The disposition effect is a behavioral finance bias in which investors are more likely to sell winning investments too soon and hold losing investments too long. It is a decision-review concept, not proof that any specific position should be sold, held, trimmed, or added to.

The bias matters because the investor may begin reacting to the feeling of realizing a gain or loss instead of reviewing the updated investment evidence. A realized gain can feel safe because it confirms a successful decision. A realized loss can feel uncomfortable because it makes the mistake visible. The disposition effect describes that pressure, but it does not replace valuation work, thesis review, risk control, tax planning, liquidity needs, or portfolio rules.

Key Points

- The disposition effect describes the tendency to sell winners too early and hold losers too long.

- The bias often relates to reference points, regret avoidance, mental accounting and loss aversion.

- It can distort evidence review when realized gain or loss becomes more important than current investment evidence.

- It does not prove that every sale of a winner or every hold of a loser is irrational.

- A checklist can help separate evidence-based decisions from realization-driven decisions.

What Is the Disposition Effect?

The disposition effect is an investor psychology pattern where a winning position is sold mainly because locking in the gain feels satisfying, while a losing position is kept mainly because realizing the loss feels painful. The purchase price often becomes the emotional reference point. Once that reference point dominates the decision, the investor may judge the position by gain or loss status instead of by current evidence.

This is why the disposition effect is closely connected to anchoring bias. The investor may keep comparing the position to the original purchase price, a prior high, or a desired break-even level. That comparison can matter emotionally even when the business evidence, valuation context, risk profile or portfolio role has changed.

| What it is | What it is not |

|---|---|

| A behavioral finance bias | A portfolio recommendation |

| A lens for reviewing sale and hold behavior | Proof that a winning investment must be held |

| A way to identify realization pressure | Proof that a losing investment must be sold |

| A decision-process risk | A return forecast, suitability test or allocation rule |

How the Disposition Effect Distorts Investor Decisions

The disposition effect works through a simple shift in attention. Instead of asking whether the current evidence still supports the position, the investor starts asking how the decision will feel after the gain or loss is realized. That emotional accounting can change the timing and quality of the decision.

A winning position may be sold because the investor wants to preserve the feeling of being right. A losing position may be held because the investor wants to avoid confirming a mistake. In both cases, the decision can become less connected to the forward-looking question: has the investment thesis improved, weakened or stayed intact?

The bias can also affect evidence selection. An investor may give more weight to information that justifies keeping a loser or selling a winner, while dismissing contrary evidence. That can overlap with availability-driven evidence filtering when the easiest or most emotionally convenient information receives more attention than the full evidence set.

Why Investors Sell Winners and Hold Losers

Several mechanisms can reinforce the disposition effect. A reference point creates the gain or loss frame. Regret avoidance makes a realized loss feel like an admission of error. Mental accounting can turn each position into a separate emotional account, even when the portfolio should be reviewed as a whole. Loss aversion can make the pain of realizing a loss feel larger than the satisfaction of realizing a comparable gain.

The result is a risk-behavior shift. The investor may become risk-averse in a winning position because the gain feels worth protecting, while becoming risk-seeking in a losing position because waiting preserves the possibility of getting back to even. That does not mean the investor is always wrong. It means the reason for the decision needs to be separated from the emotional comfort of realizing or avoiding a result.

What the Disposition Effect Is Not

The disposition effect is not a rule that winners should always be held longer or losers should always be sold faster. Selling a winner can be rational if valuation becomes stretched, the thesis weakens, risk becomes too concentrated, or a portfolio rule requires trimming. Holding a loser can also be rational if the original thesis remains intact, the risk is controlled, and the current evidence still supports the position.

The cleaner review is whether the decision still makes sense after the emotional pressure of the unrealized gain or loss is removed.

