Anchoring bias is a behavioral bias in which an early reference point shapes later judgment, even when new evidence should change the decision.

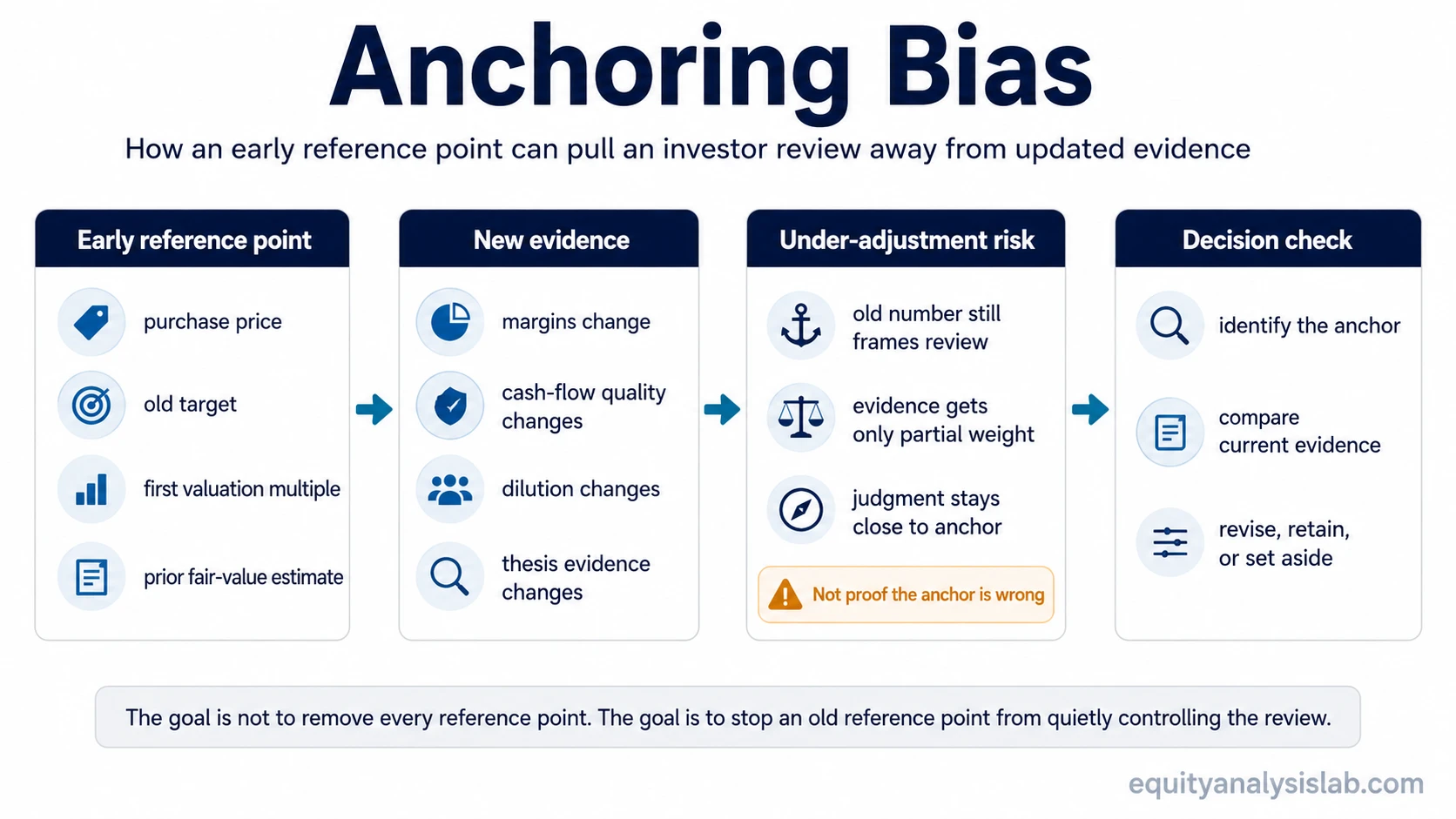

For investors, the anchor may be a purchase price, a prior high or low, an old analyst target, a first valuation multiple, or a previous fair-value estimate. The risk is not that the original reference point was automatically irrational. The risk is under-adjustment: later evidence may receive too little weight because the old anchor still frames the decision.

Definition: Anchoring bias means relying too heavily on an initial reference point when making a later judgment. In investing, it can appear when a prior number continues to influence valuation, position review, or thesis judgment after the underlying evidence has changed.

Key Points

- Anchoring bias starts with a reference point, not necessarily with bad intent, emotion, or carelessness.

- In investing, anchors can include purchase price, prior highs or lows, old targets, first valuation multiples, and earlier fair-value estimates.

- The main decision risk is under-adjusting when new evidence changes the original investment thesis.

- A checklist can help identify where the evidence update is being pulled back toward the anchor without implying that the final investment decision is automatically right or wrong.

What Anchoring Bias Means in Investing

Anchoring bias is a decision-process risk. It occurs when an investor gives too much weight to the first number, first estimate, first narrative, or first impression used to evaluate an investment.

The anchor becomes a reference point. Later information is then judged relative to that reference point instead of being reviewed from a clean evidence base. This can affect how an investor interprets valuation, earnings quality, cash-flow durability, dilution, margin changes, or business-model risk.

