Quick ratio is a liquidity ratio that compares a company’s most liquid current assets with its current liabilities. It is also called the acid-test ratio. The ratio helps investors check near-term liquid coverage, but it does not prove business quality, debt safety, valuation attractiveness, or future stock returns.

Definition: Quick ratio measures whether a company has enough liquid current assets to cover current liabilities without relying on inventory or prepaid expenses.

Key Points

- Quick ratio compares liquid current assets with current liabilities.

- It usually includes cash, marketable securities, and accounts receivable.

- It usually excludes inventory and prepaid expenses because they may not convert into cash quickly.

- A higher quick ratio is not automatically better without peer, trend, receivable quality, and cash-conversion context.

- Quick ratio is a liquidity diagnostic, not a standalone verdict on company quality or stock attractiveness.

What the Quick Ratio Measures

The ratio measures near-term liquid coverage. It asks whether a company could cover current liabilities using assets that are already cash-like or expected to convert into cash relatively quickly.

The ratio is stricter than a broad current-asset check because it normally removes inventory and prepaid expenses. Inventory may require time, discounts, or customer demand before it becomes cash. Prepaid expenses may reduce future costs, but they are not usually available to pay suppliers, lenders, employees, or tax obligations.

For investors, quick ratio is most useful as a pressure test on the balance sheet. It can highlight whether reported current assets are liquid enough to support near-term obligations, but it still needs to be compared with cash generation, liability timing, business model, and industry norms.

Quick Ratio Formula

The common quick ratio formula is:

