Confirmation bias is the tendency to favor information that supports an existing belief while giving less weight to information that challenges it.

In investor review, confirmation bias can tilt the evidence process before a thesis, valuation view, or risk assessment has been tested against contradictory evidence.

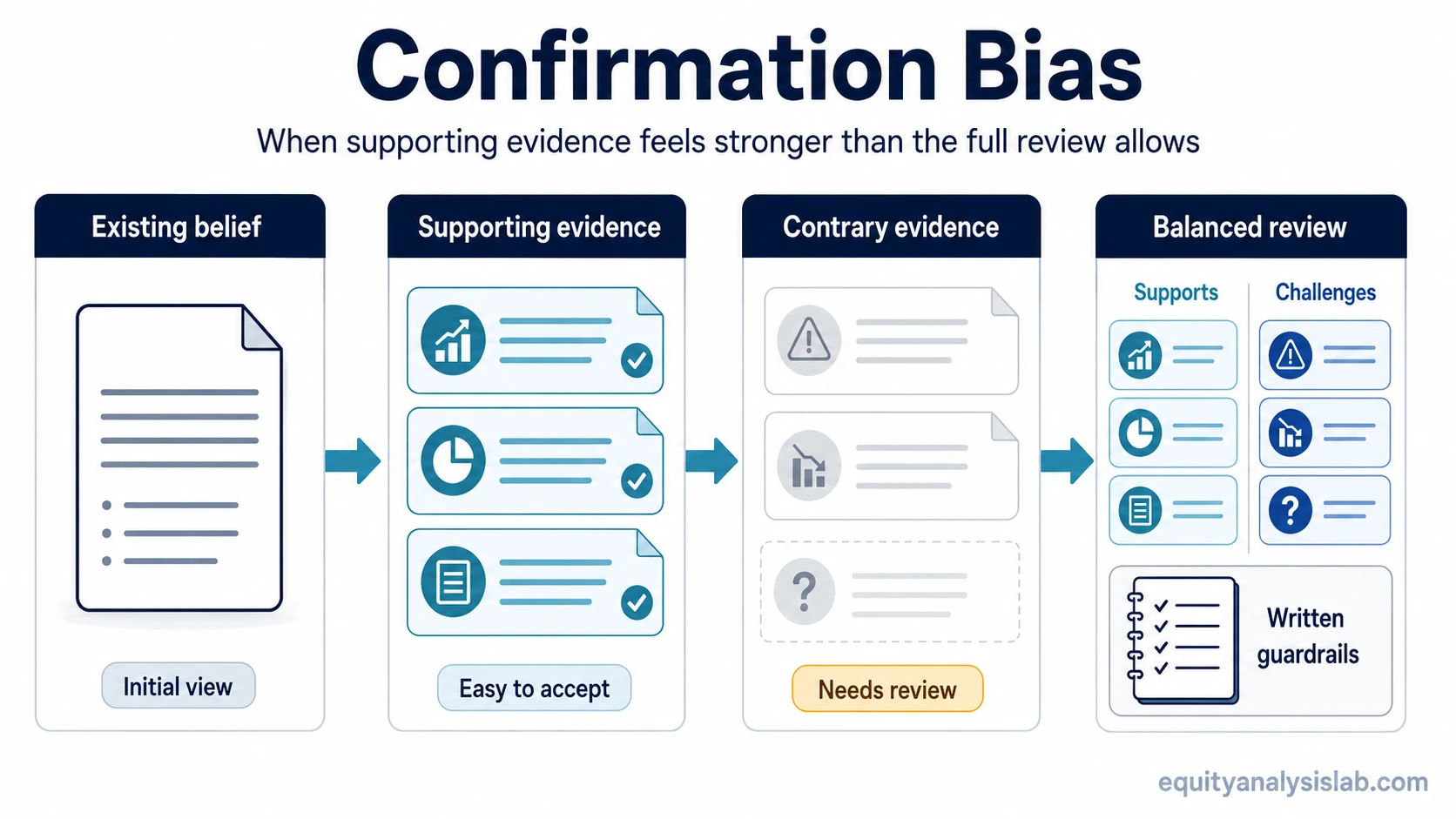

Confirmation bias definition: confirmation bias means that evidence supporting an existing view feels easier to accept, while disconfirming evidence is ignored, minimized, or interpreted defensively.

For investors, the problem is not simply “having conviction.” The problem is that the review process can become uneven: supporting facts receive detailed attention, while contrary facts receive less serious testing.

What confirmation bias means

- Confirmation bias affects how evidence is searched for, interpreted, and remembered.

- It can make an investment thesis feel stronger than the full evidence base supports.

- It often appears when a conclusion forms before the risk review is complete.

- It does not automatically mean the thesis is false; it means the review may be unbalanced.

How confirmation bias changes investor evidence review

Confirmation bias can enter the decision process before the final conclusion is written. An investor may begin with a reasonable idea, then search mainly for evidence that makes the idea easier to defend. The same bias can also shape interpretation: mixed data is treated as supportive, weak evidence is upgraded, and adverse evidence is explained away too quickly.

