Loss aversion is the tendency for losses to carry more psychological weight than equivalent gains, which can distort how investors review evidence after a position declines.

Definition: Loss aversion describes a behavioral bias where avoiding or reducing the feeling of loss can become more influential than weighing new business, valuation, risk, and portfolio evidence neutrally.

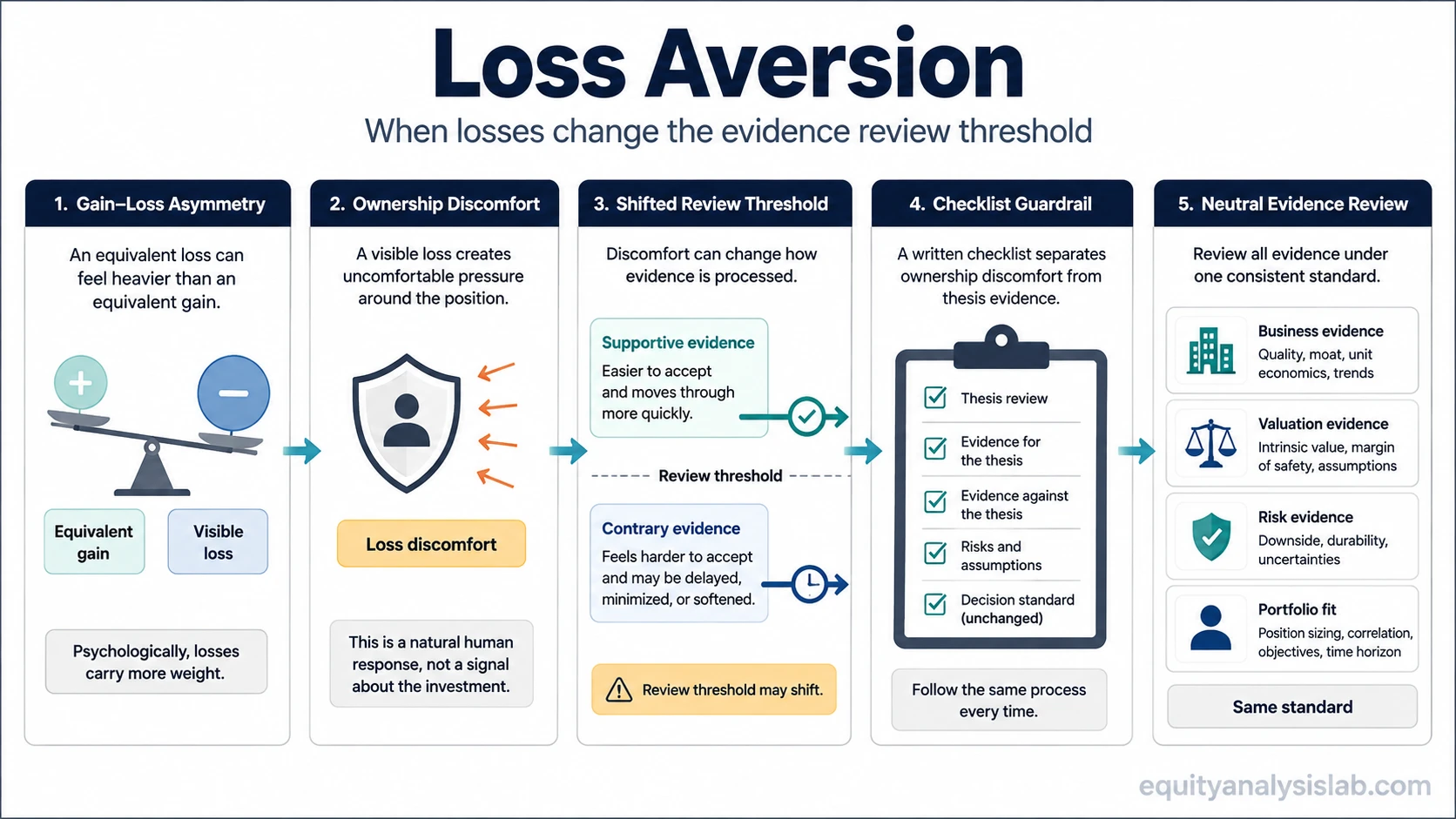

For investors, the main risk is not that every declined position is wrong. The risk is that ownership can change the burden of proof. A weak supportive data point may feel easier to accept, while contrary evidence may be delayed, softened, or treated as temporary without the same level of review.

Loss aversion sits within behavioral finance concepts because it connects emotion, uncertainty, and decision process. The practical value is in noticing when evidence is being accepted, rejected, or delayed differently after ownership begins.

Key Points

- Loss aversion means losses can feel more important than equivalent gains during investor decision-making.

- The bias can appear when an investor requires less evidence to keep a losing position than would be required to start the same position fresh.

- A declined holding is not automatically a bad investment; loss aversion is a prompt to check whether the review threshold has shifted.

- The strongest guardrail is to separate ownership discomfort from the current thesis evidence.

What Loss Aversion Means

Loss aversion is usually explained as a loss-versus-gain asymmetry: the discomfort of losing can outweigh the satisfaction of gaining a similar amount. In investor behavior, that asymmetry can make realized or unrealized losses feel larger than fresh evidence about business quality, valuation, financial risk, or portfolio fit.

Loss aversion is commonly discussed in behavioral economics and prospect theory, but an investing review does not need a full academic model to use the idea safely. The narrower question is whether the presence of a loss has changed how evidence is being accepted, rejected, or delayed.

A neutral review asks whether the current thesis still fits the evidence. A loss-affected review may quietly ask a different question: how can the discomfort of realizing the loss be avoided?

