Rolling puts means closing an existing put option and opening a replacement put option, usually with a different expiration, strike, or premium. The old contract stops controlling the open position after it is closed, but its economic result does not disappear. The replacement put creates a new exposure that needs its own assignment, exercise, payoff, liquidity, and volatility review.

Definition: A put roll is a two-part option adjustment: one put is closed, and another put is opened. The roll can change the timing, strike level, premium profile, and obligation boundary, but it is not a reset of the original trade economics.

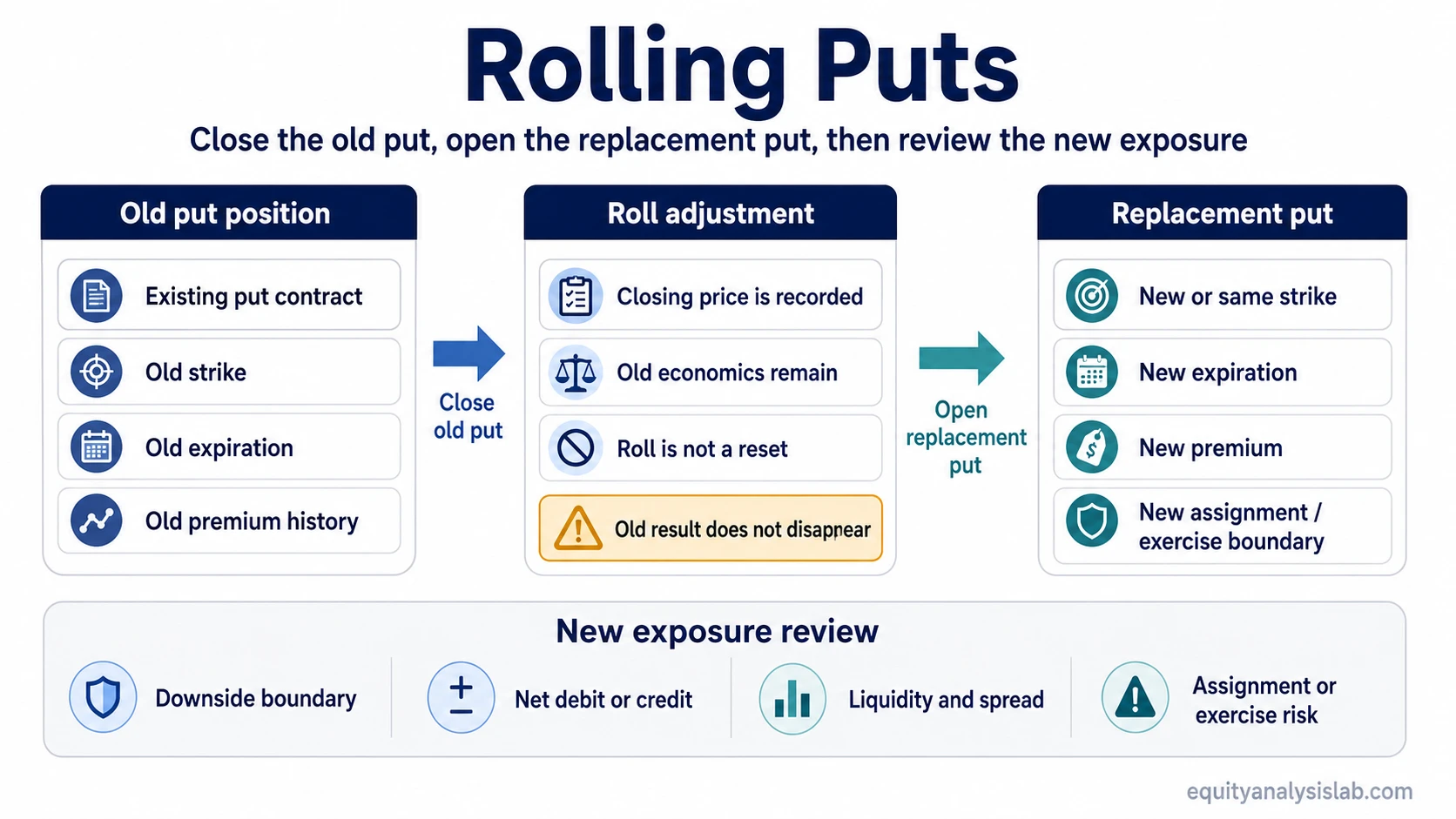

What Rolling Puts Means

Rolling puts is a position-management action, not a separate option type. The investor closes an existing put and replaces it with a new put contract. The replacement may keep the same strike, move to a lower strike, move to a higher strike, or use a later expiration depending on the structure of the roll.

For a short put, the roll usually means buying back the old short put and selling a replacement put. For a long put, the roll can mean selling or closing the old long put and buying a new long put. In both cases, the accounting of the old contract and the risk of the new contract should be separated.

The general close-and-open process is covered in rolling an option. Rolling puts is the put-specific version, where downside exposure, expiration timing, premium treatment, and assignment or exercise boundaries become the main issues.

What Changes When a Put Is Rolled

A put roll changes the open contract. It does not rewrite the history of the old contract. The new position may have a different strike, a different expiration date, a different premium, a different sensitivity to implied volatility, and a different assignment or exercise profile.

