Valuation multiples compare what investors are paying for a company with a financial or operating base such as earnings, sales, book value, free cash flow, EBITDA, or growth. The ratio is simple, but the reading changes with the numerator, denominator, peer group, and quality of the business measure being used.

A multiple is most useful when it compares like with like. Equity value should be matched with equity-level measures, enterprise value should be matched with business-wide operating measures, and peer comparisons should account for margins, growth, leverage, accounting, cyclicality, and capital intensity.

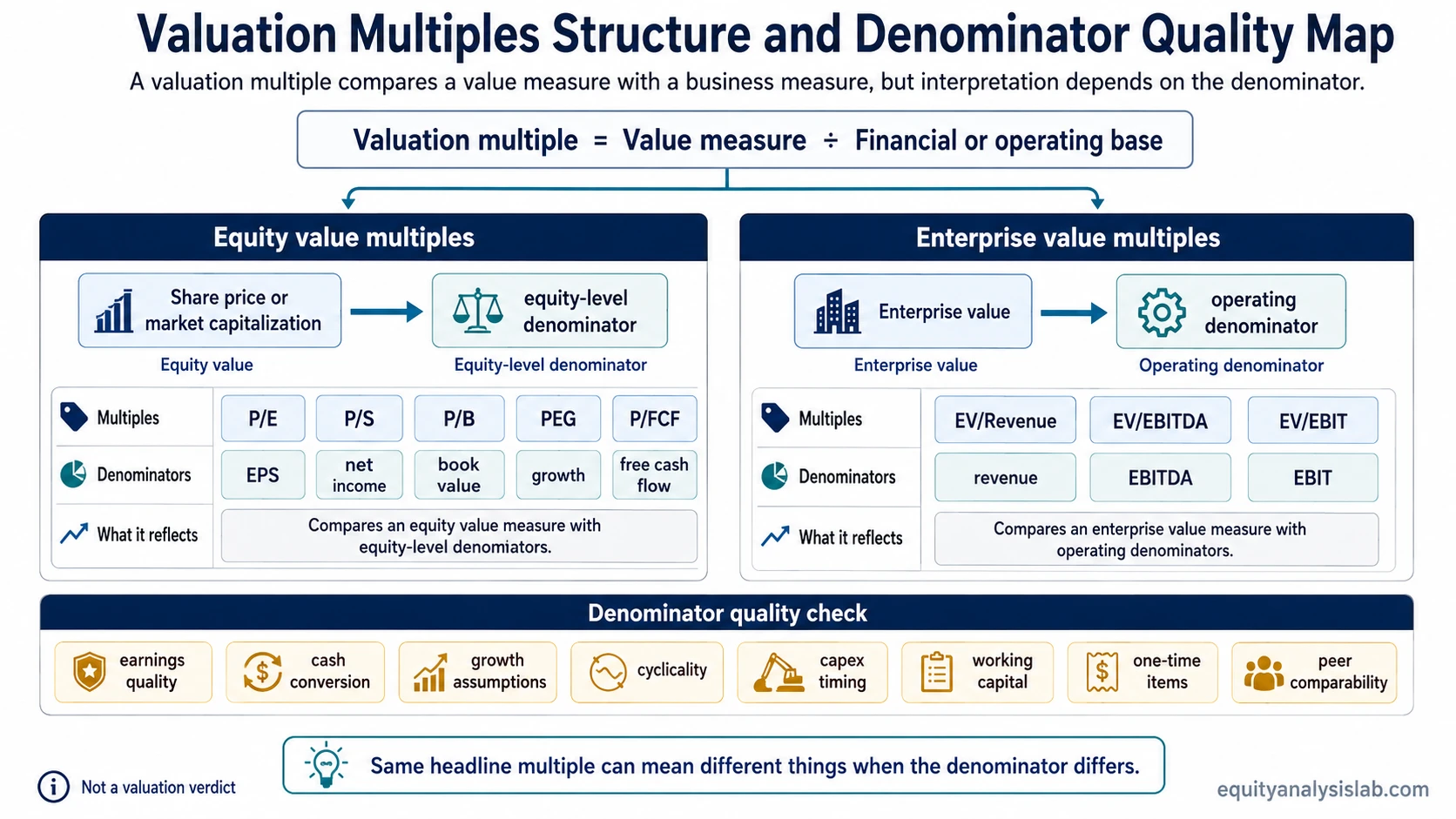

Definition: A valuation multiple is a ratio that compares a company value measure with a financial or operating measure. Common examples include market capitalization divided by net income, enterprise value divided by EBITDA, or share price divided by free cash flow per share.

