Monthly recurring revenue is the normalized recurring subscription revenue a SaaS company expects to receive each month from active paying customers.

MRR helps investors read recurring revenue momentum, but it is not a complete measure of profitability, cash conversion, retention quality, valuation support, or business durability. The metric becomes more useful when the active customer base, contract normalization, exclusions, movement components, and cash-flow boundary are visible.

The strongest reading follows MRR from the reported number back to the recurring base, monthly normalization, excluded revenue, customer movement, retention context, and accounting boundary.

Definition: Monthly recurring revenue, or MRR, is recurring subscription revenue normalized to a monthly amount. It usually focuses on active paid subscriptions or accounts, not one-time fees, non-recurring services, or future pipeline.

Key Points

- MRR measures recurring monthly subscription revenue, not total revenue, recognized revenue, cash flow, or profit.

- The basic formula is active paying customers or accounts multiplied by average recurring monthly revenue.

- Annual, quarterly, discounted, paused, trial, and usage-based contracts need careful normalization before MRR is comparable.

- MRR growth is higher quality when it comes from durable recurring demand, expansion, and retention rather than churn replacement alone.

- Investors should compare MRR with retention, margins, cash conversion, and disclosed metric definitions before relying on the trend.

What Monthly Recurring Revenue Measures

Monthly recurring revenue measures the recurring revenue base that a SaaS company expects to repeat each month from active paid customers. The metric turns subscription activity into a comparable monthly run-rate figure.

The cleanest MRR reading starts with paid recurring subscriptions, applies a consistent monthly normalization method, and removes revenue that is not expected to repeat. Without that boundary, MRR can look stronger than the recurring base actually is.

Investor boundary: MRR can support recurring-revenue analysis, but it still needs to be checked against cash conversion, gross margin, retention, sales efficiency, dilution, and valuation context.

MRR Formula and Required Inputs

The basic MRR formula is:

MRR = active paying customers or accounts × average recurring monthly revenue per customer or account

Some companies calculate MRR from customer count and average revenue per account. Others build MRR from contract-level recurring charges. The investor question is not only which formula appears, but whether the same method is used consistently across periods, segments, and product lines.

| Formula input | What it should represent | Investor check |

|---|---|---|

| Active recurring base | Paying customers, accounts, or subscriptions expected to repeat | Check whether trials, paused customers, inactive accounts, or non-paying users are excluded. |

| Average recurring monthly revenue | Recurring monthly revenue per customer or account | Check whether discounts, credits, and contract changes distort the average. |

| Contract normalization | Annual, quarterly, or multi-period contracts converted into a monthly amount | Check whether the company separates billing timing from the recurring monthly run rate. |

| Consistent period treatment | The same calculation logic applied across reporting periods | Check whether a method change created apparent MRR growth or decline. |

MRR is a recurring revenue metric, not a ratio. It becomes less comparable when a company changes what counts as active, changes the average revenue base, or mixes contracted recurring revenue with revenue that may not repeat.

What to Include, Exclude, and Treat With Caution

The strongest MRR calculation separates recurring subscription revenue from items that may increase short-term reported revenue without improving the recurring base.

| Category | Treatment in MRR | Why it matters |

|---|---|---|

| Recurring subscription fees | Include when tied to active paid subscriptions or accounts | These fees represent the recurring monthly base MRR is meant to measure. |

| Annual or quarterly contracts | Include only after consistent monthly normalization | Billing period should not be confused with monthly recurring run rate. |

| One-time setup fees | Exclude | They can raise revenue without increasing recurring subscription value. |

| Implementation or consulting services | Exclude unless truly recurring and subscription-like | Service revenue may have different margin, renewal, and repeatability characteristics. |

| Free trials and unpaid users | Exclude | They do not represent paid recurring revenue. |

| Discounts, credits, and pauses | Treat with caution | Gross subscription value may overstate the revenue actually expected each month. |

| Usage-based revenue | Treat with caution unless recurring and predictable | Variable usage can behave differently from committed subscription revenue. |