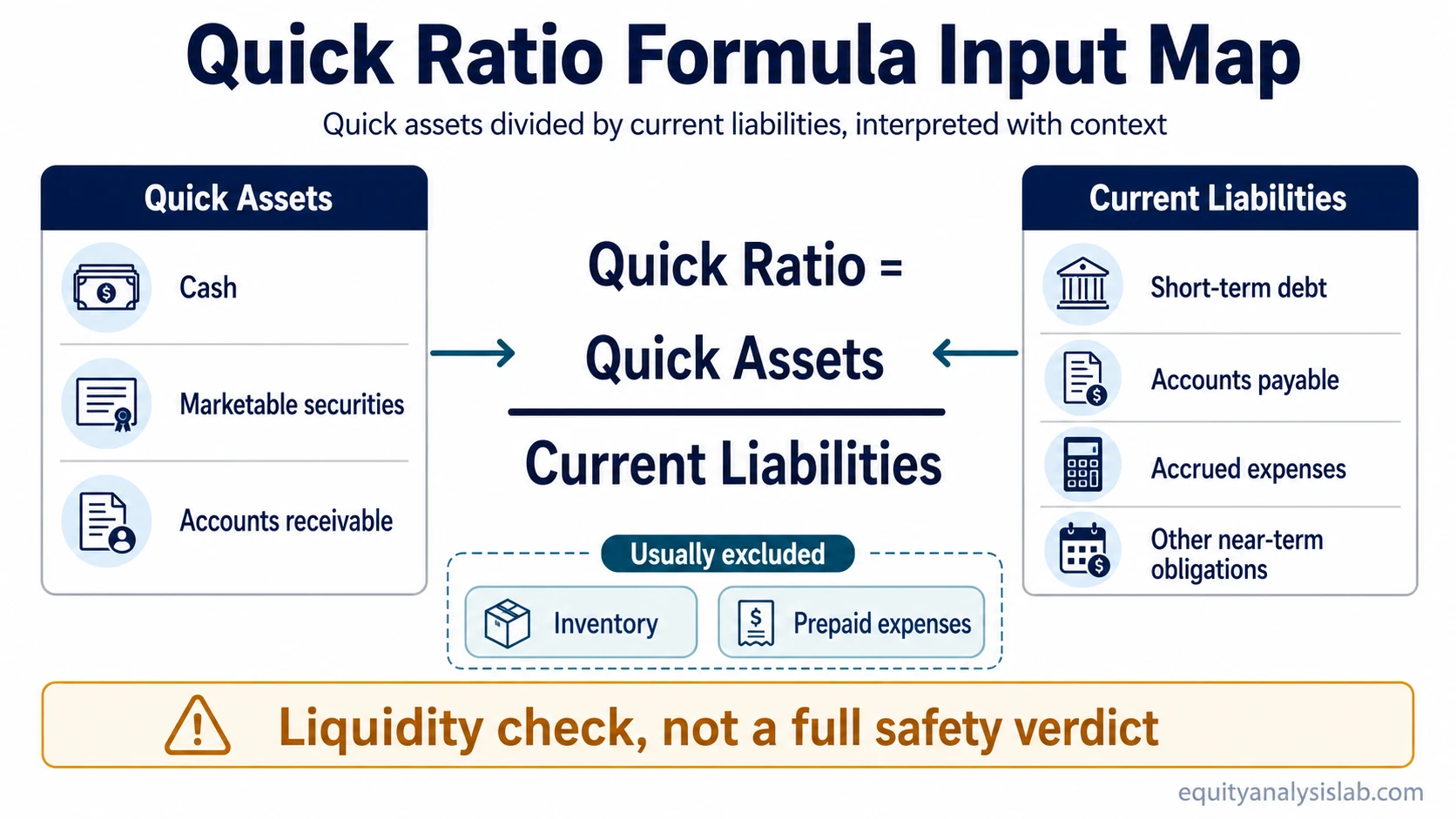

Quick Ratio = (Cash + Marketable Securities + Accounts Receivable) / Current Liabilities

Current liabilities are obligations due within the next year or operating cycle, such as short-term debt, accounts payable, accrued expenses, and other near-term obligations.

An alternative version starts with current assets and removes items that are normally less liquid:

Quick Ratio = (Current Assets – Inventory – Prepaid Expenses) / Current Liabilities

Both versions are trying to isolate quick assets: assets that are already cash or closer to cash than inventory. The result is often written as a ratio, such as 1.2, or as coverage, such as 1.2 times current liabilities.

Formula caution: The calculation is only as useful as the input quality. Accounts receivable may be included in quick assets, but receivables are less reliable when customers pay slowly, disputes are common, or one customer represents a large share of the balance.

What Counts as Quick Assets

Quick assets are the current assets most likely to support near-term payment needs. The exact presentation can vary by company and accounting disclosure, so investors should read the balance sheet notes instead of relying only on the headline number.

| Balance sheet item | Typical quick-ratio treatment | Investor interpretation |

|---|---|---|

| Cash and cash equivalents | Included | Usually the cleanest quick asset because it is already liquid. |

| Marketable securities | Usually included | Useful when securities can be sold without major loss or delay. |

| Accounts receivable | Usually included | Helpful only when collection quality, customer concentration, and payment timing are reasonable. |

| Inventory | Usually excluded | Excluded because sale timing, markdown risk, and demand conditions can make conversion uncertain. |

| Prepaid expenses | Usually excluded | Excluded because they may reduce future expenses but normally cannot pay current liabilities directly. |

Quick Ratio Calculation Example

Assume a company reports the following current balance sheet items:

| Item | Amount | Included in quick assets? |

|---|---|---|

| Cash and cash equivalents | $2 million | Yes |

| Marketable securities | $1 million | Yes |

| Accounts receivable | $3 million | Yes |

| Inventory | $4 million | No |

| Prepaid expenses | $1 million | No |

| Current liabilities | $4 million | Denominator |

Calculation: Quick assets are $2 million of cash, $1 million of marketable securities, and $3 million of accounts receivable, for a total of $6 million. Current liabilities are $4 million. The quick ratio is $6 million divided by $4 million, or 1.5.

A quick ratio of 1.5 means the company reports $1.50 of quick assets for every $1.00 of current liabilities. That does not automatically mean the company is safe. The interpretation still depends on whether receivables convert into cash, whether liabilities are due immediately, whether the business needs heavy reinvestment, and whether operating cash flow supports the balance sheet.

