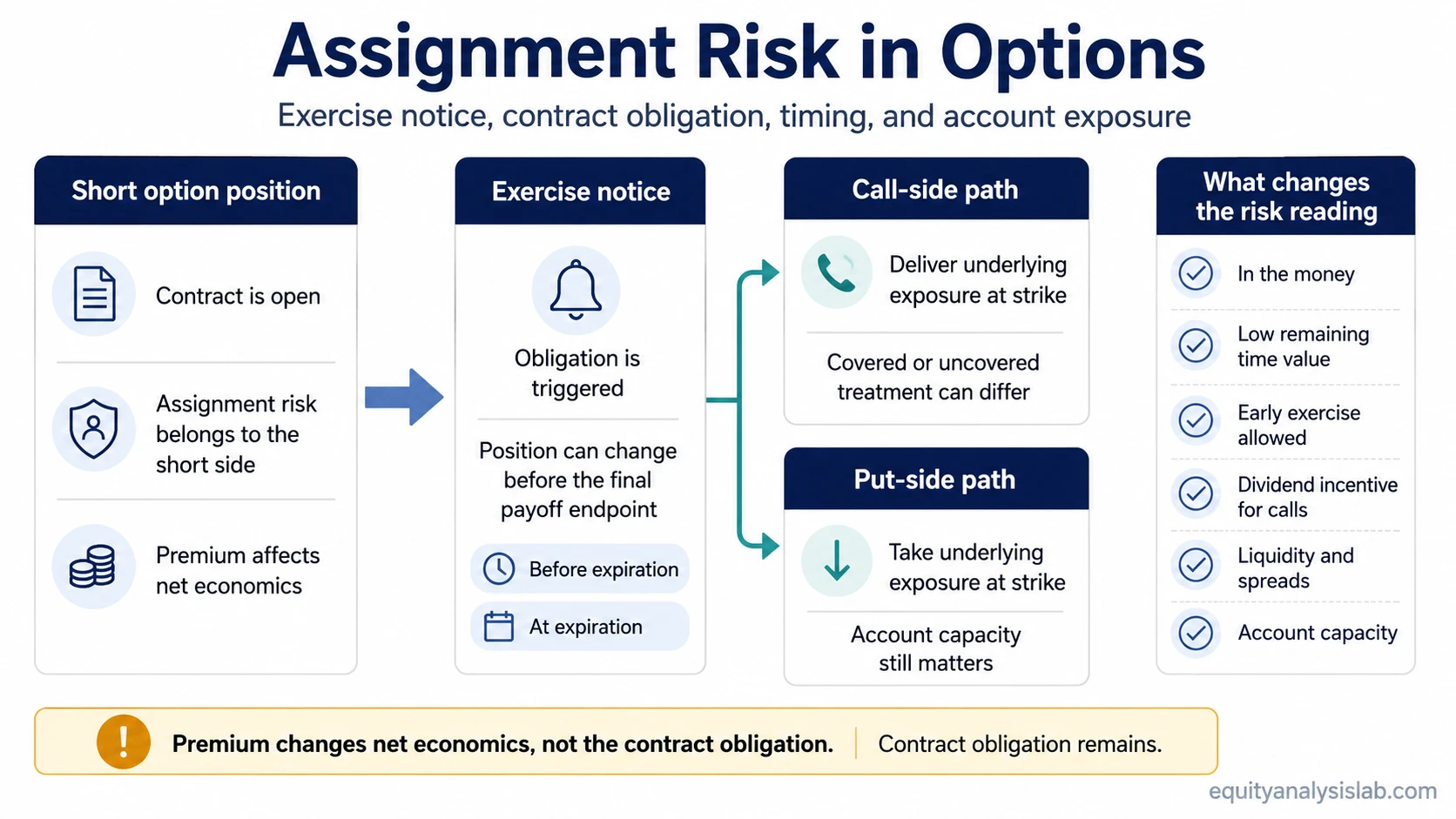

Assignment risk in options is the risk that a short option position receives an exercise notice and the seller must buy or sell the underlying before or at expiration, depending on the contract and exercise timing.

The risk belongs mainly to short option positions. A short call can create an obligation to sell the underlying at the strike price. A short put can create an obligation to buy the underlying at the strike price. The premium received changes the breakeven math, but it does not remove the contract obligation.

Definition: Assignment risk is the possibility that an option seller is assigned on a short contract and must fulfill the exercise terms, either before expiration when the contract allows early exercise or at expiration when the option finishes in an exercisable state.

Key Points

- Assignment risk is not the same as the expiration payoff line. Assignment can change the position before the final payoff diagram is reached.

- Short calls and short puts create different obligations: selling shares or delivering exposure for calls, buying shares or taking exposure for puts.

- Early assignment is most relevant for American-style options, because they can generally be exercised before expiration.

- Moneyness, remaining time value, dividends, liquidity, and account rules can all affect how assignment risk is interpreted.