How MRR Changes: New, Expansion, Contraction, Churn, and Reactivation

MRR movement matters because the same ending MRR number can come from very different business conditions. A company replacing lost revenue with new sales is not showing the same quality as a company expanding within a stable retained base.

| MRR component | Meaning | Investor interpretation |

|---|---|---|

| New MRR | Recurring revenue from new customers or accounts | Can show acquisition momentum, but should be compared with acquisition cost and payback quality. |

| Expansion MRR | Additional recurring revenue from existing customers | Can indicate product depth, pricing power, seat growth, usage growth, or successful upsell. |

| Contraction MRR | Recurring revenue lost from downgrades, lower usage, or reduced seats | Can signal budget pressure, weaker product value, or segment-specific demand weakness. |

| Churned MRR | Recurring revenue lost when customers cancel | Can reveal retention weakness even when headline MRR still grows. |

| Reactivation MRR | Recurring revenue from returning customers | Can help, but should be separated from durable new demand and expansion. |

| Net new MRR | New plus expansion and reactivation, less contraction and churn | Useful only when the positive and negative components are visible enough to judge quality. |

Retention metrics sharpen this reading. Net revenue retention helps show how expansion, contraction, and churn interact inside the existing customer base.

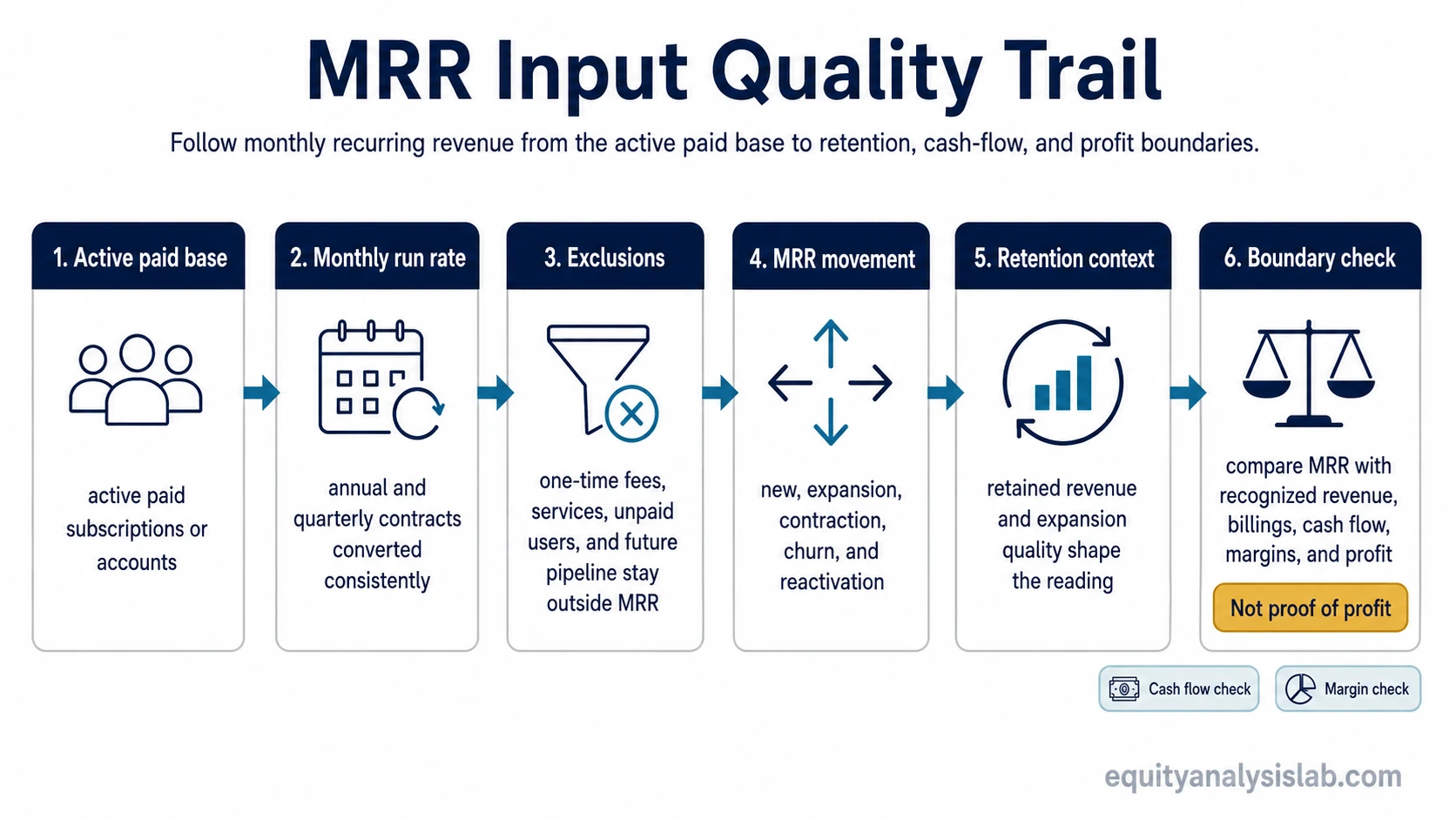

MRR Input Quality Trail

A stronger MRR reading follows the metric from reported monthly recurring revenue back to the inputs that created it. The trail matters because headline MRR can rise while the quality of the recurring base weakens.

| Trail step | Question to ask | Weak reading | Stronger reading |

|---|---|---|---|

| Active recurring base | Which customers or accounts are counted? | Trials, paused accounts, inactive users, or uncertain renewals blur the base. | Only active paid recurring customers or accounts are counted consistently. |

| Normalized monthly period | How are non-monthly contracts converted? | Billing timing creates the appearance of recurring monthly strength. | Annual and quarterly contracts are converted with a stable monthly method. |

| Excluded revenue | What revenue is removed from MRR? | Setup fees, services, or non-recurring charges inflate the recurring base. | One-time and non-recurring revenue stays outside the MRR figure. |

| Movement components | What drove the change in MRR? | New sales hide contraction or churn inside the existing base. | New, expansion, contraction, churn, and reactivation are separated clearly. |