They are comparison tools, not standalone proof that a company is cheap, expensive, or fairly valued.

Key Points About Valuation Multiples

- Valuation multiples compare a value measure with a business measure.

- Equity multiples and enterprise value multiples answer different questions.

- The denominator often controls the reading more than the headline ratio suggests.

- Peer comparability matters because different businesses can deserve different multiples.

- A low multiple is not automatically cheap, and a high multiple is not automatically expensive.

- Dedicated ratio pages are better places for full formula detail and deeper interpretation.

What Are Valuation Multiples?

Valuation multiples are comparison ratios used in equity analysis and relative valuation. They connect a company’s market value or enterprise value to a base such as earnings, revenue, book value, EBITDA, free cash flow, or expected growth.

The basic structure is:

Valuation multiple = value measure ÷ financial or operating base

The numerator shows what the market is assigning to the company. The denominator shows the business measure used to interpret that value. A multiple compresses comparison into one number, so the number needs context before it has much meaning.

How Valuation Multiples Work

A valuation multiple asks how much value is being assigned for one unit of a business measure. A company trading at 20 times earnings is being valued at 20 units of price or equity value for each unit of earnings. A company trading at 10 times EBITDA is being valued at 10 units of enterprise value for each unit of EBITDA.

The first distinction is the value claim. Equity value belongs to common shareholders after considering debt and other claims. Enterprise value represents the value of the operating business before separating the claims of debt and equity holders.

| Question | Numerator type | Denominator type | Why the match matters |

|---|---|---|---|

| What are equity holders paying? | Share price or market capitalization | Equity-level measures such as EPS, net income, book value, or free cash flow to equity | The numerator and denominator both relate to common equity holders. |

| What is the operating business worth? | Enterprise value | Operating measures such as revenue, EBITDA, or EBIT | The numerator captures debt and equity claims, so the denominator should represent the business before financing structure. |

The like-for-like rule is central. Enterprise value should not be casually divided by net income, and market capitalization should not be compared with EBITDA without recognizing the mismatch. Cleaner numerator-denominator matching makes the comparison more useful.

Main Types of Valuation Multiples

Most valuation multiples fall into two broad families: equity multiples and enterprise value multiples. Equity multiples focus on what shareholders are paying. Enterprise value multiples focus on the value assigned to the operating business before financing claims are separated.

| Multiple family | Common examples | Typical use | Main caution |

|---|---|---|---|

| Equity earnings multiples | Price-to-earnings ratio | Comparing share price or market capitalization with earnings available to equity holders | EPS may be distorted by one-time items, cyclicality, tax effects, buybacks, or accounting choices. |

| Equity revenue multiples | Price-to-sales ratio | Comparing equity value with revenue when earnings are low, volatile, or negative | Revenue does not show margins, cash conversion, dilution, or capital intensity by itself. |

| Equity asset multiples | Price-to-book ratio | Comparing equity value with book value, often for asset-heavy or financial businesses | Book value may be less useful for asset-light companies or firms with large intangible value. |

| Equity growth-adjusted multiples | PEG ratio | Comparing a P/E ratio with an expected earnings growth rate | The result is sensitive to growth assumptions and the earnings base used. |

| Equity cash flow multiples | Price to free cash flow | Comparing equity value with cash generated after capital expenditures | Free cash flow may move with working capital timing, capex cycles, and normalization choices. |

| Enterprise value operating multiples | EV/EBITDA, EV/EBIT, and related enterprise value operating multiples | Comparing business value with operating earnings before or after selected non-cash charges | EBITDA does not directly capture capital expenditures, working capital, taxes, or debt service. |

Valuation Multiple Route Map

Different multiples answer different valuation questions. The useful starting point is not which multiple is “best,” but which value claim and denominator fit the business question being asked.

