Herd behavior can affect investors when crowd action, market popularity, or social proof changes the evidence standard before the investment thesis has been reviewed independently.

Definition: In investing, herd behavior means following or overweighting the actions of other investors instead of separating crowd evidence from business, valuation, risk, and portfolio evidence.

The bias appears when crowd participation changes the investor’s burden of proof before business, valuation, risk, and portfolio evidence are checked.

Herd behavior is a behavioral finance bias tied to social proof and independent evidence review. A rising level of attention, repeated media coverage, crowded ownership, or visible consensus can start to feel like confirmation even when the original thesis still needs a separate check.

In behavioral finance, the main problem is not that a crowd exists. The problem is that popularity can quietly replace the investor’s own evidence standard.

Key Points

- Herd behavior can make popularity feel like evidence before the investment thesis has been checked.

- The bias often appears when investors rely on social proof, repeated narratives, or visible participation by others.

- A crowded idea is not automatically wrong; the risk is skipped independent review.

- A written checklist keeps popularity from replacing business, valuation, risk, and portfolio evidence.

How Herd Behavior Changes Investor Review

Herd behavior usually starts with an outside cue. A stock, sector, fund, market theme, or investing narrative becomes widely discussed. The attention itself can create pressure because other investors appear to have already reached a conclusion.

That pressure can change how evidence is weighted. Supportive information may be accepted quickly because it matches the crowd’s direction. Contrary information may feel easier to postpone, explain away, or treat as temporary. The decision may still look evidence-based, but the starting point has shifted from thesis review to popularity.

The clearest warning sign is a lower burden of proof. If valuation concerns, business-model risks, balance-sheet weakness, earnings quality, or portfolio concentration receive less attention because many others already agree, crowd action is no longer just background information.

Recent or vivid crowd evidence can also overlap with availability bias, especially when repeated headlines or social discussion make one interpretation easier to recall than the full evidence set.

Observable Investor Decision Sequence

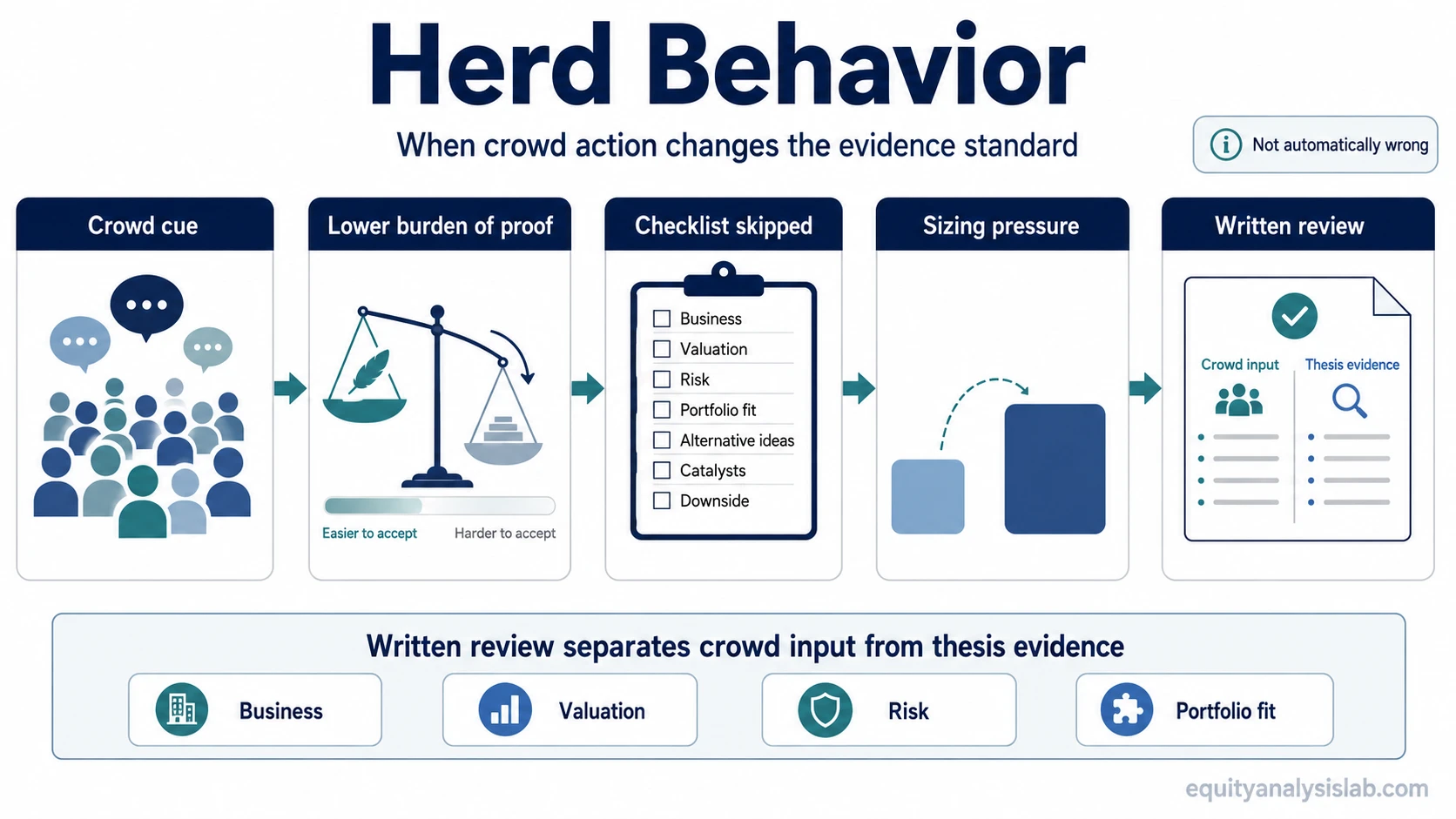

Herd behavior becomes easier to identify when the review is broken into observable steps: the crowd creates the trigger, the evidence standard weakens, the checklist is skipped, sizing pressure increases, and the written review restores separation.

