Portfolio turnover measures how much buying and selling activity occurred inside a portfolio over a defined period. It is usually expressed as a percentage of average portfolio value, so a higher number means more of the portfolio was replaced or traded during that period.

Definition: Portfolio turnover is the ratio of portfolio transaction activity to average portfolio value over a measurement period. It helps investors see how active the portfolio was, but it does not prove whether the activity was good, bad, disciplined, or excessive.

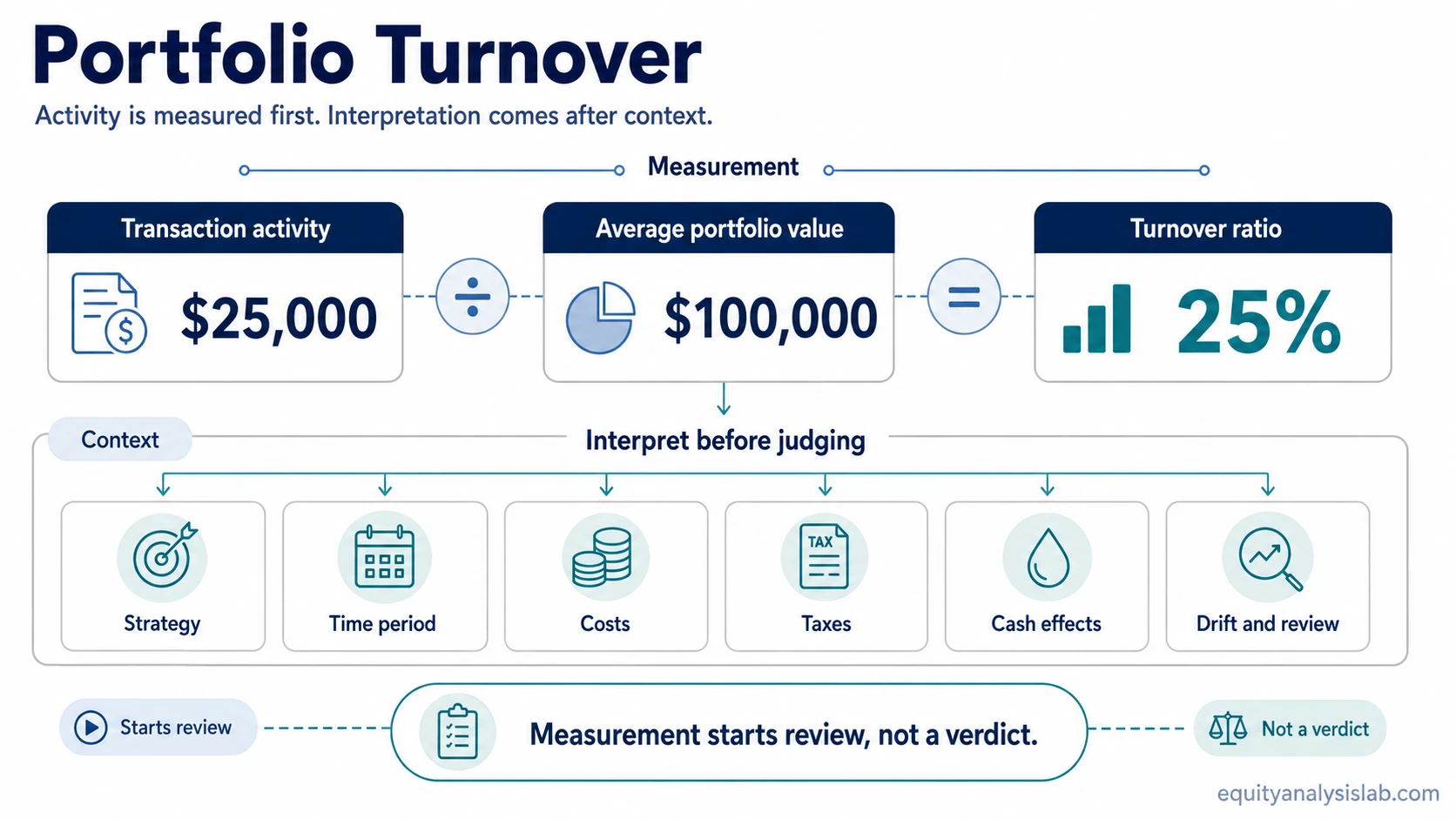

The useful interpretation starts with the measurement. A turnover number can reflect normal rebalancing, manager activity, cash deployment, security replacement, tax-sensitive decisions, or a change in the portfolio’s intended exposure. The ratio becomes more useful when it is compared with the portfolio’s strategy, time period, account context, and peer set.

Key Points

- Portfolio turnover measures transaction activity, not investment quality by itself.

- The basic calculation compares purchases or sales activity with average portfolio value over a period.

- The same turnover rate can mean different things depending on strategy, time horizon, account type, and reporting convention.

- High turnover can raise cost and tax questions, while low turnover can still hide stale exposure or weak review discipline.

- Turnover should be read as one portfolio-maintenance signal, not as a standalone instruction.

Portfolio Turnover Formula

The common formula compares transaction activity with average portfolio value:

Portfolio turnover rate = transaction activity ÷ average portfolio value

Transaction activity is often represented by the lower of total purchases or total sales over the measurement period. Average portfolio value is usually the average size of the portfolio during the same period. The result is commonly converted into a percentage.

For example, a turnover rate of 40% means transaction activity equaled 40% of the portfolio’s average value during the measured period. It does not automatically say whether that activity was necessary, costly, tax-efficient, or well aligned with the strategy.

