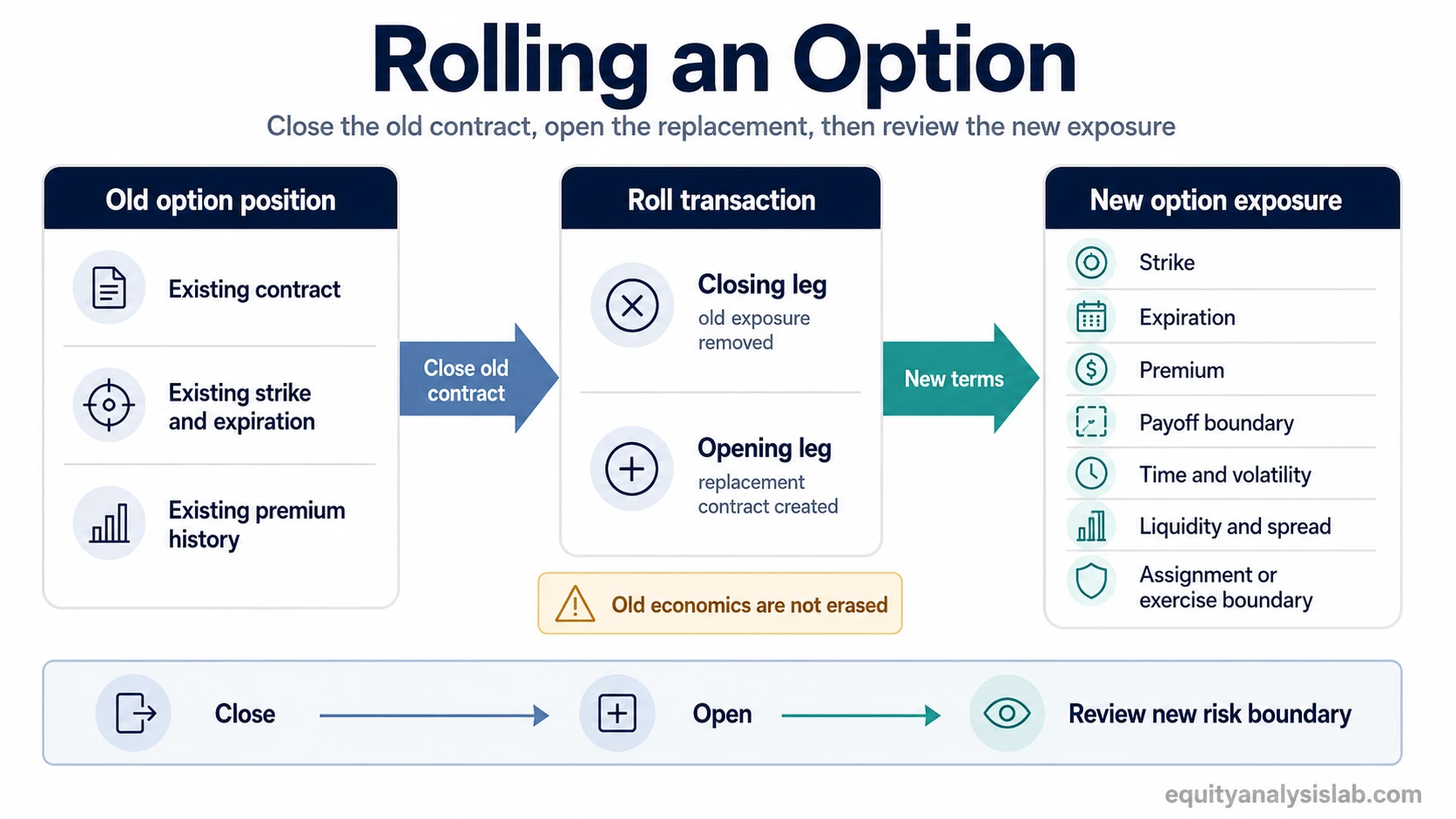

Rolling an option means closing an existing option position and opening another option position, usually with a different strike, expiration, or both. The roll changes future exposure, but it does not erase the economics of the position that was closed.

