There is no single correct number of stocks to own. A portfolio with 10 stocks can be diversified or concentrated, and a portfolio with 40 stocks can still carry overlapping exposure. The number only becomes useful after weights, overlap, concentration, review capacity, and risk capacity are visible.

- Stock count is a starting input, not a diversification score.

- Position weights can matter more than the number of holdings.

- Overlap can make many holdings behave like fewer independent bets.

- Review capacity matters because individual stocks require ongoing review.

- More stocks can reduce single-company risk, but they do not remove market risk or guarantee better results.

How many stocks should you own?

A useful answer is not a fixed number. The better question is whether the number of stocks creates exposure that can be understood, monitored, and held through the investor’s time horizon and risk capacity.

A smaller portfolio can make sense when each position is researched, sized deliberately, and not overly dependent on one sector, factor, or thesis. A larger portfolio can make sense when the investor wants less single-company dependence and has a clear process for avoiding overlap, drift, and forgotten positions.

The question becomes misleading when the headline number is treated as the whole answer. Twenty holdings do not automatically create a diversified portfolio. Forty holdings do not automatically make decision quality better. The holdings list has to be interpreted through what each position contributes to total exposure.

Why stock count is really an exposure question

Each stock adds more than another ticker symbol. It adds business exposure, sector exposure, factor exposure, valuation exposure, currency or geographic exposure in some cases, and thesis exposure. The same stock count can therefore create very different risk profiles.

A portfolio can hold many companies but still depend heavily on one economic driver. For example, several software, semiconductor, and digital advertising companies may look different by name, but they can still share sensitivity to growth expectations, interest rates, and valuation multiples. The headline number rises, but independent exposure may not rise by the same amount.

That is why diversification is not just the act of adding names. It depends on how independent the exposures are, how large each position is, and how the portfolio behaves when one theme weakens.

What changes the right number of stocks

The right number changes when the portfolio’s structure changes. A concentrated portfolio with equal weights is different from a concentrated portfolio where two holdings dominate. A broad portfolio with genuinely different business drivers is different from a broad portfolio that repeats the same thesis many times.

| Portfolio condition | What the stock count seems to imply | What the investor must check | Limitation |

|---|---|---|---|

| Few holdings with balanced weights | The portfolio may look concentrated. | Whether the companies have different drivers, sectors, and thesis risks. | A low count can still be manageable if exposures are deliberate, but single-company risk remains higher. |

| Few holdings with one or two dominant weights | The portfolio may look focused. | Top position weight, top 3 weight, and dependence on one thesis. | Focus can become fragility when one position controls the portfolio outcome. |

| Many holdings with similar business drivers | The portfolio may look diversified. | Sector, factor, valuation, revenue-driver, and thesis overlap. | More names may not reduce exposure if the holdings respond to the same conditions. |

| Many holdings with small forgotten positions | The portfolio may look safer because it has more names. | Review capacity, thesis clarity, and whether each holding still has a role. | A larger count can weaken decision quality if positions are no longer monitored. |

| Individual stocks plus funds or ETFs | The direct stock count may look modest. | Overlap between individual stocks and fund holdings, if applicable. | Fund exposure can duplicate stock exposure even when the individual stock count looks controlled. |

When more holdings do not mean better diversification

False diversification happens when the portfolio has more names but not more independent exposure. The most common causes are oversized top positions, repeated sector exposure, repeated factor exposure, and multiple companies tied to the same investment thesis.

A portfolio with 25 stocks can still be exposed mainly to one theme if most of the weight sits in similar businesses. A portfolio with 15 stocks can have broader exposure if the holdings are sized carefully and tied to different economic drivers. The headline total matters, but it does not explain the whole portfolio.

Common mistake: Adding another stock only because the portfolio count looks low can create a weaker portfolio if the new holding repeats the same exposure, has a lower-quality thesis, or receives too little attention after purchase.

The opposite mistake is treating every concentrated portfolio as automatically better because it looks focused. Concentration becomes more defensible only when position size, thesis quality, downside tolerance, and review discipline are clear.