The risk is strongest when the investor has already committed emotionally to the thesis. At that point, the evidence review may shift from “What is true?” to “What protects the conclusion I already prefer?”

| Trigger | Biased evidence behavior | Investor-review risk | Guardrail |

|---|---|---|---|

| A thesis feels attractive early | Searching mostly for facts that support the thesis | Adverse evidence may be missed or reviewed too late | Write the strongest opposing argument before strengthening the thesis |

| New information is mixed | Interpreting uncertain evidence as more supportive than it is | Weak evidence can become over-weighted | Separate fact, interpretation, and assumption in written notes |

| Past examples are easy to remember | Recalling confirming examples more easily than failed or contrary examples | Memory can make the thesis feel more tested than it is | Use written review questions instead of relying on recalled examples |

| Negative evidence appears after conviction forms | Minimizing or rationalizing the new information | The thesis becomes harder to update | Define what evidence would change the conclusion before reviewing updates |

Signs of confirmation bias in investment analysis

Confirmation bias is not a formal diagnosis. It is a review-process warning. These signs suggest that the evidence base may be leaning toward thesis defense rather than balanced evaluation.

- The investor searches for confirming data before checking disconfirming evidence.

- Negative evidence is described as temporary without a clear reason.

- A checklist is bypassed after the thesis feels emotionally settled.

- The strongest opposing argument is not written down.

- Position size, conviction, or confidence rises faster than the evidence base.

- New facts are judged by whether they protect the thesis rather than whether they change the thesis.

Types of confirmation bias

Confirmation bias can affect several parts of investor review at the same time. The most useful distinction is between search, interpretation, and recall.

| Type | What it means | Investor example |

|---|---|---|

| Biased search | Looking mainly for evidence that supports an existing belief | Reading bullish arguments before looking for balance-sheet, valuation, or competitive-risk concerns |

| Biased interpretation | Reading ambiguous evidence as more supportive than it really is | Treating a mixed earnings report as clearly positive because one favored metric improved |

| Biased recall | Remembering confirming examples more easily than contrary examples | Recalling past thesis successes while forgetting cases where similar evidence was incomplete |

| Defensive discounting | Reducing the importance of evidence that challenges the thesis | Calling every adverse update “temporary” without defining what would make the concern material |

Example of confirmation bias in an investor review

An investor begins with a thesis that a company can improve margins over the next few years. The initial observation is reasonable: recent commentary suggests cost discipline, and one segment has started to show better operating leverage.

The thesis becomes easier to defend because several supporting details line up. Management language sounds more disciplined, the investor remembers similar cases where margins improved, and a valuation model becomes more attractive when higher future margins are assumed.

The review is incomplete if contradictory evidence is handled too casually. Revenue growth may be slowing, customer concentration may be rising, or cash conversion may not be improving with reported earnings. Confirmation bias appears when those concerns are treated as minor because they make the preferred thesis harder to defend.

A stronger review would compare both sides before the thesis hardens: what supports margin improvement, what would weaken it, which assumptions carry the valuation, and what evidence would force a revision. A weaker review keeps adding supportive facts while never writing down the best disconfirming argument.

How to check confirmation bias before a thesis hardens

Confirmation bias cannot be removed completely, but the review process can be made more balanced. The stronger discipline is to make opposing evidence visible before conviction becomes difficult to update.

| Review step | Question to ask | Why it helps |

|---|---|---|

| Opposing thesis | What is the strongest case against this investment thesis? | Forces disconfirming evidence into the review before the conclusion settles |

| Evidence separation | Which points are facts, which are interpretations, and which are assumptions? | Prevents mixed evidence from being treated as stronger than it is |

| Valuation pressure test | Which assumption has the largest effect on the valuation argument? | Shows where confidence may depend on one fragile input |

| Risk review | What new evidence would change the conclusion? | Makes thesis revision possible before contradictory evidence appears |

| Written checklist | Has the same review process been applied to both supportive and adverse evidence? | Reduces the chance that conviction replaces analysis |

What confirmation bias does not prove

Confirmation bias does not prove that an investment thesis is wrong. It means the evidence-review process may be tilted toward support rather than balanced evaluation.

A thesis can still be correct, but the review is weaker if contrary evidence was not seriously tested. The practical issue is the quality of the decision process, not whether the final view happens to be favorable or unfavorable.

Related behavioral biases

Confirmation bias is easiest to separate from nearby biases by asking what part of the review process is being pulled out of balance.

- Anchoring bias is about an initial reference point staying sticky after new evidence appears.

- Availability bias is about memorable or easy-to-recall information feeling stronger than a broader evidence base.

- How framing bias changes interpretation depends on the way information is presented, not only on whether it supports an existing belief.

FAQ

Is confirmation bias the same as being wrong?

No. Confirmation bias describes a tilted evidence-review process. The conclusion may still be correct, but confidence is weaker if contrary evidence was not tested seriously.

How can confirmation bias affect investors?

It can affect the search for evidence, the interpretation of mixed information, and the recall of past examples. In investor review, that can make a thesis feel more supported than the full evidence base justifies.

What is the simplest way to check for confirmation bias before making a decision?

Write down the strongest opposing argument before finalizing the thesis. Then separate facts, interpretations, and assumptions so the conclusion is not protected by selective evidence.