Overconfidence bias in investing is the tendency to place too much weight on one’s own judgment, skill, or information before the investment evidence has been reviewed carefully enough. The problem is not confidence by itself. The risk appears when confidence lowers the evidence threshold for business quality, valuation, risk, and portfolio exposure.

Definition: Overconfidence bias is a behavioral finance bias where an investor overestimates the reliability of their own analysis, forecasting ability, or information advantage. In an investment process, it can make supportive evidence feel sufficient while contrary evidence receives less review.

Key Points

- Overconfidence bias is not the same as ordinary confidence in an investment thesis.

- The practical risk is a lower evidence threshold before a decision is reviewed.

- It can appear through ignored contrary data, frequent trading, concentration, or oversized conviction.

- A written review checklist can separate confidence from current thesis evidence.

- The bias does not prove that an investment decision is automatically wrong.

What Overconfidence Bias Means in Investing

In investing, overconfidence bias changes the way evidence is weighed. A confident investor may treat a thesis as stronger than it is because the idea feels familiar, internally consistent, or supported by several visible data points.

The bias becomes more important when confidence starts replacing review. A company can still have a strong business, an attractive valuation, or improving fundamentals, but the decision process weakens if negative evidence is dismissed before it is examined.

Some investment decisions require conviction, but conviction still needs a disciplined evidence check. The issue is not having a view. The issue is allowing the strength of that view to reduce the quality of the evidence check.

How Overconfidence Changes the Evidence Threshold

Overconfidence can make an investment idea feel “reviewed” before the review is complete. The investor may believe they understand the business, the valuation range, or the downside risk well enough, even though important parts of the thesis have not been tested.

