare tax mechanics with total implementation cost and realized fund behavior. |

| Liquidity and spread | Shows whether a potential tax advantage is being offset by trading friction. |

Limits of a Domicile-Based Reading

Limitation: ETF domicile can clarify one part of the withholding-tax path, but it cannot determine the investor’s final after-tax result by itself. Local tax rules, investor residence, account type, fund documents, income type, and share-class policy can change the interpretation.

The explanation is educational and cannot replace review of fund documents or qualified tax guidance. Avoid using domicile as a standalone reason to prefer one ETF over another.

FAQ

Does an Ireland-domiciled ETF always reduce withholding tax?

No. Ireland domicile can change the withholding-tax route for some fund structures, but the final result depends on the fund, underlying income, distribution policy, investor residence, and local tax rules.

Is ETF domicile the same as the exchange where the ETF is listed?

No. Domicile is the fund’s legal and tax residence. Listing venue is the exchange where a share class trades, and trading currency is only the quoted currency for that share class.

Do accumulating ETFs avoid dividend tax?

Not automatically. Accumulating share classes reinvest income inside the fund, but local rules may still treat income, reporting, or gains in different ways depending on the investor’s country.