An international ETF is an exchange-traded fund that gives exposure to securities or markets outside the investor’s domestic market.

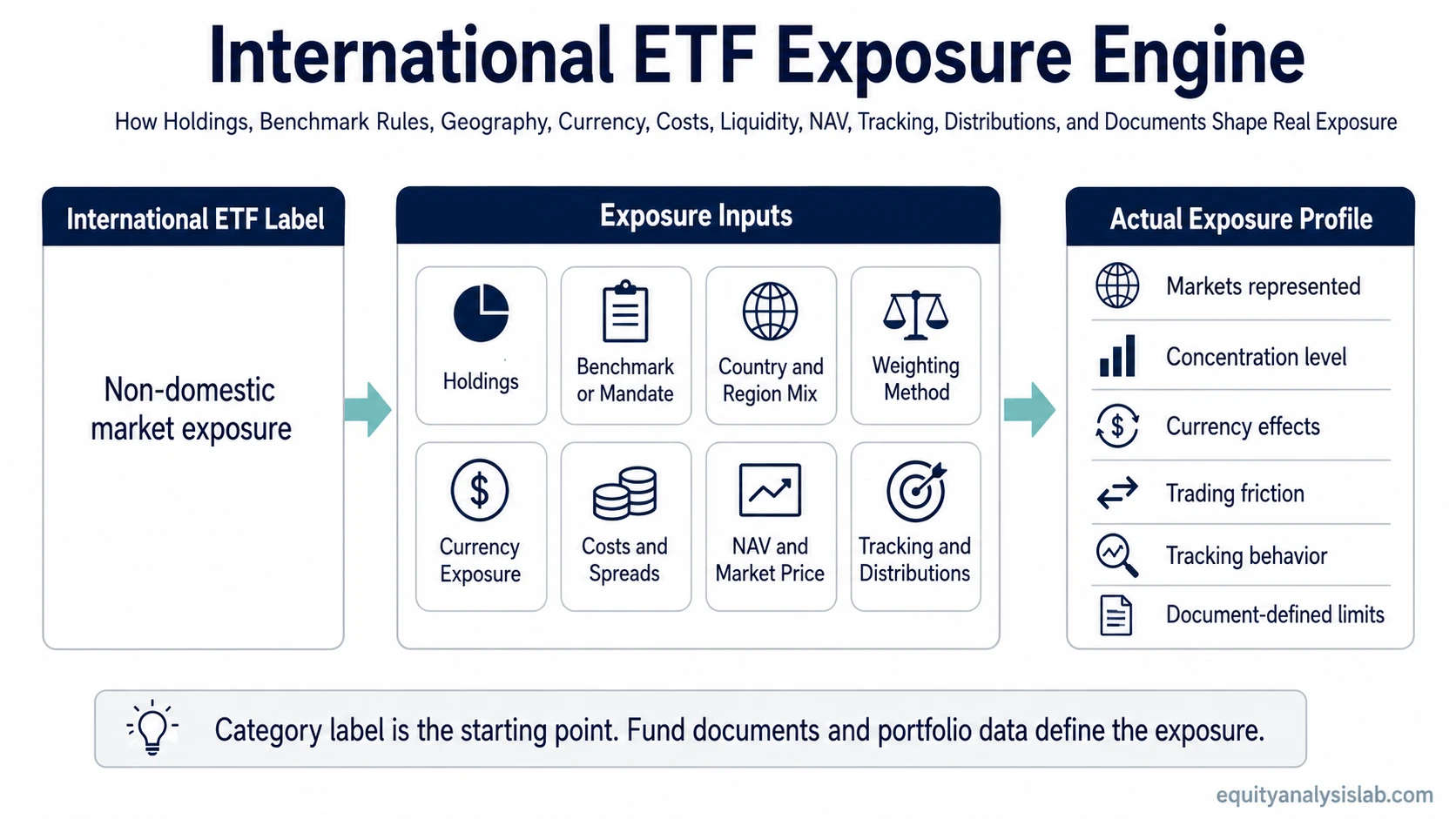

The category label is only a starting point. Holdings, benchmark or mandate, geography, weighting, costs, liquidity, NAV and market price behavior, tracking, distributions, domicile, and fund documents can all change the actual exposure profile.

Key Points

- An international ETF is an ETF type built around non-domestic market exposure.

- The word “international” is only a starting label, not a complete description of what the fund owns.

- Actual exposure depends on holdings, benchmark rules or active mandate, country mix, weighting, currency exposure, costs, liquidity, tracking, and distributions.

- Two international ETFs can behave differently even when their names sound similar.