How Investors Interpret the Quick Ratio

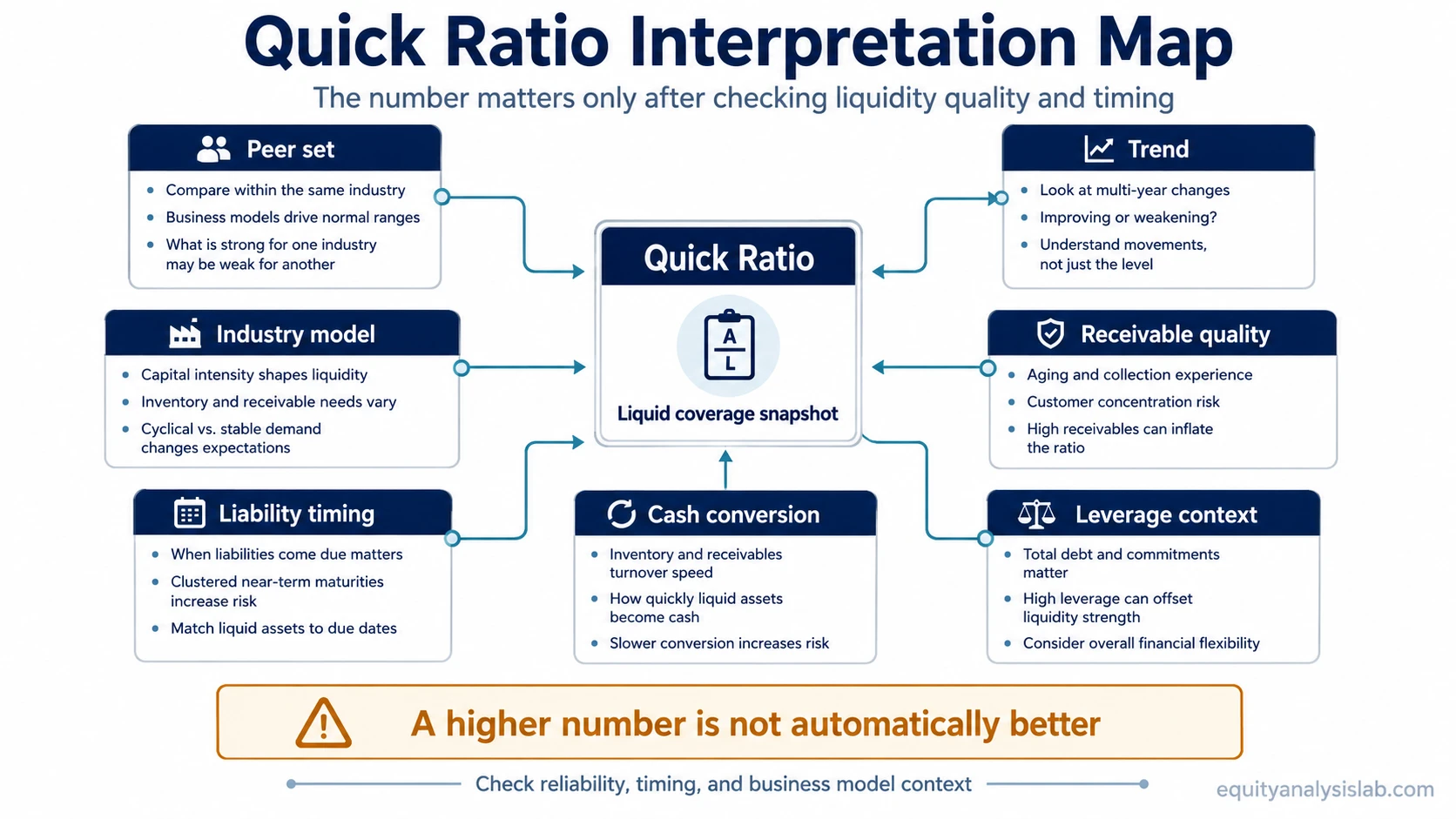

A quick ratio is stronger when it is supported by high-quality receivables, stable cash conversion, manageable near-term liabilities, and a business model that does not require constant emergency financing. A high number is weaker when the numerator depends heavily on receivables that may not convert quickly.

| Interpretation gate | What to check | Why it changes the quick ratio reading |

|---|---|---|

| Peer set | Compare companies with similar operating models, inventory needs, and payment cycles. | A normal quick ratio can differ across industries because working-capital structures differ. |

| Trend | Check whether the ratio is improving, stable, or deteriorating across several periods. | A one-period snapshot can hide whether liquidity is strengthening or weakening. |

| Industry model | Review whether the company relies on inventory, subscriptions, receivables, or upfront customer cash. | The same ratio can mean different things in asset-light software, retail, manufacturing, or distribution models. |

| Receivable quality | Check customer concentration, overdue receivables, disputes, allowances, and collection history. | Receivables count as quick assets, but weak collectability can make the ratio look stronger than reality. |

| Liability timing | Review what is due soon, what can roll forward, and whether large obligations cluster in the near term. | Current liabilities are grouped on the balance sheet, but payment timing may not be evenly distributed. |

| Cash conversion | Compare quick ratio with operating cash flow and working-capital movement. | Accounting liquidity is less convincing when the business is not converting sales into cash. |

| Leverage context | Compare near-term liquidity with broader capital structure and refinancing risk. | A company can pass a short-term liquidity check while still carrying meaningful leverage risk. |

The most useful reading combines quick ratio with cash conversion and balance-sheet context. Reported liquid assets matter, but cash flow before narrative remains a stronger test when receivables are large or working capital is moving against the company.