Key points:

- Strike: the replacement put may move the exposure boundary lower, higher, or keep it near the same level.

- Expiration: many rolls extend time, which can delay a decision but can also extend exposure.

- Premium: the closing price of the old put and the opening premium of the new put both matter.

- Assignment or exercise: the old contract’s boundary changes only after it is successfully closed, while the replacement contract creates its own boundary.

- Payoff and risk: the replacement put needs to be evaluated as a new open position, not as a continuation label.

Implied volatility also matters because the replacement put is priced under current option-market conditions. A roll opened during higher implied volatility may collect or cost a different premium than the old contract did, but that does not automatically make the replacement exposure safer.

Old Put vs Replacement Put

The cleanest way to read a put roll is to separate the contract being closed from the contract being opened. The old put contributes to the total economic result. The replacement put controls the open risk map after the roll.

| Element | Old put being closed | Replacement put being opened |

|---|---|---|

| Contract status | Closed, bought back, or sold out depending on whether the position was short or long | New open contract |

| Strike | Previous strike | New strike, same strike, lower strike, or higher strike depending on the roll |

| Expiration | Previous expiration | Later expiration in many rolls, though the replacement contract should be checked on its own terms |

| Premium | Old entry premium and closing cost remain part of the total result | New premium affects the new position economics |

| Assignment / exercise exposure | Ends once the old contract is successfully closed, assuming assignment has not already occurred | Begins under the replacement contract |

| Payoff/risk boundary | Old boundary no longer controls the open exposure after closure | New boundary must be reviewed |

| Main mistake | Treating closure as if the economics disappeared | Treating the new contract as automatically safer |

Premium, Debit, and Credit Treatment

A put roll can be opened for a net credit, a net debit, or roughly even money depending on the cost to close the old put and the premium received or paid for the replacement put. The net number describes the cash effect of the adjustment, not the full quality of the new exposure.

For a short put roll, a net credit means the replacement short put brings in more premium than the cost of closing the old short put. A net debit means the closing cost is larger than the new premium received. Neither label proves that the roll is good, safe, or complete. The replacement contract still has its own strike, expiration, assignment exposure, and downside boundary.

Important distinction: premium received from the replacement put changes the economics of the new structure, but it does not erase the closing cost, unrealized pressure, or realized result attached to the old put.

Assignment and Exercise Risk

Assignment risk matters most when rolling a short put or a cash-secured put. If the old short put is closed before assignment occurs, assignment exposure under that specific contract ends. Opening the replacement short put creates a new obligation boundary under the replacement contract.

Rolling can move the assignment boundary by changing strike or expiration, but it does not remove the obligation logic of a short put. If the replacement put is assigned, the account may still face the obligation tied to that new contract. The exact risk depends on contract terms, moneyness, expiration, and account structure.

For a deeper explanation of how a short option can become a contract obligation, review assignment risk.

Example of Rolling a Put

An investor has a short put with a 50 strike near expiration. The put was originally sold for 2.00, but it now costs 4.00 to close. The investor closes that old short put and opens a later-dated replacement short put with a 45 strike for 3.20.

The roll creates a 0.80 net debit for the adjustment because the closing cost is larger than the new premium received. The old 2.00 premium and the 4.00 closing cost remain part of the total history. The replacement 45-strike put is now the open exposure, with its own expiration, assignment boundary, premium, and downside risk.

The example does not show whether the roll is favorable. It only shows the mechanics: the old put is closed, the replacement put is opened, and the new contract must be reviewed as a new exposure.

When Rolling a Put Can Create a New Problem

Rolling can delay a problem without solving it. Extending expiration may give the position more time, but it can also keep downside exposure open for longer.

A lower strike is not automatically safer. Moving the strike lower can change the assignment boundary, but the account may still face loss if the underlying continues to move against the position.

A net credit can be misleading. More premium can reduce or reshape total economics, but it does not prove that the replacement contract has acceptable risk.

Liquidity and spreads matter. A replacement put with wider bid-ask spreads may be harder to adjust efficiently, especially when volatility is elevated.

Implied volatility can distort the premium comparison. A richer premium may partly reflect higher uncertainty, not a better position.

Rolling Puts vs Rolling an Option

Rolling an option describes the general close-and-open process across calls, puts, long positions, and short positions. Rolling puts is narrower because the replacement contract remains a put, so the analysis centers on downside exposure, put premium, strike selection, expiration timing, and assignment or exercise boundaries.

The same close/open mechanism can apply across calls and puts, but a put roll needs a separate review of downside exposure, premium history, replacement strike, expiration timing, and assignment or exercise risk. The old contract’s economics stay in the total result, while the replacement put controls the next open-position review.

Rolling Puts FAQ

Does rolling a put erase a loss?

No. Closing the old put records or preserves the economics of that contract. The replacement put creates a new exposure, but the old premium and closing cost remain part of the total result.

Is rolling a put always done for a credit?

No. A put roll can result in a net credit, a net debit, or a near-even adjustment depending on the closing cost of the old put and the premium of the replacement put.

Can rolling a short put remove assignment risk?

If the old short put is closed before assignment occurs, exposure under that specific contract ends. Opening a replacement short put creates a new assignment boundary, so assignment risk can change but is not automatically removed.