| Retention context | Is existing customer revenue durable? | Headline MRR growth depends on replacing lost customers. | Growth is supported by stable retained revenue and healthy expansion. |

| Accounting and cash-flow boundary | Does MRR convert into reported revenue, cash, and profit? | MRR growth appears strong while collections, margins, or cash conversion remain weak. | Recurring revenue momentum is checked against recognized revenue, billing, cash flow, and margins. |

This trail separates metric movement from business quality. A rising MRR line is more useful when retention, margins, cash conversion, and the economics behind growth also hold up.

MRR vs ARR, Recognized Revenue, Cash Flow, and Retention

MRR and annual recurring revenue describe related subscription run-rate concepts, but they use different time frames. MRR normalizes the recurring base to one month. ARR annualizes recurring subscription value.

| Metric or concept | What it answers | Boundary for investors |

|---|---|---|

| MRR | What recurring subscription revenue is expected each month? | Does not prove recognized revenue, cash collection, profitability, or customer durability. |

| ARR | What is the annualized recurring subscription base? | Can smooth timing, but may hide short-term monthly movement. |

| Recognized revenue | What revenue is reported under accounting rules for the period? | Can differ from billings, collections, and run-rate subscription metrics. |

| Cash flow | How much cash the business actually generates or consumes | MRR growth can coexist with weak collections, high sales costs, or negative free cash flow. |

| Retention | How much customer revenue stays, expands, contracts, or leaves | Headline MRR growth is less informative without retained-revenue context. |

Gross revenue retention helps isolate how much recurring revenue remains before expansion is added back. That boundary is important when new bookings or upsells are masking customer loss.

Accounting limitation: MRR is not a GAAP or IFRS line item. Company definitions can differ, so the calculation should be checked against reported revenue, billings, deferred revenue, cash collections, and disclosed metric definitions where available.

How Investors Interpret MRR

Investors use MRR to understand recurring revenue momentum, but the useful question is how that momentum was produced. A clean increase in MRR is more informative when it comes from durable subscriptions, expansion within existing customers, consistent definitions, and improving unit economics.