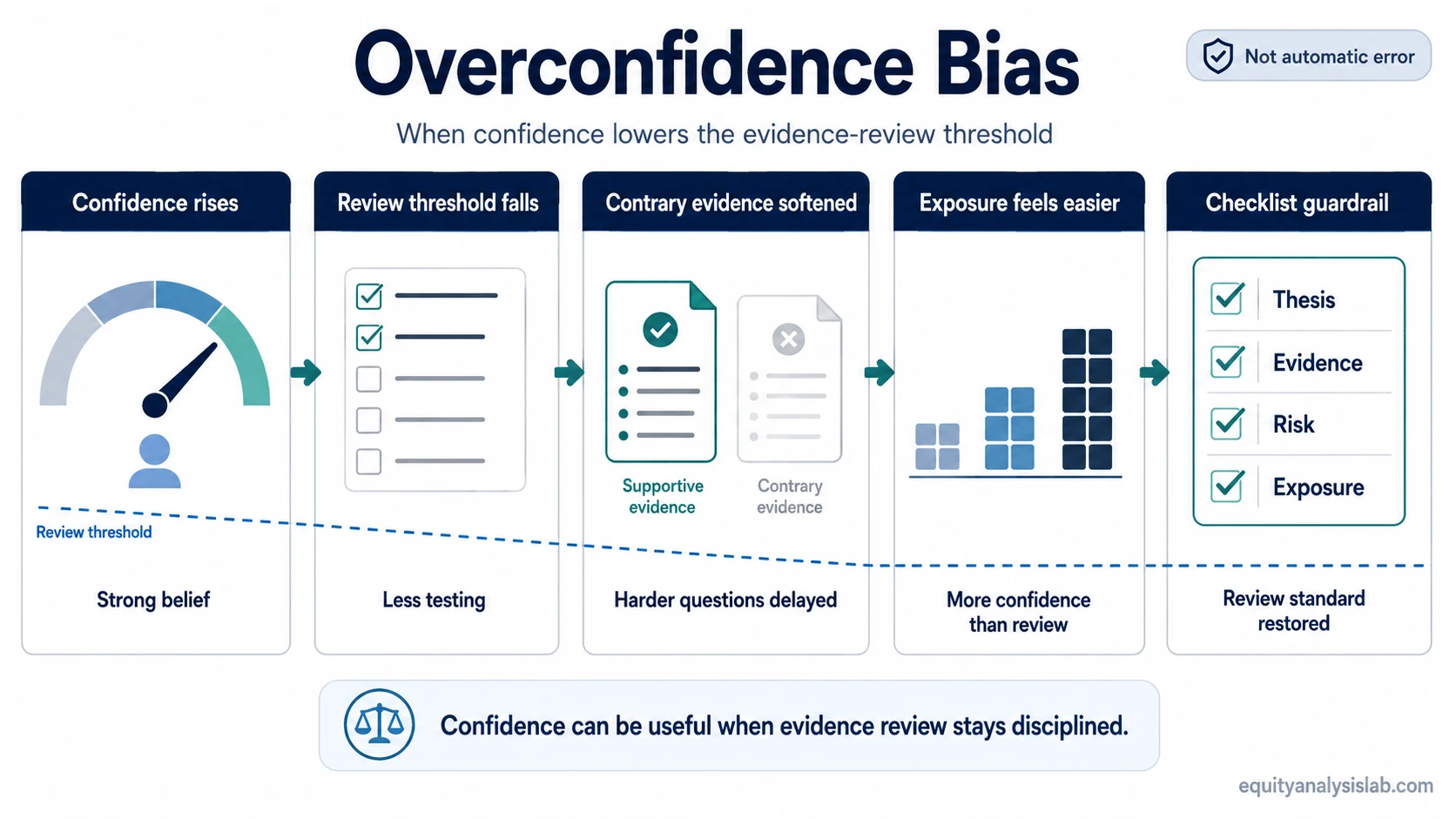

The mechanism is usually gradual. Confidence rises first. Then the investor accepts supportive information faster, softens contradictory information, and spends less time checking whether position size, valuation risk, or portfolio concentration still fit the evidence.

Evidence-review sequence: confidence rises → the review threshold falls → contrary data feels less important → sizing or concentration becomes easier to justify → the written thesis check becomes weaker.

Observable Signs in Investor Decisions

Overconfidence is easier to identify through decision behavior than through emotion. The useful question is not whether the investor feels confident, but whether the process still checks evidence with the same discipline after confidence rises.

| Observable trigger | Evidence that may be ignored | Investor decision risk | Review guardrail |

|---|---|---|---|

| A thesis feels obvious after several supportive reports or comments. | Valuation sensitivity, margin pressure, balance-sheet risk, or weak cash conversion. | The investor may treat agreement as evidence quality. | Write the strongest contrary case before changing exposure. |

| The investor trades the idea more frequently after early confirmation. | Transaction costs, tax effects, changed risk/reward, or weaker thesis quality. | Frequent action can replace patient evidence review. | Require a reason that is tied to new evidence, not only renewed conviction. |

| The position becomes larger because the thesis feels increasingly certain. | Portfolio concentration, correlation with existing holdings, and downside scenario size. | Position sizing can expand faster than the evidence base. | Check exposure against thesis uncertainty and portfolio-level risk. |

| Contrary data is treated as temporary noise. | Earnings quality deterioration, guidance weakness, dilution, or business model risk. | The thesis may survive by explanation instead of evidence. | Define what evidence would actually weaken or change the thesis. |

| Online information creates a sense of deep understanding. | Unknowns outside the visible narrative, management execution risk, or industry cyclicality. | Information volume can be mistaken for information completeness. | Separate what is known, estimated, assumed, and still untested. |

Confidence vs Evidence Quality

Confidence describes the investor’s strength of belief. Evidence quality describes how well the thesis has been tested against business facts, valuation assumptions, risk, and alternative explanations. Those two things can move together, but they are not the same.

A confident thesis may still be evidence-based if the investor has reviewed downside scenarios, checked valuation assumptions, and defined what would weaken the view. A weak thesis can also feel confident if the investor has only reviewed supportive information.