A simple count-to-exposure check

A stock count becomes more useful when it is paired with a short exposure checklist. The goal is not to find a perfect number. The goal is to see whether the number of holdings matches the portfolio’s actual risk structure.

Use the checklist as a diagnostic, not as a target-number formula.

- Holdings count: How many individual stocks are owned?

- Position weights: Is each holding sized deliberately, or did weights drift?

- Top 3 and top 5 concentration: How much of the portfolio depends on the largest holdings?

- Sector overlap: Are many holdings exposed to the same industry or economic cycle?

- Factor overlap: Are holdings repeatedly sensitive to the same growth, value, quality, size, rate, or momentum exposure?

- Thesis overlap: Are several positions built on the same underlying idea?

- Rebalancing rule: What prevents one winner, loser, or theme from becoming too large?

- Review capacity: Can each company still be followed with enough attention?

- Time horizon: Does the portfolio structure match the intended holding period?

- Risk capacity boundary: Can the investor tolerate the portfolio’s downside without being forced into poor decisions?

- Fund or ETF overlap: Do any funds already own the same companies or exposures?

Asset allocation sits above this stock-count decision because it controls the broader mix of stocks, bonds, cash, and other assets. The number of stocks only explains one part of the equity sleeve.

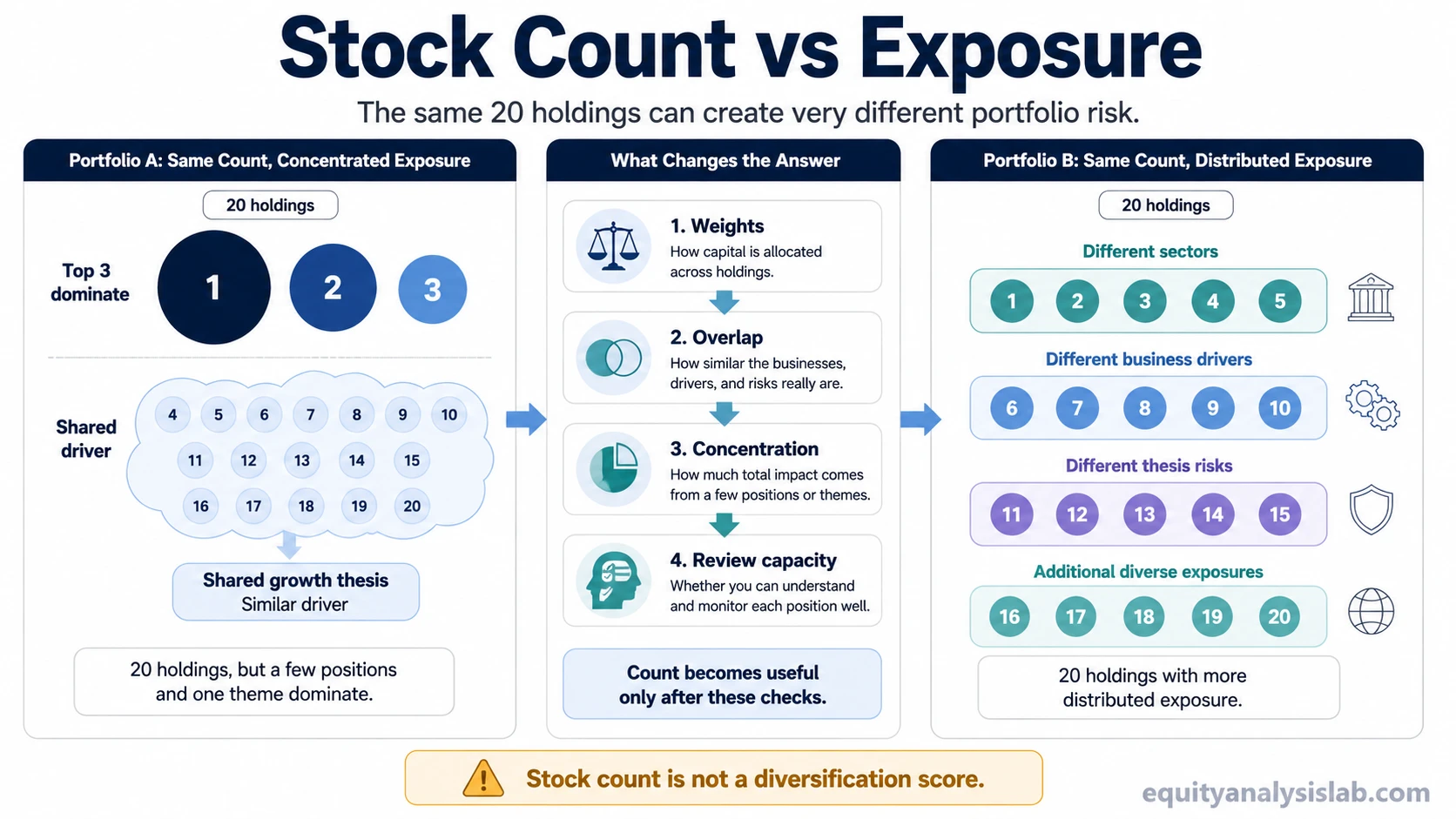

Example: same count, different exposure

Consider two illustrative portfolios with 20 individual stocks each.

Portfolio A: The top 3 holdings make up 60 percent of the portfolio, and most other holdings are tied to the same growth-oriented thesis. The portfolio has 20 names, but the outcome still depends heavily on a few companies and one broad idea.

Portfolio B: The 20 holdings are closer to equal weight, with different business models, sectors, and thesis drivers. The same count creates a more distributed exposure profile, although market risk and company-specific risk still remain.

The number is identical. The exposure is not. That is why holdings count only becomes meaningful after weights, overlap, and concentration are checked.

Common mistakes when choosing a stock count

| Mistake | Why it creates risk | Better diagnostic question |

|---|---|---|

| Choosing a number because it appears common | A common range may not fit the portfolio’s weights, overlap, or review capacity. | What exposure does the count actually create? |

| Adding stocks to feel diversified | New holdings can repeat the same sector, factor, or thesis exposure. | Does the new holding reduce dependence on an existing driver? |

