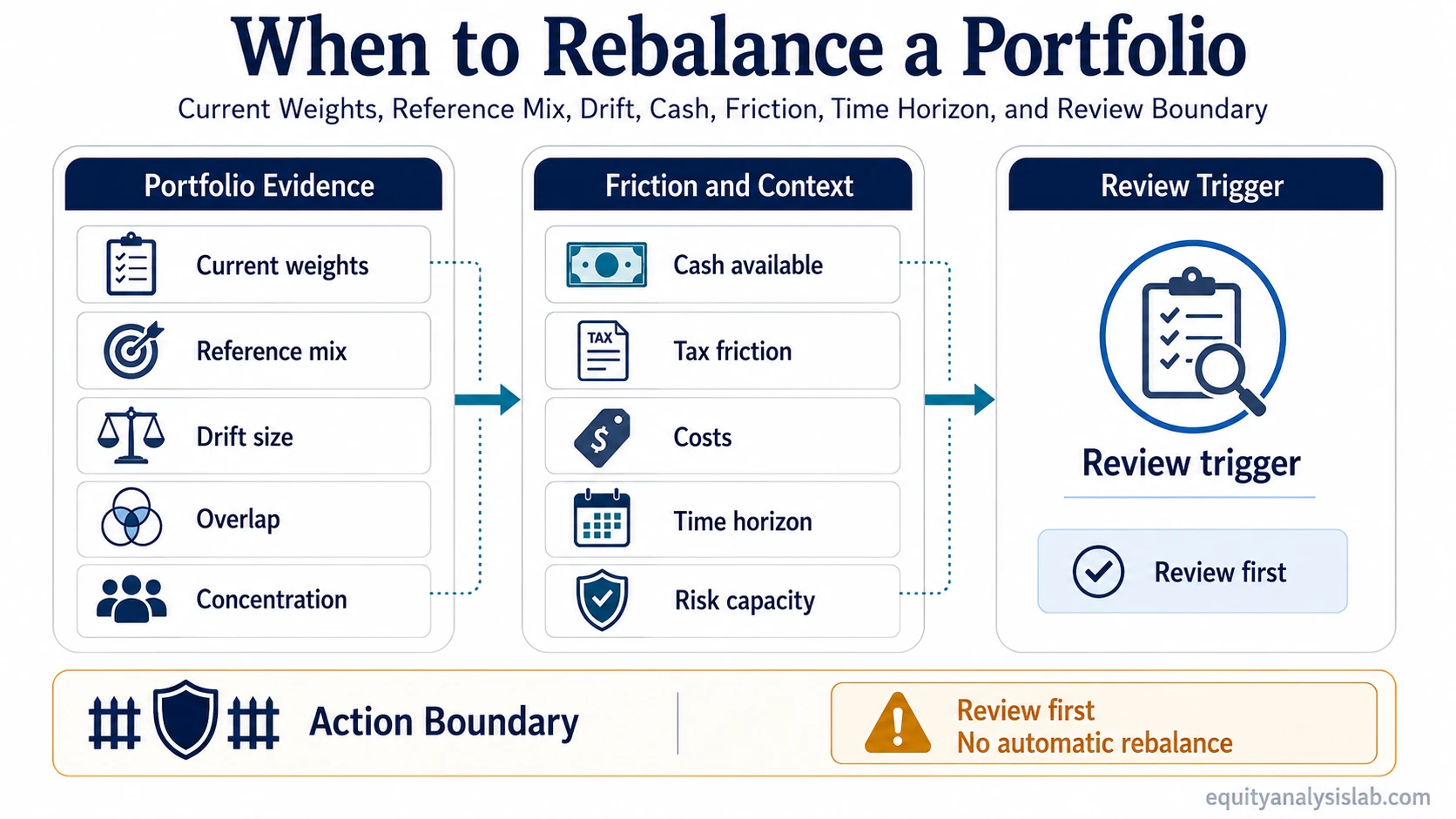

A portfolio usually becomes ready for a rebalancing review when current weights have moved far enough from the reference mix, review rule, or risk boundary to justify checking drift, overlap, concentration, cash, costs, taxes, time horizon, and risk capacity. The trigger is a reason to review the portfolio, not an automatic instruction to trade.