MRR becomes weaker evidence when growth depends heavily on replacing churn, including non-recurring revenue, changing the calculation method, or pushing discounts that reduce future revenue quality. The same growth rate can have different implications depending on cohort behavior, customer segment, product mix, gross margin, and cash conversion.

Investor interpretation frame: Start with the reported MRR trend, then separate source of growth, retained base quality, exclusions, margin structure, cash conversion, and valuation context. A higher MRR number answers only the first part of the analysis.

Simple Monthly Recurring Revenue Example

A SaaS company has 500 active paying accounts at the start of the month, with average recurring monthly revenue of $200 per account. The starting MRR is:

500 active accounts × $200 average recurring monthly revenue = $100,000 MRR

During the month, the company adds $20,000 of new MRR and $10,000 of expansion MRR. It also loses $8,000 from contraction and $12,000 from churn. Net new MRR is $10,000, so ending MRR becomes $110,000.

| Movement | Amount | Interpretation |

|---|---|---|

| Starting MRR | $100,000 | Beginning recurring monthly base |

| New MRR | +$20,000 | Recurring revenue from new accounts |

| Expansion MRR | +$10,000 | More recurring revenue from existing accounts |

| Contraction MRR | -$8,000 | Downgrades or reduced recurring spend |

| Churned MRR | -$12,000 | Cancelled recurring revenue |

| Ending MRR | $110,000 | Net monthly recurring revenue after movements |

The ending MRR growth is positive, but the quality is mixed. New sales and expansion added $30,000, while contraction and churn removed $20,000. A stronger case would show lower lost MRR, more expansion from existing customers, and better evidence that the new recurring revenue can convert into cash and margin over time.

Same MRR Growth, Different Quality

Two SaaS companies can both increase MRR by 10 percent while showing different recurring revenue quality.

Company A: MRR rises as existing customers add seats and renew at similar terms. Churn still exists, but expansion covers more of the increase than replacement selling does.

Company B: MRR also rises, but new bookings are replacing a larger lost base. Discounts are heavier, service items are harder to separate, and collections lag behind billing terms.

The headline growth rate is identical, but the interpretation is not. The quality of MRR depends on retained revenue, expansion, exclusions, customer economics, and cash conversion, not only on the reported increase.

When MRR Can Mislead

MRR can mislead when the reported number is treated as a complete business-quality verdict. The metric is most vulnerable when the recurring base, exclusions, and movement components are unclear.

| Risk | How it misleads | Better investor check |

|---|---|---|

| Inflated active base | Customers counted as active may not represent durable paid demand. | Check paid activity, renewal status, pauses, and segment disclosure. |

| Inconsistent normalization | Annual or quarterly contracts may be converted differently across periods. | Check whether the company uses the same normalization method over time. |

| Non-recurring revenue included | Setup, consulting, or one-time charges can make recurring revenue look larger. | Separate recurring subscription revenue from services and one-time fees. |

| Churn masked by acquisition | New customers may replace lost customers without improving retention quality. | Compare gross retention, net retention, churn, and expansion components. |

| Weak cash conversion | Reported MRR may not translate into cash collection or free cash flow. | Compare MRR with billings, deferred revenue, operating cash flow, and margins. |

| Profitability ignored | Recurring revenue growth may require high sales, support, or infrastructure costs. | Check gross margin, sales efficiency, payback period, and operating leverage. |

Limitation: MRR is useful because it makes recurring revenue easier to compare. It is incomplete because it does not show the full cost of acquiring, serving, retaining, and expanding that recurring revenue.

FAQ

Is MRR the same as revenue?

No. MRR is a recurring revenue run-rate metric. Recognized revenue, billings, cash collections, and profit can all differ from MRR.

What should be excluded from MRR?

One-time setup fees, non-recurring services, free trials, unpaid users, and future pipeline should stay outside MRR unless the company clearly defines a recurring paid revenue basis.

Why can MRR growth be misleading?

MRR growth can be misleading when it includes non-recurring revenue, hides churn, depends on heavy discounts, or fails to convert into cash flow and margin quality.