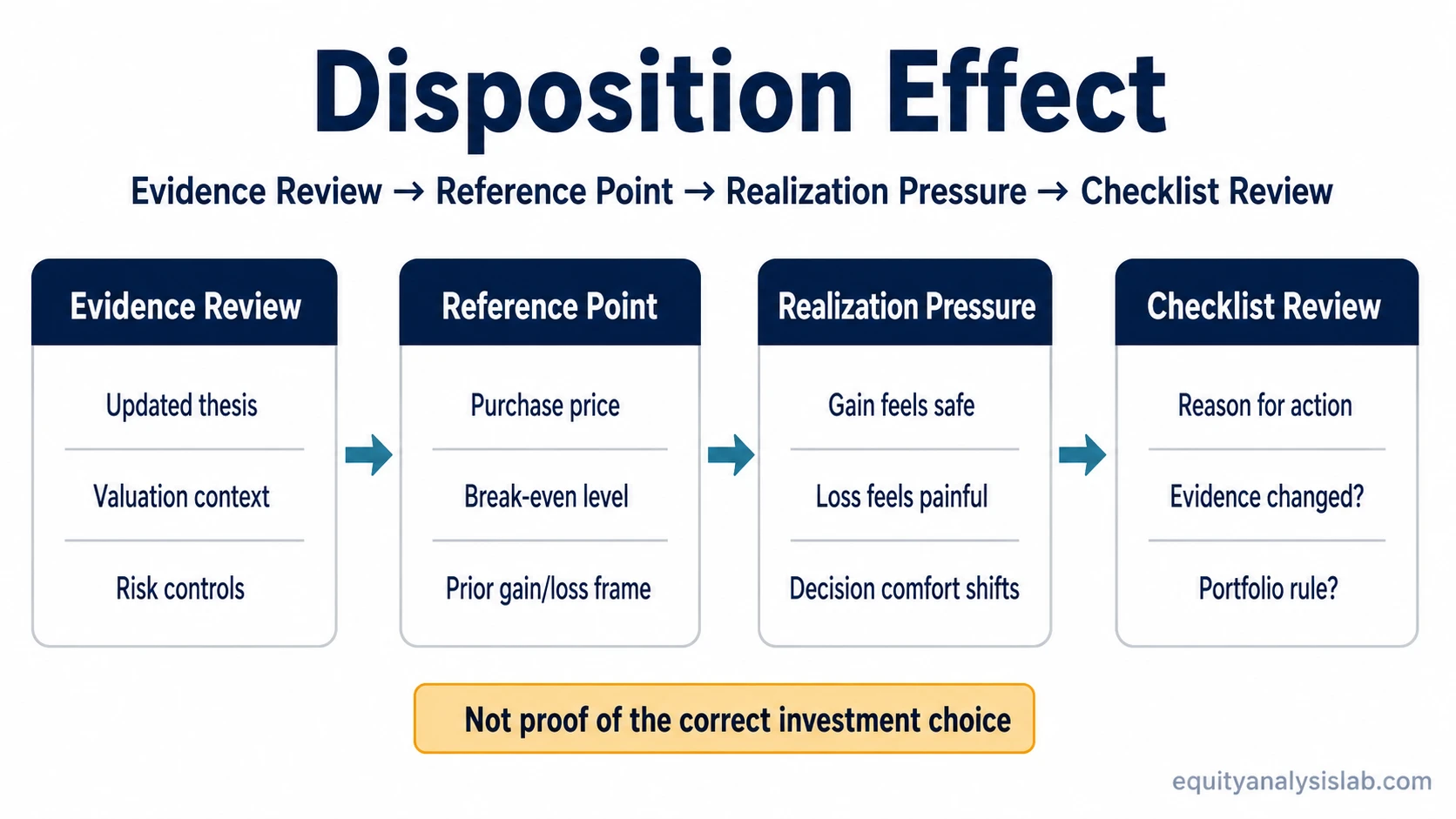

Disposition Effect Checklist for Reviewing a Decision

A practical review can make the bias more observable. The checklist below does not tell an investor what to do. It helps identify whether the decision is being driven by evidence or by the desire to realize, avoid, protect or reverse a gain or loss.

| Checklist input | What it tests |

|---|---|

| Decision trigger | Is the sale or hold decision triggered by updated evidence, or mainly by the feeling of realizing a gain or loss? |

| Evidence ignored | Is new information being dismissed because it conflicts with the preferred realization outcome? |

| Reference-point test | Would the same decision still make sense if the purchase price were unknown? |

| Position-size pressure | Is the position being allowed to drift because reducing it would make discomfort visible? |

| Review mechanism | Is there a written reason to keep, trim, exit or reassess based on thesis evidence rather than realization feeling? |

For a single investor decision, the practical test is direct: compare the action against the thesis, valuation, risk and evidence, not only against the entry price.

Example: Reviewing a Winning and Losing Position

An investor may have one position up 38% after steady earnings progress and another down 17% after repeated margin pressure. The winning position still has improving evidence: business quality remains strong, cash flow is stable, and the valuation case has not obviously broken. The losing position has weaker evidence: the original thesis is less clear, risk has increased, and the investor is mostly waiting for the price to return to the purchase level.

The disposition effect can appear if the investor sells the winner mainly to feel the gain and keeps the loser mainly to avoid realizing the loss. A cleaner review would ask what changed in the evidence, whether the same decision would be made without knowing the purchase price, and whether the position is being judged by thesis quality or by realization comfort.

The scenario is illustrative. It does not imply that the winner should be held or that the loser should be sold. It shows how the bias can enter the decision before the investment analysis is complete.

Disposition Effect vs Related Behavioral Biases

The disposition effect overlaps with several behavioral concepts, but it has a specific focus. It is mainly about the tendency to realize gains more readily than losses. Related biases can explain why that behavior becomes attractive.

| Related concept | How it differs |

|---|---|

| Loss aversion | Explains why realizing a loss can feel especially painful, but it is broader than sale and hold behavior. |

| Mental accounting | Explains why each position may be treated as its own emotional account instead of part of a portfolio review. |

| Anchoring | Explains why the purchase price or break-even level can become the reference point for the decision. |

| Endowment effect | Focuses more on ownership attachment and perceived value, while the disposition effect focuses on realizing gains and avoiding realized losses. |

The related-bias distinction matters because a sale or hold decision can have more than one psychological driver. The disposition effect describes the realization pattern. The availability bias can affect which evidence is noticed first. The ownership attachment problem can make a held position feel more valuable simply because it is already owned.

Common Mistakes When Using the Disposition Effect

Mistake 1: Treating the bias as proof that a specific decision is wrong. A biased pressure can exist even when the final decision is still reasonable for other reasons.

Mistake 2: Ignoring taxes, liquidity needs, portfolio rules or concentration limits. These can affect whether realizing a gain or loss is rational in a specific context.

Mistake 3: Replacing investment analysis with bias labels. The label is only useful if it improves the review of evidence, risk and thesis quality.

FAQ

Is the disposition effect always irrational?

No. The disposition effect describes a bias risk, not a guaranteed error. Selling a winner or holding a loser can be rational when the decision is supported by valuation, thesis evidence, tax planning, risk controls or portfolio rules.

Why does the disposition effect make investors hold losing positions?

A losing position can be held because realizing the loss feels like confirming a mistake. The investor may wait for the price to return to the purchase level even when the current evidence no longer supports the original thesis.

How can an investor review for the disposition effect?

A useful review asks whether the decision would still make sense without knowing the purchase price, whether new evidence is being ignored, and whether the reason to hold, trim, sell or reassess is written in evidence-based terms.