The trigger identifies when the portfolio deserves attention; it does not decide whether holdings should be sold, bought, or left unchanged.

Useful timing depends on observable evidence. A price move changes account value, but it does not always change portfolio exposure enough to justify action. The key distinction is movement versus drift: movement describes what markets did, while drift describes how far the portfolio has moved away from its intended mix.

Practical definition: Rebalancing timing is the point at which portfolio evidence makes a review reasonable. That evidence usually includes current weights, target weights, drift size, holding overlap, concentration, cash availability, tax or transaction friction, and whether the investor’s risk capacity still matches the portfolio’s exposure.

When a Rebalancing Review Becomes Relevant

A rebalancing review becomes relevant when the current portfolio no longer reflects the mix it was designed to hold. That can happen after strong gains in one asset class, a sharp decline in another, large contributions or withdrawals, dividend accumulation, cash buildup, or a change in risk capacity.

The allocation check starts with a comparison between current weights and reference weights. If the intended mix is 70% equities and 30% defensive assets, a move to 78% equities does not automatically require a rebalance, but it does create a clearer reason to examine exposure, risk, cash needs, and friction.

The most useful question is not “Did the market move?” The better question is “Did the portfolio’s actual exposure move far enough away from the intended mix to change the investor’s risk profile?” That keeps the decision tied to evidence instead of discomfort, headlines, or recent volatility.

Calendar-Based vs Threshold-Based Rebalancing

Calendar-based rebalancing uses a fixed review schedule, such as quarterly, semiannual, or annual review. The schedule creates discipline because the portfolio is checked even when markets feel quiet. Its weakness is that a calendar date may arrive when drift is small and action would add unnecessary friction.

Threshold-based rebalancing uses a drift band around the reference mix. The portfolio is reviewed when an allocation moves beyond the chosen band. This can be more responsive to actual exposure change, but it still should not be treated as a mechanical rule that fits every investor, account type, or market condition.

A combined method uses the calendar as the review rhythm and the threshold as the action filter. For example, an investor may review the portfolio on a set schedule, then act only if drift, concentration, cash, taxes, costs, and risk capacity support a change. This separates review discipline from automatic rebalancing.

| Review method | What triggers the review | Main limitation |

|---|---|---|

| Calendar-based review | A scheduled review date arrives. | The date may not match meaningful portfolio drift. |

| Threshold-based review | An allocation moves beyond a chosen drift band. | The band can ignore taxes, cash needs, overlap, and account type. |

| Combined review | A scheduled review checks whether drift is large enough to matter. | The rule still needs judgment around friction and risk capacity. |

What to Check Before Rebalancing

The evidence check should separate five things: market movement, portfolio drift, exposure change, review trigger, and actual action. A portfolio can experience market movement without meaningful drift. It can show drift without requiring immediate action. It can also appear diversified by asset count while remaining concentrated by underlying exposure.

Allocation drift is only one part of the timing question. The same drift percentage can mean different things in a taxable account, a tax-advantaged account, a concentrated portfolio, or a portfolio with incoming cash that can adjust weights without selling existing positions.

| Evidence item | What it shows | Why it affects timing |

|---|---|---|

| Current weights | The portfolio’s actual allocation today. | Timing cannot be assessed without knowing what the portfolio actually holds now. |

| Reference mix | The intended allocation or policy mix. | Drift only has meaning when compared with a defined reference point. |

| Drift size | The gap between current and intended weights. | Larger drift can change risk exposure more than small movement inside the normal range. |

| Overlap | Whether different funds or holdings own similar underlying exposures. | A portfolio can look diversified while the same stocks, sectors, or factors dominate risk. |

| Concentration | Whether one position, sector, or factor controls too much portfolio behavior. | High concentration can make timing more relevant even if broad asset-class weights look acceptable. |

| Cash availability | Whether new money, dividends, or existing cash can adjust weights. | Cash can reduce the need to sell holdings purely to restore balance. |

| Tax and transaction friction | The cost of acting in the account where the change would occur. | Small drift may not justify taxable gains, trading costs, spreads, or operational friction. |

| Time horizon | How long the capital is expected to remain invested. | Shorter horizons can change the acceptable balance between risk, liquidity, and turnover. |

| Risk capacity | The investor’s ability to absorb volatility or loss without forcing bad decisions. | A portfolio that no longer fits risk capacity may deserve review even if the drift rule has not been breached. |

When Not to Rebalance Automatically

Rebalancing should not be automatic just because markets moved, a position gained value, or recent volatility feels uncomfortable. A portfolio can move without becoming misaligned. A position can rise without creating unacceptable concentration. Volatility can feel uncomfortable without creating a clear allocation problem.