| Keeping tiny positions without a role | Small positions can create clutter without improving portfolio behavior. | Would the portfolio lose anything important if the position were removed? |

| Ignoring drift after price movement | A balanced portfolio can become concentrated when winners or losers change position weights. | What rule keeps position weights from drifting beyond the intended range? |

| Confusing review capacity with confidence | A larger portfolio requires more monitoring, not less. | Can every holding still be reviewed with enough depth? |

Limits of any stock-count answer

More stocks can reduce dependence on one company, but they do not guarantee better returns, lower total risk, or better decisions. Diversification does not remove market risk. A larger portfolio can still fall when the equity market falls, when a dominant sector weakens, or when many holdings share the same risk factor.

A smaller portfolio can also be more fragile than it looks if the largest positions are too important to the outcome. The useful boundary is not whether the count looks high or low. The useful boundary is whether the portfolio’s actual exposure can be understood before stress appears.

Review capacity is part of that boundary. A portfolio with more individual companies requires more earnings reviews, business-model checks, balance-sheet updates, valuation reassessments, and thesis maintenance. When the number becomes too large to monitor, the portfolio may become diversified on paper but unmanaged in practice.

Related portfolio concepts

Diversification: Useful for understanding whether different holdings actually reduce dependence on one company, sector, or thesis.

Concentration: Useful for judging whether a few holdings or one theme controls too much of the portfolio outcome.

Asset allocation: Useful for separating the stock-count question from the broader mix between equities, fixed income, cash, and other asset classes.

FAQ

Is 20 stocks enough for a portfolio?

Twenty stocks can be enough in some portfolios and too concentrated in others. The answer depends on position weights, overlap, top-holding concentration, review capacity, time horizon, and risk capacity.

Can you own too many stocks?

Yes. Too many stocks can create monitoring problems, repeated exposure, and small positions that no longer affect the portfolio meaningfully. A larger count is only useful when it improves exposure quality or reduces avoidable single-company dependence.

Does owning more stocks always reduce risk?

No. More stocks can reduce single-company risk, but they do not remove market risk, sector risk, factor risk, or thesis overlap. A portfolio can hold many names and still depend on the same underlying driver.