- Premium received can reduce breakeven pressure, but it does not make assignment harmless or remove margin, liquidity, or account-exposure consequences.

How Assignment Changes the Position

An option payoff diagram usually shows the position at expiration. Assignment risk is different because the position may change before that endpoint. The option seller can move from holding an option position to holding, delivering, buying, or selling the underlying exposure, depending on the contract and account treatment.

A short call assignment usually means the seller must deliver or sell the underlying at the strike price. A short put assignment usually means the seller must buy the underlying at the strike price. The exact account result can depend on the option contract, whether the position is covered or uncovered, available buying power, and broker rules.

This is why assignment risk cannot be judged only from the option premium. The premium is part of the payoff calculation, but the obligation is part of the contract structure.

Early Assignment vs Expiration Assignment

Expiration assignment is tied to the option’s status near expiration. If a short option is in the money at expiration, assignment risk can become more direct because the option has exercisable value. That does not mean every contract outcome is identical across brokers, products, or accounts, but the short option seller must treat expiration as a point where assignment mechanics become more important.

Early assignment is the risk that the short option is assigned before expiration. This is mainly associated with American-style options, which can generally be exercised before expiration. European-style options are typically exercisable only at expiration, so the early-assignment path is different.

Early assignment often becomes easier to understand by separating intrinsic value from time value. When an option still has meaningful extrinsic value, exercising early can sacrifice that remaining time value. When extrinsic value is small, and another incentive exists, the early-exercise decision can become more attractive for the long option holder.

Assignment Risk Interpretation Table

Assignment risk is clearest when the option position is interpreted through conditions, not only through premium received or the final payoff shape.

| Condition | What it changes | Why premium or payoff alone can mislead |

|---|---|---|

| Short option moves in the money | The contract has exercisable intrinsic value. | The payoff line may show expiration math, but assignment can create the stock or cash obligation tied to the strike. |

| American-style option before expiration | Exercise may be possible before the final expiration date. | A simplified expiration chart can hide the path risk that occurs before expiration. |

| Little remaining extrinsic value | The long holder may sacrifice less time value by exercising. | Premium received by the seller does not show whether the long holder still has a reason to keep optionality alive. |

| Short call near an ex-dividend date | Dividend capture can increase the incentive to exercise in some cases. | The option seller may focus on breakeven while missing the dividend-related early-assignment incentive. |

| Short spread with one leg assigned | The account may temporarily hold a different exposure than the original spread shape. | The defined payoff diagram can look controlled while the live account exposure changes before the position is resolved. |

| Wide bid-ask spread or weak liquidity | Adjusting or closing the option may become more expensive or harder to execute cleanly. | Theoretical payoff can ignore the transaction cost and execution friction around assignment-sensitive positions. |

| Insufficient buying power or margin capacity | Assignment can create account constraints or forced account actions depending on broker rules. | Premium income does not remove the need to handle the resulting stock, cash, or margin exposure. |

Short Call and Short Put Assignment

Short call assignment and short put assignment are not interchangeable. A short call is linked to the obligation to sell the underlying at the strike price. If the seller does not already own the shares or required deliverable, assignment can create short stock exposure or another account-level obligation depending on the product and broker treatment.

A short put is linked to the obligation to buy the underlying at the strike price. If assigned, the seller may receive long stock or equivalent exposure and must have enough account capacity to support the position. The premium collected reduces the net breakeven, but the assigned position can still be large relative to the original option premium.

The practical risk is the size and timing of the obligation. A small option premium can sit in front of a much larger notional exposure if assignment occurs.

Why Dividends Can Affect Early Assignment Risk

Dividend risk is most relevant for short calls on dividend-paying stocks. Around the ex-dividend date, a call holder may compare the value of keeping the option open with the value of exercising and owning the shares before the dividend date. If the dividend incentive is larger than the remaining time value and other costs, early exercise can become more attractive.

This does not mean every short call near an ex-dividend date will be assigned. The risk depends on the option’s moneyness, remaining extrinsic value, dividend amount, borrow or financing considerations, liquidity, and contract terms.

The important boundary is that dividend-related assignment is an incentive problem, not a certainty rule. It becomes more relevant when the option is in the money and the remaining extrinsic value is low.

The Premium Received Does Not Erase the Obligation

Common mistake: Treating premium received as if it makes assignment risk disappear. Premium changes the net economics of the position, but the short option still carries an obligation if assigned.

For a short put, the collected premium lowers the net breakeven compared with the strike price. For a short call, the premium raises the effective sale level compared with the strike price. In both cases, the seller can still face the contract obligation, and the resulting exposure can be larger than the premium collected.

Premium also does not solve timing. Assignment can occur before the seller expected to deal with the underlying position, especially when early exercise is possible. That timing difference can matter when liquidity is poor, spreads are wide, or the account does not have enough capacity for the resulting exposure.

