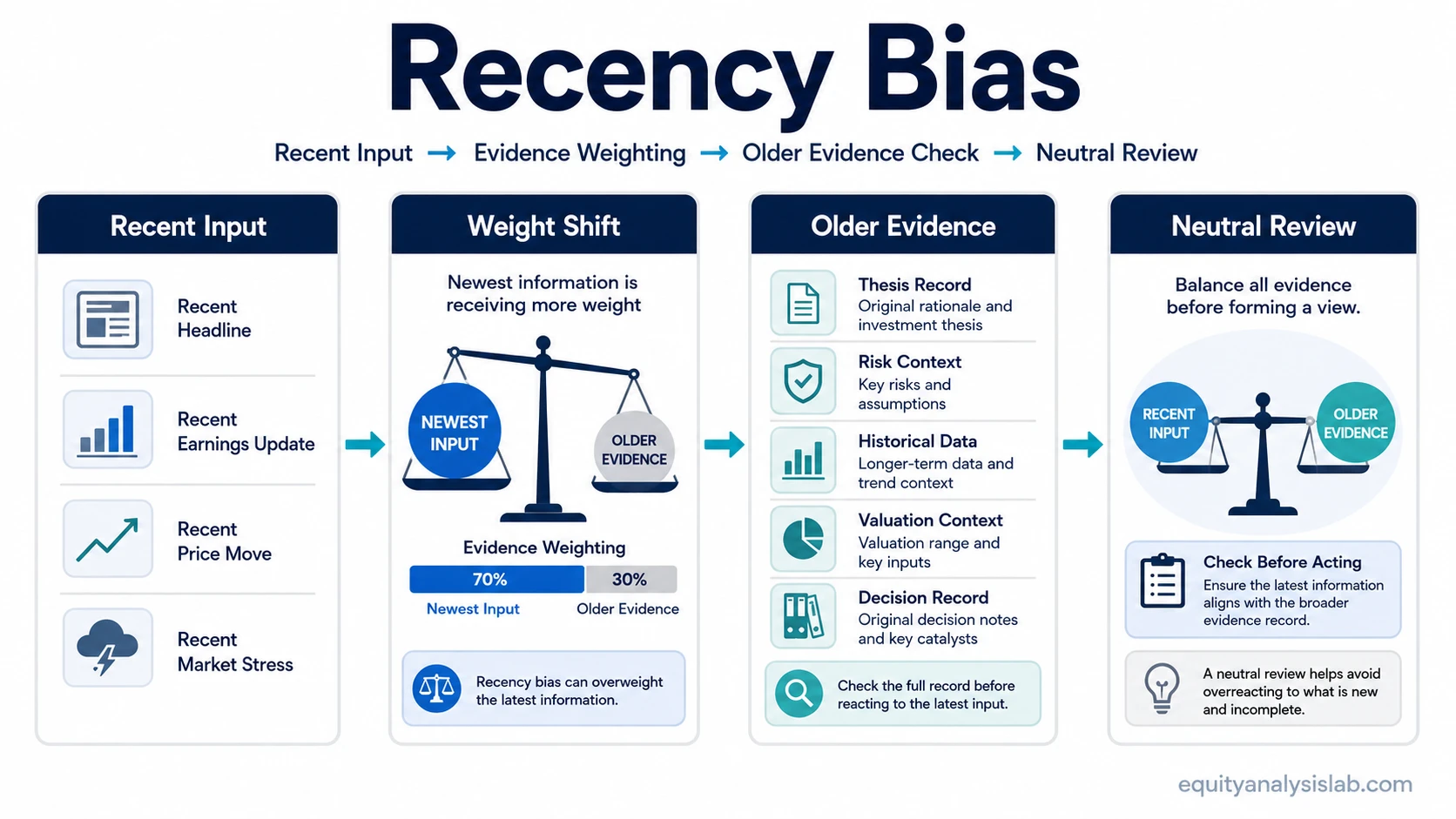

Recency bias is a behavioral bias in which the newest information receives more weight than the broader evidence base. In investing, it can appear when recent returns, headlines, earnings updates, price moves, or market stress dominate the review of a company, thesis, or portfolio decision.

Recent evidence can be important. The problem begins when the latest input is treated as the whole picture before it is compared with older data, prior assumptions, risk context, valuation context, and the original decision record.

Definition: Recency bias is the tendency to give disproportionate weight to the most recent information when forming a judgment. In investor psychology, it can make the latest market or company input feel more representative than the longer decision record.

Key Points

- Recency bias gives extra weight to the newest evidence, even when older evidence remains relevant.

- In investing, it can affect the review of recent returns, earnings updates, headlines, price action, or drawdowns.

- It differs from availability bias, anchoring bias, confirmation bias, and the recency effect.

- A neutral review compares recent input with the original thesis record, not with emotion alone.

- Recency bias does not prove that a specific portfolio action is correct or required.

What Is Recency Bias?

Recency bias is a cognitive and behavioral-finance bias. It occurs when the latest information feels more meaningful than earlier evidence simply because it is fresh, vivid, or emotionally close.

For an investor, the bias can appear after a sharp rally, a sudden decline, a strong earnings report, a disappointing update, or a short period of market stress. The latest input may feel like a new truth even when the longer record is mixed, incomplete, or unchanged.

The bias is not the same as noticing new evidence. New information can legitimately change an investment view. Recency bias becomes a concern when the newest input receives extra weight before the investor checks whether it actually changes the thesis, valuation context, business evidence, risk assumptions, or portfolio criteria.

How Recency Bias Affects Investor Decisions

Recency bias changes the weight assigned to evidence. A recent price decline can make a long-term thesis feel weaker than the underlying business evidence suggests. A recent rally can make a company feel stronger even if valuation, margins, cash flow, or competitive position have not improved enough to support that feeling.