Definition: Rolling an option is a two-part position change: one option is closed, and another option is opened with new contract terms. A roll normally keeps the same underlying while changing the strike, expiration, premium paid or received, or another contract term that affects the next risk boundary.

A roll is often described as one action because both legs may be placed together as a combined order. Economically, however, it still contains two separate pieces: the closing value of the old option and the opening value of the new option.

That separation matters because the old leg already created a gain, loss, debit, credit, or obligation effect. The new leg creates a new payoff profile that must be evaluated on its own terms.

Key Points

- Rolling an option means closing one option position and opening another.

- The new option usually changes the strike, expiration, or both.

- The old position’s economic result is not erased by the new opening trade.

- A roll for a credit or debit does not describe the full outcome of the combined sequence.

- Assignment, exercise, implied volatility, time decay, liquidity, and spread costs can still affect the new exposure.

What rolling an option changes and what it does not change

A roll changes the contract terms that define the next stage of exposure. The most common changes are the strike price, expiration date, or both. Because options are contracts, those terms shape where payoff, obligation, and time sensitivity sit after the adjustment.

| Area | What may change | What does not automatically change |

|---|---|---|

| Strike | The replacement option may use a higher or lower strike than the old option. | A changed strike does not remove the need to evaluate the new payoff boundary and moneyness. |

| Expiration | The replacement option may move to a later expiration date. | More time does not guarantee a better result. It changes the exposure window and the time-value profile. |

| Premium | The roll may create a net credit or a net debit. | A credit does not prove profit, and a debit does not describe the full result. The old-leg economics still matter. |

| Payoff boundary | The new option creates a new payoff profile tied to its strike, expiration, and premium. | The prior gain or loss does not disappear just because the next contract has a different payoff shape. |

| Assignment / exercise exposure | Closing an old short option can remove that specific contract, while a new short option can create a new obligation boundary. | Rolling does not remove assignment or exercise exposure by definition. The new contract must be reviewed on its own terms. |

| Implied volatility exposure | The replacement option may have a different sensitivity to changes in implied volatility. | Observed premium can still change because of implied volatility even if the underlying price does not move much. |

| Liquidity / spread exposure | The new option may have a different bid-ask spread, depth, or execution quality than the old option. | Bid-ask spread and liquidity can still affect the real economics of the roll. |

Rolling up, rolling down, and rolling out

Roll descriptions usually refer to how the new contract differs from the old one. The terms are directional descriptions of contract terms, not proof that the adjustment is good or bad.

| Roll type | Basic meaning | Contract-term effect |

|---|---|---|

| Roll out | Move from a nearer expiration to a later expiration. | Extends the life of the exposure and changes the time-value component. |

| Roll up | Move to a higher strike. | Changes the strike boundary and the relationship between the option and the underlying price. |

| Roll down | Move to a lower strike. | Changes the strike boundary in the opposite direction. |

A roll can also combine direction and time, such as moving to a different strike and a later expiration. The label still describes contract terms only; it does not determine whether the roll improves the position, reduces risk, increases risk, or creates a better net result.

Close versus roll

Closing an option ends that option position. Rolling adds a second decision because a new option is opened after, or at the same time as, the closing transaction.

Close only: the old option position is closed, and no replacement option is opened.

Roll: the old option position is closed, and a replacement option is opened with its own strike, expiration, premium, and risk profile.

The difference is important because a roll can look like an exit while still leaving the account exposed to a new contract. The old exposure may be gone, but the new exposure has to be evaluated separately.

