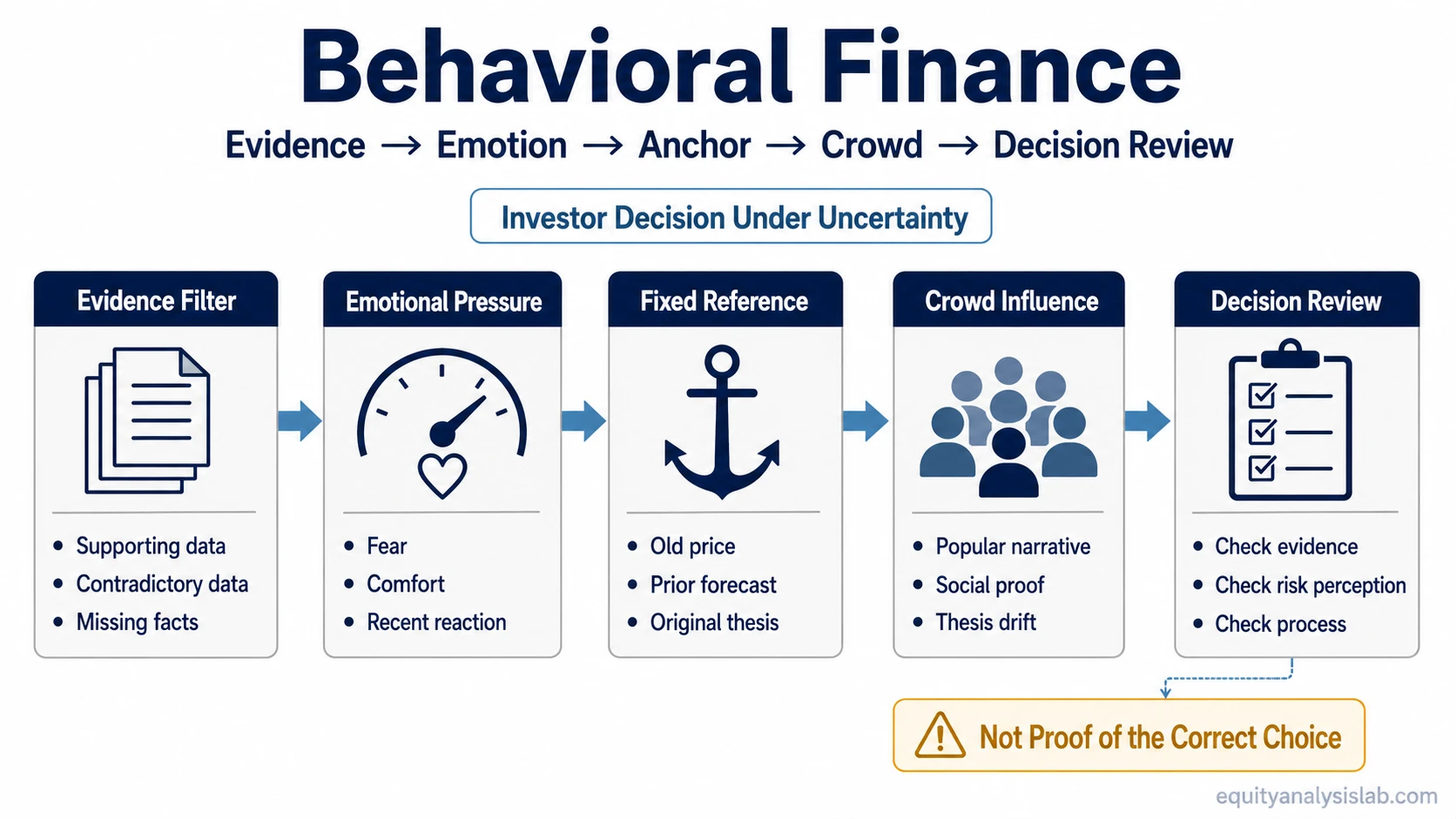

Behavioral finance is the study of how psychology, emotion, and cognitive bias can affect financial decisions, risk perception, evidence review, and portfolio behavior. In investing, it often appears when ignored data, emotional pressure, a fixed reference point, crowd influence, or attachment to an existing thesis changes how an investor reviews evidence.

Its value is not that it proves an investor is irrational or that one investment choice is correct. It is a process-checking lens: a way to inspect whether the investment process is being distorted before the final conclusion is treated as reliable.

Key Points

- Behavioral finance studies how psychology and bias can affect financial decisions.

- It is useful for reviewing evidence, emotional pressure, thesis attachment, and risk perception.

- Bias risk does not prove that an investor is wrong.

- It cannot forecast returns, prove suitability, or select the correct portfolio.

What Is Behavioral Finance?

Behavioral finance is the study of how psychological factors, emotions, and cognitive biases can influence financial decision-making. In investing, it helps explain why an investor may interpret the same evidence differently under pressure, uncertainty, recent market movement, or attachment to a prior view.

The concept sits between finance, psychology, and behavioral economics. Traditional finance often assumes that investors evaluate information rationally. Behavioral finance adds a practical complication: real investors may filter, overweight, ignore, or misread evidence because the decision is being made under uncertainty.

For an investor, the useful question is not “Which bias proves the decision is wrong?” A better question is whether the research process is still testing the thesis against contrary evidence, valuation context, risk constraints, and portfolio-level consequences.