What Is a Good Quick Ratio?

A good quick ratio depends on the company’s industry, operating model, liability schedule, receivable quality, and cash-flow profile. A ratio above 1.0 is often viewed as more comfortable than a ratio below 1.0 because quick assets exceed current liabilities, but that threshold should not be treated as a universal safety line.

A company with a quick ratio below 1.0 may still operate normally if it has predictable cash inflows, strong supplier terms, recurring revenue, or access to financing. A company with a quick ratio above 1.0 may still face pressure if receivables are slow, customers are concentrated, marketable securities are volatile, or large liabilities are due soon.

Common mistake: Treating a high quick ratio as proof of financial strength can create false comfort. Liquidity quality depends on the timing and reliability of cash conversion, not only on the size of quick assets at one balance sheet date.

Quick Ratio vs Current Ratio

Quick ratio is stricter than current ratio because it removes inventory and prepaid expenses from the asset side of the calculation. Current ratio compares all current assets with current liabilities, while quick ratio focuses on assets that are closer to cash.

Quick ratio: Best for a stricter liquid-asset check when inventory may not convert into cash quickly.

Current ratio: Best for a broader current-asset coverage check that includes inventory and other current assets.

The difference matters most when inventory is large, slow-moving, seasonal, or exposed to markdown risk. In those cases, current ratio may look comfortable while quick ratio gives a more cautious liquidity reading.

When the Quick Ratio Can Mislead

The ratio can be useful and still incomplete. It is built from balance sheet values at a point in time, while real liquidity depends on cash movement, liability timing, customer behavior, and access to financing.

Receivables may not convert quickly: Accounts receivable can inflate quick assets when customers pay slowly, dispute invoices, or represent concentrated credit risk.

Marketable securities may lose liquidity: Securities that appear liquid in normal conditions may become harder to sell at full value during stress.

The balance sheet is a snapshot: A reporting-date ratio may not show daily liquidity needs, seasonal working-capital pressure, or large payments just after period-end.

Near-term cash needs may be hidden: Payroll, supplier payments, debt maturities, tax obligations, and capital spending may create pressure that the ratio does not fully capture.

A high ratio can have mixed meaning: Excess cash may show flexibility, but it can also reflect underinvestment, weak reinvestment opportunities, or unusual working-capital timing.

Liquidity analysis becomes more balanced when quick ratio is compared with operating cash flow, debt maturity, supplier terms, customer collections, and management’s capital allocation needs.

Related Metrics

This measure works best as one part of a company-analysis toolkit. Debt-to-equity ratio adds leverage context by comparing debt financing with shareholder equity, while quick ratio focuses on short-term liquid coverage.

Asset turnover ratio answers a different question: how efficiently a company uses assets to generate revenue. A company can be liquid but inefficient, or efficient but exposed to short-term liquidity pressure.

Use quick ratio for: near-term liquid coverage.

Use current ratio for: broader current-asset coverage.

Use debt-to-equity ratio for: leverage and capital-structure context.

Use asset turnover ratio for: asset efficiency rather than liquidity.

FAQ

What is quick ratio?

Quick ratio is a liquidity ratio that compares cash, marketable securities, and accounts receivable with current liabilities. It is also called the acid-test ratio.

What is the quick ratio formula?

The common formula is cash plus marketable securities plus accounts receivable, divided by current liabilities. Another version is current assets minus inventory and prepaid expenses, divided by current liabilities.

What is a good quick ratio?

A good quick ratio depends on industry, business model, receivable quality, liability timing, and cash conversion. A ratio above 1.0 can be more comfortable, but it is not a universal safety threshold.

Is quick ratio the same as current ratio?

No. Quick ratio usually excludes inventory and prepaid expenses, while current ratio includes all current assets. Quick ratio is the stricter liquidity measure.

Can quick ratio be misleading?

Yes. Quick ratio can be misleading when receivables are slow to convert, marketable securities are less liquid than expected, liabilities are due sooner than they appear, or operating cash flow is weak.