| Decision step | How herd behavior can appear | Review guardrail |

|---|---|---|

| Decision trigger | A stock, sector, or theme becomes widely discussed, heavily owned, or treated as an obvious opportunity. | Write down the original reason for reviewing it before reading more crowd commentary. |

| Evidence ignored | Valuation, business quality, balance-sheet risk, or thesis uncertainty receives less attention because participation by others feels reassuring. | List the evidence that would matter if the idea were unpopular. |

| Checklist failure | The investor skips normal review steps because the crowd appears to have already validated the idea. | Use the same review checklist applied to less popular holdings or ideas. |

| Position sizing pressure | The investor feels pressure to own more than the evidence, risk budget, or portfolio role supports. | Separate thesis confidence from position size and portfolio concentration. |

| Written review mechanism | The decision becomes easier to justify after the crowd has already moved. | Record the independent thesis, contrary evidence, valuation view, and risk limits before making a decision. |

Simple Herd Behavior Example in Investing

A stock becomes widely discussed after strong recent attention around its industry. Many investors describe the theme as inevitable, and the company’s share price has already moved sharply. An investor who had not previously reviewed the business begins treating the popularity of the idea as evidence that the thesis must be strong.

The investor reads commentary before reading the earnings release, so the later review starts with the crowd’s conclusion already in mind. Revenue growth, margins, competitive position, or cash flow could still support part of the thesis. The problem appears when valuation, balance-sheet risk, business durability, and portfolio exposure receive less independent attention.

The cleaner review writes the business case, valuation concern, contrary evidence, and portfolio role before deciding how much weight the crowd’s interest deserves.

Limitations and Common Mistakes

Limitation: Herd behavior does not prove that the crowd is wrong. A widely followed idea can still have strong business evidence, improving fundamentals, reasonable valuation support, or a clear portfolio role.

The useful distinction is between crowd confirmation and independent confirmation. Crowd confirmation says many people appear to agree. Independent confirmation checks whether the investment thesis still holds after business quality, valuation, risk, time horizon, and portfolio fit are reviewed on their own.

Common mistake: Treating popularity as a shortcut for due diligence. Popularity can point attention toward an idea, but it cannot replace the work of checking what the company is worth, what could impair the thesis, and how the position fits the portfolio.

Another mistake is automatic contrarianism. Rejecting an idea only because it is popular still lets the crowd control the decision. The review standard should remain the same whether the idea is crowded, ignored, praised, or criticized.

Herd Behavior Compared With Nearby Biases

Herd behavior is specifically about crowd action or social proof changing the investor’s evidence standard. Nearby biases can overlap, but they distort the review in different ways.

| Bias | Main distortion | How it differs from herd behavior |

|---|---|---|

| Herd behavior | Crowd action becomes a substitute for independent evidence review. | The pressure comes from what other investors appear to be doing or believing. |

| anchoring bias | An early reference point receives too much weight. | The pressure comes from a fixed reference point, not from the crowd. |

| Availability bias | Easy-to-recall information feels more representative than it may be. | The pressure comes from mental prominence, which may or may not be crowd-driven. |

| Confirmation bias | Evidence that supports an existing thesis is easier to accept. | The pressure comes from protecting a belief, not necessarily from following others. |

The practical boundary is the source of the pressure. If the investor is pulled toward a decision because others appear to agree, herd behavior is the central concern. If the investor is pulled by an earlier number, a recent headline, or a preferred thesis, another bias may be doing more of the work.

How to Review Herd Behavior Without Using Popularity as Proof

Herd behavior should be reviewed as a process risk, not as a shortcut for judging an investment. The fact that many investors like or dislike an idea does not by itself say what the investment is worth, what the company will earn, or how the portfolio should be positioned.

A useful review starts by separating crowd input from thesis evidence. Crowd input may explain why the idea is visible. Thesis evidence must still come from the business, valuation, financial quality, risk factors, time horizon, and portfolio role.

Review mechanism: Write the investment case as if the idea were not popular. Then write the strongest reason the crowd might be right, the strongest reason the crowd might be overconfident, and the evidence that would change the conclusion.

This keeps social proof from becoming proof. It also prevents the opposite mistake: rejecting a valid idea only because many people have already noticed it.

FAQ

What is herd behavior in investing?

Herd behavior in investing means following or overweighting what other investors are doing instead of independently reviewing the business, valuation, risk, and portfolio evidence.

Is herd behavior always irrational?

No. A crowd can respond to real information. The risk is not agreement itself, but allowing agreement by others to replace independent evidence review.