How Moneyness and Time Value Change the Risk

Moneyness describes where the underlying price sits relative to the strike. A short option that is out of the money usually has less immediate assignment pressure because exercising it would not normally create favorable intrinsic value for the holder. A short option that is in the money has intrinsic value, which can make assignment risk more relevant.

Time value adds another layer. A long option holder who exercises early may give up remaining extrinsic value. When that extrinsic value is still meaningful, selling the option may be more attractive than exercising it. When extrinsic value is small, the cost of exercising early can be lower.

The strongest assignment-risk reading usually combines both conditions: the option is in the money, and the remaining extrinsic value is limited. Other incentives, such as dividends on short calls, can then matter more.

Spread Assignment and Account Exposure

Assignment risk can feel misleading inside spreads because the expiration payoff may look defined. If one short leg is assigned before the long leg is exercised, closed, or otherwise handled, the account can temporarily carry exposure that differs from the neat spread diagram.

A spread may still have offsetting option rights, but those rights do not automatically eliminate every timing, liquidity, or account-treatment issue. The long leg may have value, but using it can involve execution decisions, exercise rules, bid-ask spreads, and broker-specific handling.

This is one reason assignment risk belongs in position management rather than only in payoff math. The risk is not only the final profit or loss line. It is also the path from option position to assigned exposure, and the account constraints that can appear along that path.

Practical Scenario

A short call is in the money before expiration, the stock has an upcoming ex-dividend date, and the option has very little remaining extrinsic value. The expiration payoff may still look understandable on a chart, but the short call seller can face early assignment if the long call holder has a strong reason to exercise. The premium received affects the net result, but it does not prevent the obligation to deliver or sell the underlying if assignment occurs.

The same logic can apply in a different form to short puts. If the put is in the money and assignment occurs, the seller may have to buy the underlying at the strike. The premium reduces the effective breakeven, but the account still must absorb the resulting exposure.

Where Assignment Risk Differs From Nearby Risks

Pin risk is narrower than assignment risk. Pin risk usually concerns uncertainty when the underlying price is close to the strike near expiration. Assignment risk is broader because it includes early exercise, moneyness, dividends, time value, spreads, and account obligation.

Rolling an option is one possible adjustment path, not a guarantee that assignment risk disappears. A roll can change strike, expiration, premium, and exposure, but the position still needs to be evaluated through the new contract terms and account risk.

Covered calls, cash-secured puts, and option spreads can each carry assignment risk in different ways. The structure changes the consequences, but it does not remove the need to understand who may exercise, when exercise can occur, and what obligation appears if assignment happens.

Assignment Risk Checklist

Assignment risk becomes easier to evaluate when the position is separated into contract mechanics, incentives, and account effects.

| Question | Why it matters |

|---|---|

| Is the short option in the money? | Intrinsic value can increase the relevance of exercise and assignment. |

| Is early exercise allowed? | American-style options can generally be exercised before expiration, while European-style options usually cannot. |

| How much extrinsic value remains? | Early exercise can become more attractive when little time value would be sacrificed. |

| Is there an ex-dividend date? | Short calls on dividend-paying stocks can face additional early-assignment incentive. |

| What happens if the short leg is assigned? | The account may receive long stock, short stock, cash requirements, or other exposure depending on the position. |

| Can the account support the resulting exposure? | Buying power, margin, and broker rules can shape the practical consequence of assignment. |

| How liquid is the option? | Wide bid-ask spreads can make adjustments more expensive and reduce flexibility. |

Limits of Assignment Risk Analysis

Limitation: Assignment risk can be evaluated, but it cannot be predicted with certainty from one variable. Moneyness, exercise style, time value, dividends, liquidity, and account rules interact.

No single condition guarantees assignment or prevents it. An in-the-money option can remain open. An option with low extrinsic value can still avoid early exercise. A dividend can increase the incentive to exercise a call, but the actual decision belongs to the option holder and depends on the full economics of the position.

The safest interpretation is conditional. Assignment risk tends to deserve more attention when a short option is in the money, early exercise is allowed, remaining extrinsic value is small, and the resulting account exposure would be difficult or costly to handle.

FAQ

What is assignment risk in options?

Assignment risk in options is the possibility that a short option seller receives an exercise notice and must fulfill the contract obligation, such as buying or selling the underlying at the strike price.

Can assignment happen before expiration?

Assignment can happen before expiration when the option is exercisable early, as with many American-style options. Early assignment is not guaranteed and depends on moneyness, remaining time value, dividends, and other incentives.

Does premium received remove assignment risk?

No. Premium received changes the net breakeven and payoff math, but it does not remove the short option obligation if assignment occurs.

Why do dividends matter for short call assignment?

Dividends can matter because a call holder may have an incentive to exercise before the ex-dividend date when the call is in the money and remaining extrinsic value is low.

Is assignment risk the same as pin risk?

No. Pin risk usually concerns uncertainty near a strike around expiration. Assignment risk is broader and can involve early exercise, dividends, time value, spreads, and account exposure.