How Loss Aversion Shows Up in Investor Decisions

Loss aversion often appears through evidence weighting. An investor may become more patient with weak thesis support, more forgiving of deteriorating business evidence, or more focused on the possibility of recovery than on the quality of the current case.

One common pattern is a higher threshold for admitting thesis damage. A new risk that would have mattered before ownership may be reframed as noise after the position is already down. Another pattern is a lower threshold for keeping the position: small improvements receive more attention than the broader evidence set can justify.

The opposite side can also appear. Gains may be protected too quickly because securing relief feels safer than continuing to review the thesis. That behavior is still connected to loss aversion when the dominant pressure is avoiding a future loss rather than weighing the evidence on its own terms.

Observable Signs That the Review Threshold Has Shifted

Loss aversion becomes more useful when it is translated into observable review behavior. The bias cannot be proven from discomfort alone; it becomes more plausible when the investor applies a different standard for accepting or rejecting new information after the loss is visible.

| Observable investor behavior | What it may indicate | Review guardrail |

|---|---|---|

| The position review becomes less strict after a decline. | Loss avoidance may be influencing how evidence is weighted. | Re-read the original thesis and list the evidence that would change it. |

| Weak supportive evidence receives more attention than stronger contrary evidence. | The review standard may have shifted toward defending the holding. | Compare the standard with the evidence required for a fresh investment review. |

| Contrary evidence is repeatedly softened, delayed, or treated as temporary. | Ownership discomfort may be shaping interpretation. | Separate business evidence from the discomfort created by the visible loss. |

| The investor keeps changing the reason for owning the position. | The thesis may be adapting to protect the position rather than to reflect new evidence. | Write the current thesis in one sentence and compare it with the original reason for ownership. |

| Recovery potential receives attention before downside evidence is reviewed. | The desire to get back to even may be crowding out neutral analysis. | Review business quality, valuation, balance-sheet risk, and portfolio fit before recovery scenarios. |

Simple Loss Aversion Example in Investor Review

An investor owns a company whose share price has declined after weaker operating results. Before ownership, the investor required durable revenue growth, stable margins, and credible cash-flow evidence. After the decline, the same investor gives more weight to a single positive management comment while treating margin pressure, weaker cash conversion, and slower customer growth as temporary.

The concern is not the decline by itself. The concern is that the thesis-review discipline has become easier on supportive evidence and harder on contrary evidence. A more neutral review asks whether the same business evidence would be strong enough if the position were not already owned. If the answer is no, loss aversion may be influencing the review process.

A cleaner review does not require an automatic action. It requires a consistent standard. The current thesis, the evidence that would change it, and the reasons for continued ownership need to be clear enough to review without relying on the desire to avoid realizing a loss.

Loss Aversion vs Nearby Behavioral Biases

Loss aversion is different from anchoring bias. Loss aversion is about the psychological weight of losses compared with gains. Anchoring bias is about relying too heavily on a reference point, such as an original purchase price, old valuation estimate, or previous high.

Loss aversion also differs from availability bias. Availability bias gives extra weight to information that is easy to recall. Loss aversion gives extra weight to the discomfort of loss, even when the most available information is not the most relevant evidence.

| Concept | Main pressure | Investor review risk |

|---|---|---|

| Loss aversion | Losses feel more powerful than equivalent gains. | The investor may adjust the burden of proof to avoid realizing or accepting a loss. |

| Anchoring bias | A reference point becomes too influential. | The investor may treat an old price or valuation as more meaningful than current evidence. |

| Availability bias | Easily recalled information receives too much weight. | The investor may overweight recent headlines, memorable examples, or vivid narratives. |

| Framing bias | Presentation changes interpretation. | The investor may react differently to the same facts depending on wording, sequence, or comparison base. |

| Sunk cost effect | Past commitment influences current judgment. | The investor may defend a decision because time, attention, or capital has already been committed. |

Investor Checklist Guardrail

A checklist guardrail is useful because loss aversion often works through subtle review changes rather than obvious panic. Written questions make the standard easier to compare before and after ownership.

- What evidence would change the thesis if the position were not already owned?

- Would the same risk be accepted in a fresh investment review?

- Is the current review defending the thesis or avoiding realization?

- Has the review threshold changed since ownership began?

- Which facts are business evidence, and which reactions come from ownership discomfort?

- What would a neutral reviewer need to see before accepting the current thesis?

The checklist does not remove uncertainty. It makes the review standard visible. A visible standard can be compared, challenged, and updated when evidence changes.

Limitations of Loss Aversion

Loss aversion does not prove that a declined holding is wrong. A position can fall for reasons that do not damage the long-term thesis, and an investor may have rational reasons to continue reviewing the evidence patiently.

Loss aversion also does not explain every decision made after a loss. Taxes, portfolio constraints, liquidity needs, risk limits, valuation changes, and new business evidence can all matter. The bias is most useful as a review prompt when supportive and contrary evidence are no longer being judged by the same standard.

The safest use is diagnostic rather than prescriptive. Loss aversion flags the possibility that emotional loss avoidance is influencing interpretation. The next step is better evidence review, not automatic action.

FAQ

What is a simple example of loss aversion in investing?

A simple example is an investor giving weak supportive evidence more weight after a position declines, while requiring much stronger evidence before admitting that the thesis has weakened.

Is loss aversion the same as risk aversion?

No. Risk aversion is a general preference for lower uncertainty or lower risk. Loss aversion is specifically about losses carrying more psychological weight than equivalent gains.

Does loss aversion mean a losing investment is wrong?

No. Loss aversion does not prove the investment is wrong. It signals a need to check whether the evidence standard has changed because the loss is emotionally uncomfortable.