Common mistake: Treating discomfort as the trigger. A market decline, a sharp rally, or a stressful news cycle can make the portfolio feel wrong before the evidence confirms that weights, overlap, concentration, or risk capacity have actually changed enough to matter.

Better framing: Check the evidence first. Compare current weights with the reference mix, check drift and hidden exposure, then weigh taxes, transaction costs, cash needs, and time horizon before deciding whether any action is justified.

Another mistake is treating asset count as diversification. A portfolio with several funds may still hold similar mega-cap stocks, sector exposure, style exposure, or factor exposure underneath. In that case, rebalancing by label alone can leave the real concentration problem unresolved.

Limitation: Rebalancing can create false diversification if the portfolio is adjusted at the category level while the underlying holdings remain highly overlapping. The exposure check should look through the labels far enough to identify the holdings, sectors, or factors that actually drive portfolio risk.

How Cash, Costs, and Taxes Affect Timing

Cash can change the timing decision because new contributions, dividends, interest, or planned withdrawals may adjust the portfolio without selling existing holdings. A planned contribution can be directed toward underweight areas, while a withdrawal can come from overweight areas if that fits the investor’s constraints.

A large cash position may also need its own review. Cash can create flexibility, but it can also leave the portfolio underexposed to the intended mix if it remains higher than planned for too long.

Cash drag becomes relevant when excess cash reduces participation in the portfolio’s intended exposure. That does not mean all cash should be invested immediately. It means the cash level should be judged against the portfolio’s purpose, liquidity needs, and risk boundary.

Taxable accounts require extra care because selling appreciated holdings can create tax consequences. Transaction costs, bid-ask spreads, fund restrictions, and account rules can also make small changes less useful. The timing decision should compare the benefit of restoring the mix with the friction created by the action.

A Simple Rebalancing Timing Example

Assume a reference mix is 70% equity exposure and 30% defensive exposure. After a strong equity rally, the current mix becomes 78% equity and 22% defensive. That change creates a review trigger because the portfolio now carries more equity exposure than intended.

The maintenance check still does not end with automatic selling. If new cash is arriving soon, the investor may be able to direct it toward the defensive side. If the account is taxable, selling appreciated assets may create friction. If the equity exposure is concentrated in overlapping funds, the real risk may be larger than the headline 78% number suggests.

The useful conclusion is that the timing question depends on the full evidence set, not the drift number alone.

Review Trigger vs Action Decision

The cleanest way to think about rebalancing timing is to separate a review trigger from an action decision. A review trigger says, “The portfolio deserves closer inspection.” An action decision says, “The evidence and constraints justify a specific adjustment.”

That separation prevents overtrading when drift is small, but it also prevents neglect when exposure has quietly changed. The review can lead to no action, a contribution adjustment, a withdrawal adjustment, a cash deployment, a partial rebalance, or a delayed decision if the friction is too high relative to the benefit.

Process note: The strongest rebalancing review usually starts with the reference mix, then checks current weights, drift, overlap, concentration, cash, taxes, costs, time horizon, and risk capacity. Action comes only after those items are clear enough to support it.

FAQ

Does market volatility mean a portfolio should be rebalanced?

Market volatility alone is not enough. The stronger trigger is whether volatility has changed current weights, hidden exposure, concentration, or risk alignment enough to justify a review.

Is threshold-based rebalancing better than calendar-based rebalancing?

Neither method is universally better. A threshold can tie review to actual drift, while a calendar can create discipline. A combined approach often separates scheduled review from the decision to act.

Should taxes stop a portfolio from being rebalanced?

Taxes should be considered as friction, especially in taxable accounts, but they do not automatically prevent rebalancing. The decision should compare the risk benefit of restoring the mix with the tax and transaction cost created by the action.