Portfolio drift occurs when the current weights or exposures inside a portfolio move away from the intended reference mix. The drift can come from market performance, contributions, withdrawals, partial sales, new purchases, changing cash balances, or overlapping holdings that make the real exposure different from the visible holding list.

Definition: Portfolio drift is the gap between a portfolio’s intended or reference exposure and its current exposure. It is an observation about portfolio structure, not an automatic instruction to rebalance, sell, buy, or change allocation.

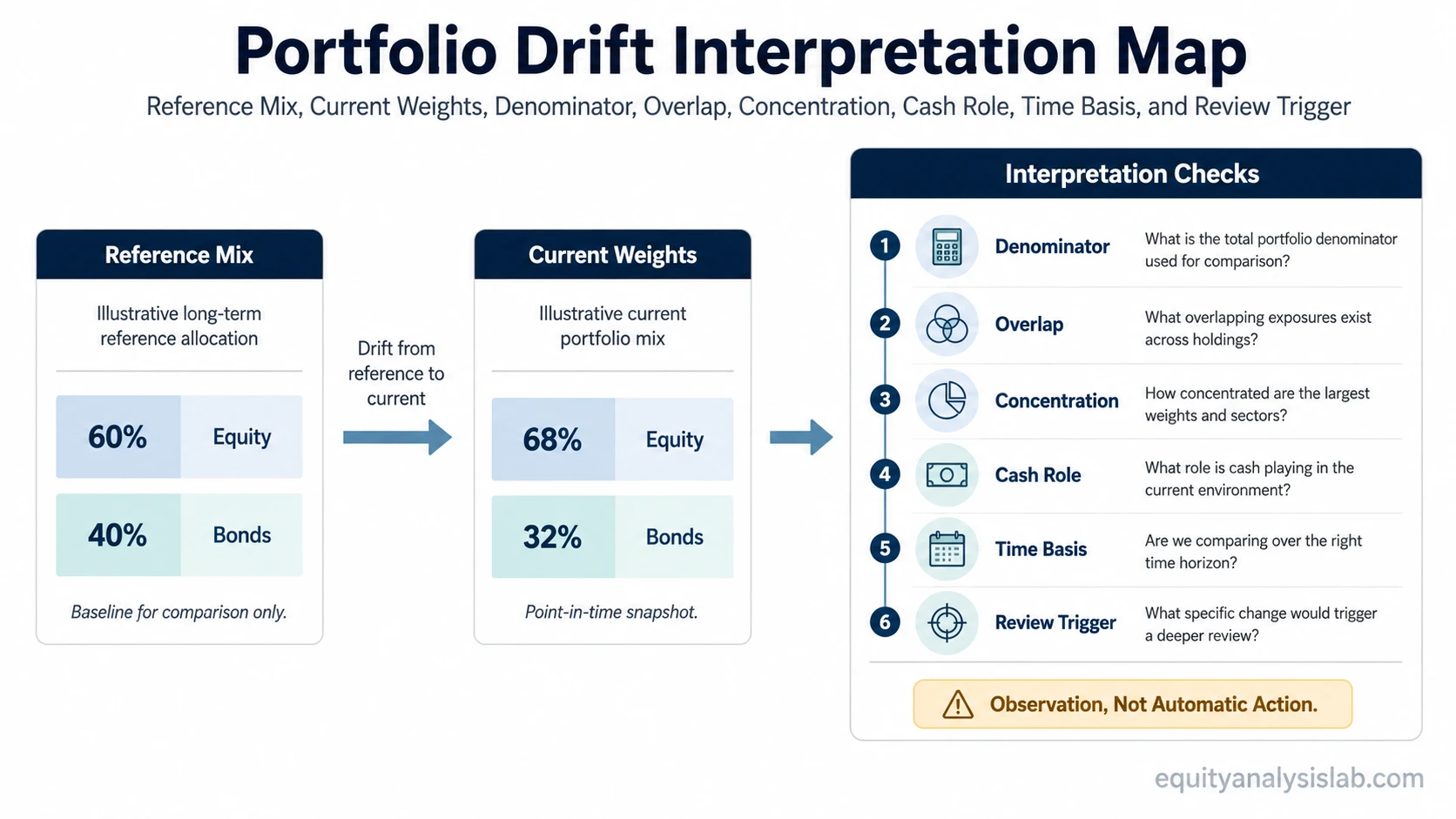

The useful question is not only whether a percentage has moved. A clearer interpretation depends on the reference mix, current denominator, cash role, overlap, concentration, time basis, and review trigger being visible together.