This is where overconfidence differs from favoring evidence that supports an existing view. Confirmation bias focuses on the direction of evidence selection. Overconfidence bias focuses on the level of certainty assigned to the investor’s own judgment.

A Short Checklist Scenario

An investor studies a company and becomes confident after reading several supportive notes about its growth, management, and market opportunity. Before increasing exposure, a written checklist forces separate review of valuation, balance-sheet risk, earnings quality, contrary evidence, and current portfolio concentration.

The checklist does not automatically reduce conviction. It prevents conviction from replacing evidence review. If the thesis remains strong after the checklist, confidence is supported by process rather than by familiarity alone.

Where Overconfidence Often Appears

Overconfidence can show up in several parts of an investing workflow. It may appear before purchase, when the investor believes the opportunity is clearer than it is. It may appear after early success, when the investor starts treating a previous correct call as evidence of repeatable forecasting skill. It may also appear during review, when negative information is explained away too quickly.

The portfolio effect is often more important than the single decision. A thesis that is only moderately overconfident can become much riskier if it leads to larger sizing, reduced diversification, or repeated additions without a fresh review of evidence.

Common Mistake: Confusing Conviction With Evidence Quality

Common mistake: treating a strong feeling of conviction as proof that the investment case has been reviewed well.

Conviction can be useful when it is built from tested assumptions, risk awareness, and a clear view of what would change the thesis. It becomes weaker when it grows mainly from repetition, agreement, recent success, or the feeling that the investor has special insight.

How Overconfidence Differs From Nearby Biases

Several behavioral biases affect evidence review, but they do not all work the same way. Overconfidence is specifically about the investor assigning too much reliability to their own judgment or information set.

| Bias | Main evidence problem | Investor-process distinction |

|---|---|---|

| Anchoring bias | Too much weight is placed on a reference point. | The decision is pulled toward an initial price, estimate, or valuation marker. |

| Availability bias | Recent, vivid, or easy-to-recall information receives too much weight. | Availability-driven confidence can rise because the most visible information feels more representative than it is. |

| Confirmation bias | Supportive information is easier to accept than conflicting information. | The evidence search becomes tilted toward the existing thesis. |

| Overconfidence bias | The investor gives too much reliability to their own judgment. | The review threshold falls because the investor feels the decision is already well understood. |

Limits of the Concept

Overconfidence bias does not mean the investor is automatically wrong, irrational, or unable to make a good decision. A confident investment view can be reasonable when it is supported by business evidence, valuation discipline, risk review, and portfolio awareness.

The concept is most useful as a process check. It asks whether confidence has changed the standard of review. If the standard remains disciplined, confidence can coexist with careful analysis.

Practical Review Guardrails

A simple review guardrail is to separate four items before the decision changes: the thesis, the evidence, the risk, and the exposure. Each item should be written clearly enough that another person could understand what is known, what is assumed, and what would weaken the case.

| Review question | Why it matters |

|---|---|

| What evidence supports the thesis? | Separates real evidence from repeated narrative or agreement. |

| What evidence conflicts with the thesis? | Prevents confidence from filtering out inconvenient information. |

| Which assumptions matter most? | Identifies whether the case depends on fragile forecasts or valuation inputs. |

| What would reduce or break the thesis? | Creates a review standard before the investor becomes more attached to the idea. |

| How large is the exposure in portfolio context? | Connects confidence to concentration, diversification, and downside tolerance. |

FAQ

Is overconfidence bias always bad for investors?

No. Confidence can help an investor act when evidence is strong. The bias becomes a problem when confidence reduces the quality of the review process or makes contrary evidence easier to dismiss.

How is overconfidence bias different from confirmation bias?

Overconfidence bias is about assigning too much reliability to one’s own judgment. Confirmation bias is about giving more weight to evidence that supports an existing view than to evidence that challenges it.

Can a correct investment decision still involve overconfidence?

Yes. A decision can have a good outcome even if the review process was weak. Process quality and outcome are related, but they are not the same thing.