| Valuation question | Multiple family | Numerator | Denominator | Main interpretation risk | Deeper page |

|---|---|---|---|---|---|

| How much are shareholders paying for earnings? | Equity earnings multiple | Share price or market capitalization | EPS or net income | Earnings quality, cyclicality, one-time items, buyback effects, and negative EPS can distort the reading. | price-to-earnings ratio |

| How much is the operating business valued against EBITDA? | Enterprise value operating multiple | Enterprise value | EBITDA | Capital expenditures, working capital, taxes, and leverage may make EBITDA cleaner than cash economics. | EV/EBITDA |

| How much value is assigned to each unit of sales? | Revenue multiple | Market capitalization or enterprise value | Revenue | Margins, cash conversion, growth quality, and dilution may vary sharply across companies with similar sales. | price-to-sales ratio or EV/Revenue |

| How much are shareholders paying relative to accounting equity? | Book value multiple | Share price or market capitalization | Book value per share or common equity | Book value relevance depends on asset quality, accounting treatment, and the business model. | price-to-book ratio |

| How does the earnings multiple compare with expected growth? | Growth-adjusted multiple | P/E ratio | EPS growth rate | Growth estimates may be fragile, inconsistent, or disconnected from cash-flow quality. | PEG ratio |

| How much are shareholders paying for free cash flow? | Cash flow multiple | Share price or market capitalization | Free cash flow or free cash flow per share | Working capital timing, capex cycles, and normalization choices may change the denominator materially. | price to free cash flow |

Why the Denominator Matters

The denominator is often where the ratio changes meaning. Two companies may share the same headline multiple while relying on business measures with different quality, durability, or comparability.

Earnings: EPS anchors valuation better when earnings are durable, cash-flow supported, and not overly shaped by one-time gains, tax effects, accounting choices, buybacks, or unusual margins.

EBITDA: EBITDA helps operating comparisons, but it leaves out capital expenditure needs, working capital, taxes, interest, and debt service. A capital-light business and a capital-intensive business may appear similar on EV/EBITDA while producing different cash economics.

Revenue: Sales are useful when earnings are temporarily weak or negative, but revenue quality still depends on margins, retention, pricing power, dilution, and the cost of growth.

Book value: Book value tends to matter more for asset-heavy or financial businesses than for asset-light firms where brand, software, network effects, or internally developed intangibles may not be reflected cleanly on the balance sheet.

Free cash flow: Cash flow before narrative is a useful discipline, but free cash flow still moves with working capital timing, investment cycles, or one-off capital spending. A single-year denominator may not represent normalized economics.

Growth: Growth-adjusted multiples depend on an assumption rather than a reported number. The reading weakens when the growth estimate is aggressive, short-lived, or unsupported by margins and cash conversion.

How Investors Use Valuation Multiples

Investors commonly use valuation multiples to compare companies, screen for candidates, sanity-check assumptions, and understand what the market may be implying about growth, margins, risk, or earnings durability.

- Peer comparison: Multiples help compare companies in the same industry when the peer group has similar business models, margins, growth, leverage, and accounting treatment.

- Historical comparison: A company’s current multiple can be compared with its own past range, but the business quality and market environment may have changed.

- Screening: Multiples help narrow a research list, but screening is only a starting point.

- Assumption checks: A multiple can test whether a valuation view is consistent with margins, growth, cash flow, and risk.

- Cross-checking: Multiple families can be compared with each other to see whether earnings, revenue, cash flow, and balance-sheet measures tell a consistent story.

A single multiple should not carry the full valuation decision. The stronger use is comparison plus diagnosis: what is the market paying for, what denominator is being used, and what might distort that denominator?

Common Mistakes When Reading Valuation Multiples

- Treating a low multiple as automatically cheap: A low multiple may reflect weak growth, high leverage, poor earnings quality, cyclicality, litigation risk, or a deteriorating business model.

- Treating a high multiple as automatically expensive: A high multiple may reflect stronger margins, better growth durability, higher returns on capital, lower capital intensity, or lower balance-sheet risk.

- Mixing enterprise value with equity-only denominators: Enterprise value should generally be paired with operating measures such as revenue, EBITDA, or EBIT, not equity-only measures such as EPS.

- Using weak peer groups: Companies in the same sector can still have different margins, growth rates, leverage, accounting policies, customer concentration, and reinvestment needs.

- Relying on a one-year denominator: A single year of EPS, EBITDA, revenue growth, or free cash flow may be distorted by cycles, one-time items, or temporary working capital moves.

- Ignoring negative or unusually low denominators: Negative earnings or unusually low cash flow may leave a multiple meaningless, unstable, or difficult to compare.