Key Points

- Portfolio drift compares intended exposure with current portfolio weights.

- Market movement is one cause, but cash flows, partial transactions, and hidden overlap can also change exposure.

- Drift is a review input. It does not prove that rebalancing, trading, or any other action is required.

- The same drift amount can mean different things depending on concentration, cash role, time horizon, and risk capacity.

What Portfolio Drift Means

Portfolio drift means the actual portfolio no longer matches the reference structure used to monitor it. That reference may be a target allocation, a policy mix, a model portfolio, or a personal planning baseline. Without that reference point, the word drift becomes loose because there is nothing stable to compare the current portfolio against.

A portfolio can drift even when no new decision has been made. If one asset class, sector, factor, region, or individual holding rises faster than the rest, its weight can become larger. If another part falls, receives less new capital, or is diluted by new deposits, its weight can shrink. The portfolio may still contain the same holdings while the exposure profile changes.

That distinction matters because portfolio drift is about actual exposure, not simply the number of positions owned. A list of ten holdings can look diversified while two or three positions, sectors, or overlapping funds carry most of the portfolio’s risk.

How Portfolio Drift Changes Actual Exposure

Portfolio weights move because portfolio components do not rise and fall at the same pace. A stock sleeve may grow faster than a bond sleeve. A sector fund may overlap with several individual holdings. A new cash deposit may temporarily lower invested exposure. A withdrawal may change the denominator used to calculate every position weight.

The cleanest sequence is detection, interpretation, and then a portfolio maintenance check. Detection identifies the current exposure. Interpretation asks what changed. The final check belongs to a broader review discipline, not to the drift observation by itself.

Drift can also appear through hidden concentration. A portfolio may hold several funds with different names, but if those funds share large underlying positions or the same sector bias, current exposure may be more concentrated than the surface holdings suggest.

Portfolio Drift Interpretation Inputs

A portfolio drift comparison is stronger when the inputs are explicit. The same current weight can be harmless, unresolved, or material depending on what the investor is comparing it against and why that comparison exists.

| Input checked | What it clarifies | Mistake it helps prevent |

|---|---|---|

| Target or reference mix | The baseline used to define whether exposure has moved | Calling every weight change drift without a stable reference point |

| Current weights | The actual percentage now assigned to each sleeve, asset class, sector, or position | Relying on old allocation numbers after market movement |

| Denominator | Whether weights are measured against total portfolio value, invested assets, or a narrower sleeve | Comparing percentages that were calculated on different bases |

| Overlap | Whether funds or holdings share the same underlying exposure | Treating different tickers or funds as separate risk sources when they behave similarly |

| Concentration | Whether a small number of holdings, sectors, or factors now dominate the portfolio | Confusing holding count with diversification |

| Cash role | Whether cash is temporary, strategic, pending deployment, or needed for liquidity | Misreading a temporary cash flow as a permanent allocation change |

| Time basis | Whether the drift is short-lived, gradual, or persistent across review periods | Reacting to a single snapshot without knowing how long the exposure has been different |

| Risk capacity boundary | Whether the changed exposure still fits the investor’s ability to absorb risk | Reducing drift to a number while ignoring the portfolio’s practical risk boundary |

| Review trigger | Whether the drift is large, persistent, or relevant enough to justify a closer look | Treating detection as the same thing as action |

A Simple Portfolio Drift Example

A portfolio starts with a 60% equity and 40% bond reference mix. After a period where the equity sleeve rises and the bond sleeve is roughly flat, the current mix becomes 68% equity and 32% bonds. The portfolio has drifted because the actual exposure no longer matches the reference mix.