How Behavioral Finance Shows Up in Investor Decisions

Behavioral finance becomes easier to recognize through observable decision behavior. The signal is usually not a feeling by itself, but a process change: evidence gets skipped, a prior reference point becomes too important, or the investor stops asking what would weaken the thesis.

| Decision trigger | Possible bias risk | Evidence being ignored | Review guardrail |

|---|---|---|---|

| A stock falls below the investor’s original purchase price | Attachment to a prior reference point | Updated fundamentals, valuation change, or deteriorating thesis quality | Review the current thesis without using the old price as proof of value |

| Recent news dominates the research process | Overweighting what is vivid or easy to recall | Longer-term earnings quality, balance-sheet risk, and business model durability | Separate recent information from evidence that changes the long-term thesis |

| The investor searches mainly for supportive commentary | Evidence filtering | Contradictory data, margin pressure, dilution, competition, or revised expectations | Write down what would make the thesis weaker before reviewing supporting material |

| Portfolio exposure increases after a strong move | Overconfidence or crowd influence | Position concentration, downside risk, liquidity needs, and valuation sensitivity | Review whether position size still matches the investor’s risk framework |

| A popular market narrative becomes the main reason for holding | Herd behavior or thesis drift | Company-specific evidence, cash flow, competitive position, and risk limits | Restate the thesis using evidence that would still matter without the crowd narrative |

This type of review does not decide whether the investment should be owned. It helps separate evidence-based reasoning from decision pressure that can distort the interpretation of that evidence.

Common Behavioral Finance Biases

Behavioral finance includes many biases, but an investor does not need a long list to use the concept well. The practical use is to identify which kind of decision pressure may be affecting the research process.

| Bias | How it can affect investor decisions | Process question to ask |

|---|---|---|

| Anchoring | The investor gives too much weight to an old price, valuation, forecast, or thesis reference point. | Would the same conclusion make sense if the original reference point were removed? |

| Availability | Recent or vivid information receives more attention than slower, less visible evidence. | Is the decision being driven by what is easiest to remember rather than what is most relevant? |

| Confirmation | Supportive evidence is collected while contradictory evidence receives less attention. | What evidence would challenge the current thesis? |

| Loss aversion | The investor may treat avoiding a realized loss as more important than reviewing the current opportunity cost. | Is the decision based on current evidence or on discomfort with recognizing a loss? |

| Overconfidence | The investor may underestimate uncertainty after a correct call, a strong return, or a persuasive thesis. | What assumption has the widest error range? |

| Herd behavior | The investor may become more comfortable with a decision because many others appear to agree. | What evidence would still matter if the crowd view disappeared? |

| Recency | The investor may treat the latest movement or result as more representative than it is. | Does the recent evidence change the thesis, or only the emotional weight of the decision? |

These biases can overlap. A thesis may be anchored to an old valuation while confirmation-driven research filters out weaker evidence. The review should focus on the decision process, not on labeling the investor.

Behavioral Finance as a Decision-Review Layer

Behavioral finance is most useful when it is placed between research and action. It gives the investor a way to ask whether the conclusion still follows from the evidence or whether the process has been pulled by emotion, habit, reference points, or social pressure.

Evidence review: Has the investor considered both supporting and contradictory information?

Thesis review: Has the original investment case changed, or is the investor defending an old view?

Risk perception: Has recent price movement changed the perceived risk more than the actual evidence changed?

Portfolio behavior: Does the decision still fit concentration, liquidity, time horizon, and risk constraints?

This keeps behavioral finance within its proper role. It can improve the quality of questions asked before a decision, but it does not replace valuation work, business analysis, risk capacity review, or portfolio construction rules.

Behavioral Finance Decision-Checklist Scenario

An investor has followed a company for several years and built a thesis around its margin expansion. After a disappointing earnings report, the investor reads several supportive opinions and focuses on management’s optimistic comments. At the same time, the investor spends little time reviewing weaker cash conversion, rising debt, and whether the original margin thesis still has evidence behind it.

A behavioral finance review would not automatically say the stock is good or bad. It would slow the decision down and ask whether the investor is filtering evidence, anchoring to the old thesis, or giving too much weight to comforting information. The useful output is a cleaner decision process, not a guaranteed investment answer.

What Behavioral Finance Cannot Prove

Behavioral finance can identify process risk, but it cannot prove the correct investment choice. A biased decision can still have a favorable outcome, and a disciplined decision can still produce an unfavorable result because markets, companies, valuation, and timing remain uncertain.

It also cannot diagnose an investor, forecast returns, prove suitability, or determine the right allocation. Those questions require separate evidence, financial constraints, risk capacity, time horizon, liquidity needs, and portfolio-level analysis.

The limitation matters because behavioral finance can be misused as a label. Calling a decision “biased” is not enough, and it should not be treated as a psychological diagnosis. The stronger use is to identify the specific process weakness and decide what evidence should be reviewed before the conclusion is trusted.

Related Behavioral Biases

Behavioral finance is the broader field, while individual bias pages separate specific decision patterns. Anchoring bias focuses on the risk of relying too heavily on a fixed reference point such as an old price, forecast, or valuation.

Availability bias explains how vivid or recent information can dominate the evidence review even when quieter information is more relevant to the investment question.

Research discipline also depends on how the investor handles confirming evidence, especially when a thesis already feels familiar or emotionally comfortable.

FAQ

What is behavioral finance?

Behavioral finance is the study of how psychology, emotion, and cognitive bias can affect financial decision-making, investor behavior, risk perception, and evidence review.

Is behavioral finance the same as behavioral economics?

Behavioral finance applies behavioral and psychological ideas to financial decisions. Behavioral economics is broader and studies how human behavior affects economic choices more generally.

Does behavioral finance prove investors are irrational?

No. Behavioral finance helps identify decision-process risks, but it does not prove that an investor is irrational, that a specific investment is wrong, or that a particular portfolio is suitable.