A Simple Valuation Multiple Example

Consider two companies that both trade at 15 times earnings. The headline multiple is the same, but the reading may diverge.

| Company | Headline multiple | Denominator quality | Interpretation issue |

|---|---|---|---|

| Company A | 15x earnings | Earnings are recurring, cash-flow supported, and produced with stable margins. | The multiple is easier to compare if peers have similar growth, margins, and reinvestment needs. |

| Company B | 15x earnings | Earnings include a temporary gain and margins are near a cyclical high. | The same multiple may overstate comparability if the denominator is not normalized. |

The example does not show which company is worth owning. It shows why the same multiple may carry different meaning when the denominator differs in durability, cash conversion, cyclicality, or accounting quality.

When Valuation Multiples Are Most Useful

Valuation multiples are most useful when they organize comparison rather than replace analysis. They work best when the business model, accounting base, capital structure, margin profile, growth outlook, and cash conversion are reasonably comparable.

- Comparing companies with similar economics inside the same industry.

- Checking whether a valuation assumption is broadly consistent with peer context.

- Identifying when a company deserves deeper research because its multiple looks unusual.

- Understanding whether the market is assigning more value to growth, profitability, cash flow, or balance-sheet strength.

- Cross-checking one valuation method against another without treating any single ratio as final.

Where Valuation Multiples Can Mislead

Valuation multiples mislead when the ratio looks clean but the comparison base is weak. The most common problem is not the formula itself, but the assumption that two denominators mean the same thing.

- Accounting differences: Revenue recognition, depreciation policies, capitalization choices, and one-time items may change the denominator.

- Cyclicality: Earnings, EBITDA, margins, and cash flow may peak near cyclical highs and compress near troughs.

- Capital structure: Equity multiples and enterprise value multiples may tell different stories when leverage, cash, or debt cost differs across companies.

- Market sentiment: Multiples may expand or contract because investors change risk appetite, not only because the company changes.

- Negative earnings: A negative or near-zero denominator often leaves common multiples unusable or unstable.

- One-time items: A temporary gain, charge, tax effect, or working capital movement may distort the year used in the ratio.

- Peer mismatch: A company may belong to the same industry but have different margins, growth, capital needs, or competitive position.

- Growth assumptions: Growth-adjusted comparisons depend on forecasts that may change quickly.

- Capital intensity: EBITDA and revenue multiples may miss the difference between businesses that need heavy reinvestment and businesses that convert more revenue into cash.

Which Valuation Multiple Should You Read Next?

The next useful step depends on the denominator you are trying to understand. Earnings-based comparisons usually start with P/E. Operating-business comparisons often move toward EV/EBITDA. Revenue, book value, cash flow, and growth-adjusted ratios answer different questions and need their own denominator checks.

| Reader question | Best next topic | Why it fits |

|---|---|---|

| I want to compare share price with earnings. | Price-to-earnings ratio | Focuses on how much investors pay for each unit of EPS or net income. |

| I want to compare operating value before financing effects. | EV/EBITDA | Uses enterprise value and an operating earnings denominator. |

| I want to analyze companies where earnings are weak or negative. | Price-to-sales ratio | Uses revenue as the base, while still requiring margin and cash-flow checks. |

| I want to compare value with balance-sheet equity. | Price-to-book ratio | Often fits better when accounting equity and asset values matter. |

| I want to compare earnings multiples with expected growth. | PEG ratio | Adds a growth denominator, making assumptions more visible. |

| I want to focus on cash generation after reinvestment. | Price to free cash flow | Moves the comparison toward cash economics, while still requiring normalization. |

Valuation Multiples FAQ

What is a valuation multiple?

A valuation multiple is a ratio that compares a company value measure with a financial or operating measure, such as earnings, sales, book value, EBITDA, free cash flow, or growth.

Are lower valuation multiples always better?

No. A lower multiple can reflect weaker growth, lower earnings quality, higher leverage, cyclicality, or business risk. The denominator and peer group need to be checked before interpreting the ratio.

What is the difference between equity multiples and enterprise value multiples?

Equity multiples use share price or market capitalization and usually compare value with equity-level measures. Enterprise value multiples use enterprise value and usually compare the operating business with revenue, EBITDA, or EBIT.

Why can two companies with the same multiple have different valuations?

The same headline multiple can hide differences in margins, growth durability, cash conversion, leverage, accounting quality, cyclicality, and one-time items. Those differences can change how the ratio should be interpreted.