Illustrative example: The 68% equity weight does not automatically mean the portfolio must be changed. It first shows that the portfolio now carries more equity exposure than the reference mix. A stronger interpretation would check why the weight changed, whether new cash flows affected the denominator, whether equity exposure is concentrated in a few holdings, and whether the change matters for the next review.

The same 68% equity weight can carry a different interpretation if it came from broad equity appreciation, one concentrated holding, a temporary cash withdrawal, or overlapping funds that increased the same underlying exposure.

The arithmetic drift is visible first. The interpretation comes after the inputs are checked.

Portfolio Drift vs Rebalancing

Portfolio drift is the condition. Rebalancing is a possible response that may be considered after the exposure change is understood. Blending the two too early creates a common error: the investor sees a gap between target and current weights, then treats the gap as if it already contains the answer.

A cleaner sequence is detect, interpret, then decide whether closer inspection is warranted. Detection answers what changed. Interpretation asks whether the change affects exposure, concentration, cash role, or risk capacity. The later decision may include action, delay, or no change.

Limitation: Portfolio drift does not say which action is correct. It does not set a rebalance schedule, define a threshold, solve tax questions, or determine whether a position should be bought or sold.

Portfolio Drift vs Cash Drag, Cash Position, and Portfolio Turnover

Cash drag describes the effect of cash sitting outside intended exposure. Portfolio drift is broader because any portfolio component can move away from the reference mix, not only cash.

A portfolio cash position describes the role and weight of cash inside the portfolio. Portfolio drift asks whether that cash weight, along with other portfolio weights, still matches the intended structure.

Portfolio drift also differs from activity-driven changes. A portfolio can drift without trades if market prices move unevenly, while changes caused by buying and selling holdings create a separate activity and cost question.

Common Portfolio Drift Mistakes

| Mistake | Safer interpretation |

|---|---|

| Treating drift as automatic action | A drift comparison identifies a change in exposure; it does not decide the response. |

| Measuring only the number of holdings | Holding count can hide concentration if several positions share the same sector, factor, geography, or underlying companies. |

| Ignoring overlap | Multiple funds can create repeated exposure to the same large holdings or market segment. |

| Mixing denominators | A position can look different when measured against total assets, invested assets, or a single sleeve. |

| Confusing temporary cash flow with structural drift | New deposits, withdrawals, dividends, or pending transactions can change weights before the portfolio’s longer-term structure has changed. |

When a Portfolio Drift Reading Is Incomplete

An exposure check is incomplete when the reference mix is unknown, the current weights are stale, the denominator is unclear, or the time basis is missing. A single snapshot can identify a possible gap, but it cannot explain whether the gap is persistent, temporary, intentional, or relevant to the investor’s risk boundary.

The interpretation is also incomplete when overlap and cash role are not checked. A portfolio can appear close to its reference allocation while hidden fund overlap increases exposure to the same group of companies. Another portfolio can appear to drift because cash has grown, while the cash is actually reserved for a known liquidity need.

Drift interpretation sequence: reference mix → current weights → denominator → overlap → concentration → cash role → time basis → review trigger. Skipping the middle steps turns a structural observation into a premature conclusion.

FAQ

What is portfolio drift?

Portfolio drift is the movement of current portfolio weights or exposures away from an intended reference mix. It can happen because holdings perform differently, cash flows change the denominator, or overlapping holdings alter real exposure.

Is portfolio drift the same as rebalancing?

No. Portfolio drift is the observed condition. Rebalancing is one possible process that may be reviewed after the drift is understood, but drift alone does not require a specific action.

Can a portfolio drift without any trades?

Yes. A portfolio can drift when some holdings rise or fall more than others. The holdings may stay the same while their weights and exposure contribution change.

Why can hidden overlap matter in portfolio drift?

Hidden overlap can make exposure more concentrated than the holding list suggests. Several funds or positions may appear separate while sharing the same companies, sectors, factors, or market drivers.