- Product comparison should start with fund documents, not with the category label alone.

What Is an International ETF?

International ETF definition: an international ETF is an exchange-traded fund that gives investors exposure to securities outside their domestic market. For a U.S.-based investor, that usually means exposure to non-U.S. stocks, bonds, or other eligible securities, depending on the fund mandate.

The category is useful because it separates domestic exposure from foreign market exposure. It does not, by itself, say whether the fund is broad or narrow, developed-market or emerging-market, equity-only or fixed-income, index-based or actively managed.

Some international ETFs track a benchmark. Others use an active process, where the manager selects securities within a stated mandate. That distinction matters because an Actively Managed ETF can have different portfolio construction logic from an index-tracking international fund.

How International ETF Exposure Works

International ETF exposure starts with the fund’s holdings. A name can suggest foreign market access, but the portfolio determines which countries, sectors, currencies, issuers, and asset classes are actually represented.

The benchmark or mandate controls the first layer of exposure. A benchmark may include only developed markets, only emerging markets, a mix of both, a specific region, or a single country. An active mandate may allow more discretion, but the prospectus and portfolio disclosures still define the boundaries.

Weighting changes the final exposure. A market-cap-weighted fund can concentrate heavily in the largest companies, countries, or sectors inside the eligible universe. An equal-weighted or rules-based approach can produce a different country and sector profile, even when the fund is still described as international.

Currency exposure also matters. The fund may hold foreign securities that trade in local currencies, depositary receipts, or other structures. Currency movements can affect the investor’s return experience even when the underlying companies or bonds do not change in value in local terms.

NAV and market price should be separated. The NAV reflects the estimated value of the fund’s underlying portfolio, while the market price is where ETF shares trade. International ETFs can be more sensitive to timing gaps when the underlying foreign markets are closed while the ETF continues to trade locally.

Tracking difference is another layer. Fees, trading costs, sampling methods, taxes, cash drag, currency effects, and market access frictions can cause fund results to differ from the benchmark or stated exposure target.

International ETF Types and Boundaries

International ETF is a broad category, so the useful question is not only whether a fund is international. The more important question is what kind of international exposure the fund is designed to provide.

| Category label | What it usually means | Exposure question to ask |

|---|---|---|

| Broad international ETF | Exposure across multiple non-domestic markets | Which countries, regions, and sectors dominate the portfolio? |

| Global or world ETF | May include both domestic and foreign markets | Does the fund include the investor’s home market or exclude it? |

| Regional ETF | Exposure to a defined region such as Europe, Asia, or Latin America | Is the fund diversified across the region or concentrated in a few markets? |

| Single-country ETF | Exposure focused on one foreign country | How much country, currency, sector, and political risk is concentrated in one market? |

| Developed-market ETF | Foreign exposure limited to markets classified as developed by the benchmark provider | Which markets are included, and which are excluded by the classification rule? |

| Emerging-market ETF | Exposure to countries classified as emerging markets | How much of the portfolio is concentrated in the largest emerging economies or sectors? |

| International bond ETF | Foreign fixed-income exposure rather than foreign equity exposure | What are the currency, duration, credit, sovereign, and issuer risks? |

The main boundary is home-market exposure. An international ETF is usually framed around markets outside the investor’s domestic market, while a global or world ETF may include both domestic and foreign markets. Developed-market and emerging-market labels then describe which foreign markets qualify under the fund’s benchmark or mandate.

International exposure can also appear outside equity funds. A fund can hold foreign bonds, which makes the asset-class boundary important when comparing it with a bond ETF.

International ETFs should also be separated from other exposure categories. A fund built around foreign equities is not the same thing as a fund built around raw materials, futures, or producer-linked exposure. That distinction is why a broad fund-type comparison may need to separate equity exposure from commodity exposure.

Label vs Actual Exposure

The same international ETF label can hide very different exposure profiles. One fund may spread assets across many developed markets with large multinational companies. Another may be heavily concentrated in a few countries, a small group of sectors, or a narrow market classification rule.

| What the label says | What can change the real exposure | Why it matters |

|---|---|---|

| International | Domestic market excluded or included, depending on the fund category | A global fund and an international ex-domestic fund can have different home-market exposure. |

| Diversified | Country, sector, issuer, or currency concentration | A fund can hold many securities while still depending heavily on a few markets or sectors. |

| Developed markets | Benchmark provider classification | Country classification rules affect which markets qualify for inclusion. |

| Emerging markets | Large-country and large-company weights | The largest countries or companies can drive a large share of the fund experience. |

| Low cost | Expense ratio, spread, trading cost, tax drag, and tracking difference | The expense ratio is only one part of the total investor experience. |

| Benchmark exposure | Replication method, sampling, cash position, and local-market access | The fund can differ from the benchmark even when the objective is index tracking. |