The decision process often changes in a simple sequence. A recent input appears. Older evidence receives less attention. The original checklist becomes easier to bypass. Position-size pressure, regret, fear of missing out, or portfolio-review pressure begins to influence the interpretation. A neutral evidence-weighting check then has to separate new information from new emotion.

Illustrative scenario: A stock reports one strong quarter after several years of inconsistent margins and weak cash conversion. Recency bias can make the latest earnings update feel like a complete business turnaround. A fuller review would compare the new quarter with multi-period margin trends, cash flow quality, balance-sheet risk, valuation assumptions, and the original thesis criteria.

The same pattern can work in the opposite direction. A holding may fall during a short period of market stress, and the recent decline can dominate the investor’s memory of why the position existed. A review based only on that decline may miss whether the company’s long-term evidence has actually deteriorated.

Why Recent Evidence Feels Stronger

Recent information is easier to notice because it is closer to the decision moment. It may also be more emotional. A fresh loss, a sudden gain, a surprising earnings headline, or a sharp move in a sector can create a stronger impression than older evidence stored in notes, filings, models, or prior research.

The bias can be stronger when the latest development is easy to explain with a simple story. A recent rally can be interpreted as confirmation that conditions have improved. A recent drawdown can be interpreted as proof that the original thesis has failed. Both interpretations may be incomplete if the investor has not checked the broader evidence base.

Common mistake: The newest information is treated as decisive before it is tested against the original thesis, the longer evidence window, and the conditions that were supposed to change the decision.

Recent Input vs Full Evidence Review

A useful review does not reject recent evidence. It asks what the recent input changes. The difference is important because a recent development can be relevant without being sufficient on its own.

| Recent input | Recency-biased interpretation | Full evidence review |

|---|---|---|

| One strong earnings update | The company has turned around. | Compare the update with multi-period revenue quality, margins, cash flow, balance-sheet risk, and prior thesis assumptions. |

| Short-term price rally | The investment case is now stronger. | Check whether the rally reflects improved fundamentals, valuation changes, sentiment, liquidity, or temporary positioning. |

| Recent drawdown | The original thesis has failed. | Separate market-wide pressure from company-specific evidence, and compare the decline with the original risk criteria. |

| New headline or analyst comment | The headline changes the whole decision. | Review whether the information changes the business model, earnings quality, valuation assumptions, or risk context. |

| Recent sector strength | Every company in the sector now deserves a better interpretation. | Distinguish sector-level momentum from company-level quality, balance-sheet strength, and durable cash generation. |

The full evidence review keeps the latest information in the process without allowing it to erase the rest of the record.

How to Review Recency Bias Neutrally

Recency bias review works best as a neutral evidence check. It does not answer whether a security is attractive, whether a portfolio is suitable, or whether a position requires action. It only tests whether the newest information has been given more weight than the broader record supports.

Neutral review sequence:

- Identify the recent input that is influencing the judgment.

- Write down the older evidence that may be receiving less attention.

- Compare the new input with the original thesis, valuation assumptions, and risk criteria.

- Check whether portfolio pressure, regret, fear, or excitement is changing the evidence weight.

- Decide whether the evidence record has changed, without treating the review as a portfolio instruction.

A written decision record can help because it separates the original reasons from the latest emotional pressure. Predefined criteria can also make the review more consistent. The goal is not to remove judgment. The goal is to make the evidence weighting visible.

Recency Bias vs Availability, Anchoring, and Confirmation Bias

Recency bias is often confused with nearby behavioral biases. The distinctions matter because each bias changes the decision process in a different way.

| Bias or effect | Main distortion | Investor-review distinction |

|---|---|---|

| anchoring bias | Sticking too closely to an initial reference point. | The issue is the first anchor, not necessarily the newest evidence. |

| availability bias | Giving more weight to information that is easiest to recall or most salient. | The information may be memorable without being the most recent. |

| selective evidence filtering | Favoring evidence that supports an existing belief. | The issue is thesis defense; recency bias can appear even before a fixed view is formed. |

| Recency effect | Greater recall or influence from items presented last. | The effect is often discussed in memory and order-of-information contexts; recency bias in investing is more about evidence weighting in a decision review. |

These biases can overlap. A recent headline may also be easy to recall, confirm an existing thesis, or pull judgment away from an earlier reference point. The cleaner review question is which part of the evidence process is being distorted.

When Recent Evidence Is Actually Relevant

Recent evidence is not automatically noise. A new earnings report, management change, financing event, competitive development, or balance-sheet issue can materially change the investment case. Recency bias review becomes useful because it asks whether the new information changes the underlying evidence, not whether it is recent.

Limitation: Recency bias is a review lens, not a portfolio action rule. It does not prove that an investor is wrong, that recent evidence should be ignored, or that any buy, sell, hold, allocation, or rebalancing decision is required.

The safest interpretation is procedural. Recent information deserves attention when it changes the thesis, risk context, valuation assumptions, or portfolio criteria. It becomes a bias risk when its freshness replaces that review.

FAQ

What is recency bias?

Recency bias is the tendency to give disproportionate weight to the newest information. In investing, it can make recent returns, headlines, earnings updates, or price moves feel more important than the full evidence record.

What is the difference between recency bias and availability bias?

Recency bias gives extra weight to the newest information. Availability bias gives extra weight to information that is easiest to recall or most vivid, even if it is not the newest information.

How can recency bias be reviewed without making portfolio advice?

A neutral review compares the latest input with the original decision record, longer evidence window, thesis criteria, and risk assumptions. The review checks evidence weighting; it does not prescribe a portfolio action.