Premium, debit, credit, and net economics

Many rolls are described by whether they create a net credit or a net debit. That cash-flow label is useful, but it is incomplete.

| Roll cash flow | What it describes | What it does not prove |

|---|---|---|

| Net credit | The opening leg brings in more premium than the closing leg costs. | It does not prove the total sequence is profitable or that the new risk is small. |

| Net debit | The closing and opening sequence costs additional premium. | It does not by itself show whether the adjustment is sensible or whether the new exposure is acceptable. |

| Even or near-even roll | The closing and opening premiums are close to balanced. | It still changes the contract terms and future exposure. |

The full economics include the original entry price, the closing price of the old option, the opening price of the replacement option, commissions or fees where relevant, and the eventual result of the new position.

Common misunderstanding: a roll is not a reset

A roll can change the next contract, but it does not reset the full position history. The old option was closed at a real price. That closing transaction creates an economic result that remains part of the sequence.

The replacement option starts a new risk profile. That risk profile may have more time, a different strike, a different premium, and a different sensitivity to implied volatility. Those changes can help define the next exposure, but they do not erase what already happened.

How rolling affects assignment and exercise exposure

Assignment and exercise exposure depends on the contract type, position side, moneyness, expiration, and whether the option can be exercised early. Rolling can close one contract and open another, so the exposure must be checked at both points in the sequence.

For a short option, closing the old contract can remove that specific contract’s assignment risk. Opening a new short option can create a new assignment boundary tied to the replacement contract.

Near expiration, contract behavior can also be affected by how close the underlying price is to the strike. That is why pin risk is best treated as a related but separate concept rather than the main definition of rolling.

Practical example of a roll sequence

Suppose an investor has an open option position that is near expiration. Instead of simply closing the position and leaving no replacement exposure, the investor closes the old option and opens a later-expiring option on the same underlying.

The adjustment changes the expiration date and may change the strike or premium. The first transaction still locks in the closing value of the old option. The second transaction creates a new option position with its own time value, volatility exposure, liquidity conditions, and assignment or exercise considerations.

The useful point is not whether the roll is favorable. The useful point is that the roll is a sequence: old contract closed, replacement contract opened, new exposure reviewed.

What to review after rolling an option

After a roll, the replacement option should be treated as a new contract exposure. The old position history still matters for total economics, but the new contract has its own risk boundaries.

| Review area | Question to ask |

|---|---|

| Strike | Where is the new strike relative to the underlying price? |

| Expiration | How much time has been added or changed? |

| Premium | Was the roll a net debit, net credit, or near-even adjustment? |

| Old-leg result | What economic result was created when the original option was closed? |

| New payoff boundary | What does the replacement contract require for a favorable or unfavorable result? |

| Time decay | How does the new expiration affect time-value sensitivity? |

| Implied volatility | How could changes in implied volatility affect the replacement option’s theoretical value and observed premium? |

| Liquidity | Are bid-ask spreads, depth, and execution conditions different in the replacement contract? |

| Assignment or exercise | Does the new contract create a new obligation or exercise boundary? |

Rolling is a position-management action, not a trade signal

Rolling an option describes a contract adjustment. It does not say whether the position should be opened, closed, extended, reduced, or avoided. The same roll label can describe very different risk profiles depending on the option type, position side, strike, expiration, premium, volatility, and account context.

For that reason, the roll should be read as a mechanics term first. It explains what changed in the contracts. It does not prove that risk was reduced, that income was earned, or that the next outcome is more likely to be favorable.

Rolling an Option FAQ

What does it mean to roll an option?

Rolling an option means closing an existing option position and opening another option position, usually with a different strike, expiration, or both.

Is rolling an option the same as closing it?

No. Closing ends the existing option position. Rolling closes the existing option and opens a replacement option, so new exposure remains.

Does rolling an option remove assignment risk?

Closing a short option can remove that specific contract’s assignment exposure, but opening a new short option can create a new assignment boundary.

Can rolling for a credit still lose money?

Yes. A credit describes the cash flow on the roll, not the full economic result of the old leg, the new leg, and the final position outcome.