What to Check Before Comparing International ETFs

Comparing international ETFs starts with the fund documents and portfolio data. The useful review is not “which international ETF is best,” but whether the fund’s structure and exposure match the investor’s research question.

| Review item | What to inspect | Practical interpretation |

|---|---|---|

| Holdings | Companies, bonds, issuers, sectors, and top positions | Shows what the fund actually owns or references. |

| Benchmark or mandate | Index rulebook, active strategy, eligible markets, and exclusions | Explains why certain countries or securities are included. |

| Country and region weights | Largest countries, regional exposure, developed and emerging split | Reveals whether the fund is broad or concentrated. |

| Currency exposure | Local currency exposure, hedging policy, and reporting currency | Helps separate security performance from currency translation effects. |

| Costs | Expense ratio, trading cost, spread, and other fund-level frictions | Shows how much of the exposure may be reduced by ongoing or trading costs. |

| Liquidity | Trading volume, bid-ask spread, creation/redemption support, and underlying market liquidity | Helps identify whether the ETF share price may trade efficiently. |

| NAV and market price | Premiums, discounts, timing gaps, and market holiday effects | Clarifies whether the traded price may temporarily differ from portfolio value. |

| Tracking | Tracking difference, tracking error, replication method, and sampling approach | Shows whether the ETF has followed its stated benchmark or objective closely. |

| Distributions | Dividend or interest distributions, schedule, and reinvestment assumptions | Separates income treatment from price movement. |

| Domicile and tax documents | Prospectus, tax section, local rules, account type, and withholding considerations | Identifies questions that require document review or tax advice rather than assumptions. |

Example: Same Label, Different Exposure

Consider two hypothetical funds that are both described as international ETFs. Fund A tracks a developed-market benchmark that excludes the investor’s home market and spreads exposure across several large foreign markets. Fund B focuses on a smaller set of emerging markets where a few countries and sectors dominate the portfolio.

The label is similar, but the exposure is not. Fund A may be more affected by developed-market sector weights and major foreign currencies. Fund B may be more affected by country concentration, local market liquidity, currency swings, and emerging-market classification rules.

The stronger review compares holdings, country weights, benchmark rules, costs, liquidity, NAV behavior, tracking, distributions, and documents. The weaker review stops at the category name and assumes both funds solve the same exposure problem.

Risks and Limits of International ETFs

International ETFs can broaden market exposure, but they do not remove risk. They can introduce risks that are less visible in a domestic-only fund, especially when the investor looks only at the category label.

Main limitation: an international ETF is not automatically safer, more diversified, or better suited than a domestic ETF. The exposure must be checked through the fund’s holdings, mandate, benchmark, cost structure, liquidity, tracking behavior, distribution policy, and documents.

Currency risk can affect returns when the investor’s home currency moves against the currencies tied to the underlying holdings. A strong underlying market can still translate into a weaker result after currency effects, while the reverse can also occur.

Country and regional risk can dominate when a fund is concentrated in a small number of markets. A broad-sounding international label may still produce concentrated exposure if the benchmark or weighting method gives large allocations to a few countries.

Emerging-market exposure can add additional uncertainty around liquidity, regulation, governance, capital flows, currency controls, and market access. Those risks vary by fund design and should not be treated as identical across all emerging-market allocations.

Costs and trading frictions can matter more than the headline expense ratio suggests. A fund with a low expense ratio can still have wider spreads, weaker liquidity, larger tracking gaps, or higher practical friction in stressed conditions.

Distribution and tax mechanics may need to be reviewed through fund documents and local rules where relevant. A category label does not determine tax treatment for a specific investor, account type, or jurisdiction.

FAQ

Is an international ETF the same as a global ETF?

No. International often refers to exposure outside the investor’s domestic market, while global or world funds may include both domestic and foreign markets. The exact boundary depends on the fund objective and documents.

Can an international ETF hold bonds?

Yes. Some international ETFs focus on foreign equity exposure, while others can provide foreign fixed-income exposure. The fund mandate and holdings determine the asset class.

Why can two international ETFs perform differently?

Two international ETFs can differ by benchmark, country mix, developed or emerging-market exposure, sector weights, currency exposure, costs, liquidity, tracking behavior, and distributions.

Does an international ETF automatically diversify a portfolio?

No. It can broaden exposure, but diversification depends on the actual holdings, weights, correlations, currencies, countries, sectors, and the investor’s existing portfolio.