An anchor can be useful when it is treated as a starting assumption that must be revised. It becomes risky when it quietly becomes the standard that all new evidence must overcome.

How Anchoring Bias Works

Anchoring bias usually works through under-adjustment. The investor begins with a reference point, receives new information, and adjusts the view only partially. The final judgment may still sit too close to the original anchor.

It can also work through selective evidence review. Once the anchor is in place, evidence that supports the old reference point may feel more relevant, while evidence that challenges it may be discounted, delayed, or explained away. This is where anchoring can overlap with a confirmation-bias pattern, but the two are not identical. Anchoring starts with the reference point; confirmation bias concerns how evidence is selected or defended after a view exists.

In an investment process, the practical problem is not the existence of an initial estimate. Investors need starting assumptions. The problem is failing to update those assumptions when the evidence no longer supports the same interpretation.

Common Anchors Investors Use

Anchors are not limited to formal valuation models. They can come from any number or reference point that becomes psychologically sticky during a decision check.

| Anchor type | How it can affect investor judgment | Evidence to compare against the anchor |

|---|---|---|

| Purchase price | The investor may judge the position around being above or below the entry price rather than around current evidence. | Review the current thesis, valuation context, business evidence, and portfolio role. |

| Prior high or low | A past price level may feel like a natural destination or danger zone even when the business evidence has changed. | Separate historical price memory from current fundamentals and risk conditions. |

| Old analyst target | A prior target may remain persuasive after estimates, margins, rates, or company guidance have shifted. | Check whether the assumptions behind the target still hold. |

| First valuation multiple | The first multiple used in analysis may become the default “normal” multiple even if growth quality or risk changes. | Reassess the multiple against earnings durability, capital intensity, cyclicality, and comparable evidence. |

| Previous fair-value estimate | An earlier estimate may keep shaping the decision even after new cash-flow, dilution, or business-model information appears. | Update the estimate from the underlying drivers rather than adjusting the old number mechanically. |

How to Spot Anchoring Bias in an Investment Review

Anchoring bias is easier to manage when it is treated as an observable thesis-update problem, not as a personality flaw. The following checklist focuses on the decision process rather than on whether the final investment view is right or wrong.

| Checklist point | Question to ask | Why it matters |

|---|---|---|

| Decision trigger | What number, price, estimate, or narrative is pulling the decision back to the original view? | This identifies the anchor before the investor debates the conclusion. |

| Evidence ignored | Which new evidence would matter if the original anchor did not exist? | This separates the present evidence from the old reference point. |

| Checklist failure | Which part of the normal review process is being skipped, softened, or delayed? | This turns a vague bias concern into a process issue that can be reviewed. |

| Position-sizing pressure | Is the anchor influencing how the investor interprets exposure, risk, or the need for review? | This checks whether the reference point is affecting risk interpretation, not only the written analysis. |

| Review mechanism | What evidence would justify revising the original estimate, and what evidence would leave it intact? | This creates a cleaner update rule without assuming the old view must be abandoned. |

Example of Anchoring Bias in an Investment Decision

An investor forms an initial fair-value estimate for a company and uses that estimate as the basis for later review. At the time, the estimate may be reasonable. Later, margins weaken, dilution increases, or cash-flow quality deteriorates. Instead of rebuilding the analysis from the changed evidence, the investor keeps comparing the stock to the original fair-value estimate.

This is an illustrative scenario, not a historical case and not investment advice. The issue is not that the old estimate was automatically wrong. The issue is that the thesis update may be under-adjusting to new evidence because the old estimate still acts as the anchor.

Anchoring Bias vs Related Biases

Anchoring bias can look similar to other behavioral biases, but the decision error starts in a different place.

| Bias | Main reference point | Investor-process distinction |

|---|---|---|

| Availability bias | Information that is easiest to recall | The investor may overweight recent, vivid, or memorable information rather than the first reference point. |

| Confirmation bias | Evidence that supports an existing view | The investor may search for or emphasize evidence that defends the existing thesis. |

| Framing bias | The way information is presented | The same evidence may feel different depending on whether it is framed as a loss, gain, discount, risk, or opportunity. |

Anchoring is specifically about the pull of an early reference point. A purchase price, prior high, old target, or first valuation multiple can keep shaping judgment even after the evidence base changes.

Limitations of Using Anchoring Bias as an Investor Lens

Anchoring bias is a useful lens for reviewing decision quality, but it is not a diagnosis and not proof that an investor is wrong. A prior estimate can still be reasonable if the evidence continues to support it.

Awareness also does not remove anchoring bias by itself. A better safeguard is a repeatable process check: identify the anchor, list the new evidence, check what part of the thesis changed, and decide whether the original estimate should be revised, retained, or set aside.

The goal is not to eliminate every reference point. The goal is to prevent an old reference point from quietly controlling a decision that should be based on updated evidence.

FAQ

Is anchoring bias the same as confirmation bias?

No. Anchoring bias begins with a reference point that shapes later judgment. Confirmation bias concerns the tendency to favor evidence that supports an existing view. The two can appear together, but they describe different parts of the decision process.

Can awareness remove anchoring bias?

Awareness can help, but it does not reliably remove anchoring bias on its own. A structured review process is usually more useful because it forces the investor to compare the old reference point with current evidence.