What the Formula Inputs Change

The formula looks simple, but each input changes the interpretation. A turnover number becomes more reliable when the investor knows what was counted, what period was measured, and what kind of portfolio is being compared.

| Input or context | What it changes | Why it matters | What not to conclude |

|---|---|---|---|

| Purchases or sales | Which side of activity is used in the numerator | Sales may reflect exits, while purchases may reflect new deployment or replacement | Do not assume every transaction was speculative or unnecessary |

| Average portfolio value | The denominator used to scale activity | A smaller average value can make the same transaction amount look larger as a percentage | Do not compare turnover without checking portfolio size and measurement base |

| Measurement period | Whether the number reflects a month, quarter, year, or other review window | Short windows can exaggerate temporary activity, while long windows can smooth it out | Do not compare periods as if they represent the same behavior |

| Strategy mandate | Whether activity is expected for the portfolio’s design | An active strategy and a low-turnover index strategy may have different normal ranges | Do not label high or low turnover as good or bad without strategy context |

| Peer set | The comparison group used to judge whether activity is unusual | Turnover is more meaningful when compared with similar portfolios | Do not compare unlike portfolios as if they have the same job |

| Account type | The relevance of taxes, transaction costs, and reinvestment timing | Taxable and tax-advantaged settings can change the interpretation of the same turnover number | Do not turn a generic turnover rate into a tax conclusion |

| Reporting basis | How the turnover number was calculated or presented | Different reports can use different conventions or time windows | Do not compare reported numbers without understanding the convention |

Simple Portfolio Turnover Calculation Example

Illustrative example: Suppose a portfolio had an average value of $100,000 during the year. During that year, the lower of total purchases or total sales was $25,000.

Calculation: $25,000 ÷ $100,000 = 0.25, or 25% portfolio turnover.

A 25% turnover rate means the measured transaction activity equaled one-quarter of the portfolio’s average value during that period. The number shows activity. It does not prove whether the portfolio was improved, whether the trades were necessary, or whether the investor should change anything.

How to Interpret High or Low Portfolio Turnover

High portfolio turnover usually means the portfolio changed more during the measured period. That may raise questions about transaction costs, taxable gains, manager discipline, strategy consistency, and whether the activity was part of a deliberate review. It may also be normal for a portfolio designed to adjust frequently.

Low portfolio turnover usually means holdings changed less. That may suggest patience, low transaction activity, or a longer holding period. It may also create false comfort if the portfolio has not been reviewed, if exposures have become stale, or if the portfolio has moved away from its intended structure without action.

High turnover is not automatically bad. It may reflect active management, security replacement, risk reduction, cash deployment, or rebalancing after large market moves.

Low turnover is not automatically good. It may reflect discipline, but it may also reflect neglect, legacy holdings, unrealized tax concerns, or a portfolio that has not responded to changing objectives.

The better question is not whether turnover is high or low in isolation. The better question is whether the activity matches the portfolio’s mandate, review period, cost structure, tax setting, and intended exposure.

Costs, Taxes, and Cash Effects

Turnover matters because transactions are not always frictionless. Buying and selling may create direct trading costs, bid-ask spread costs, taxable events in some account types, and timing gaps between sale proceeds and redeployment.

When sales leave money uninvested for longer than intended, the turnover discussion can overlap with cash drag. The issue is not turnover alone, but whether transaction activity creates idle cash exposure that changes the portfolio’s intended return and risk profile.

Turnover may also change the portfolio cash position. A sale raises cash until it is redeployed, while a purchase reduces cash and changes exposure. That cash movement can be temporary, deliberate, or a sign that the review process is incomplete.

Tax interpretation should remain account-specific. A generic turnover number does not show the investor’s tax basis, holding periods, jurisdiction, account type, or realized gain and loss profile. It only flags that transaction activity occurred and may deserve closer review.

Portfolio Turnover vs Portfolio Drift

Portfolio turnover and portfolio drift are related, but they measure different things. Turnover measures buying and selling activity. Drift measures how far portfolio weights have moved from a target or intended allocation.

A portfolio may have high turnover without much allocation drift if trades replace securities inside the same category. A portfolio may also have low turnover and still show meaningful drift in portfolio weights if market prices move and the investor does not rebalance.

| Concept | What it measures | Common confusion |

|---|---|---|

| Portfolio turnover | How much buying and selling occurred during a period | It can be mistaken for portfolio quality or discipline |

| Portfolio drift | How far current weights moved from intended weights | It can be mistaken for transaction activity |

When Portfolio Turnover Can Mislead

Limitation: Portfolio turnover can mislead when it is compared across different strategies, account types, tax settings, reporting bases, peer sets, or review periods.

A turnover number can create a false alarm when activity looks high but the portfolio was intentionally adjusted after a major contribution, withdrawal, mandate change, risk review, or security replacement. The number shows activity, but not the reason for the activity.

It can also create false comfort when activity looks low but the portfolio has not been reviewed. Low activity does not prove that exposures still match the investor’s goals, that concentration risk is controlled, or that the portfolio remains aligned with the intended allocation.

Turnover is most useful when it starts a question: what changed, why did it change, what did it cost, and does the resulting portfolio still match the intended structure?

How Turnover Fits Portfolio Maintenance

Portfolio turnover belongs inside a broader portfolio review process. The ratio can flag activity, but the review has to connect that activity to holdings, costs, taxes, cash, allocation drift, and the investor’s stated objectives.

A useful review does not treat turnover as an instruction. It treats turnover as evidence that something changed. The next step is to understand whether the change was intentional, whether it improved the portfolio’s structure, and whether costs, taxes, cash, or exposure changes remain after the transactions.

FAQ

What is portfolio turnover?

Portfolio turnover is a ratio that measures buying and selling activity inside a portfolio over a defined period. It compares transaction activity with average portfolio value and is usually expressed as a percentage.

How is portfolio turnover calculated?

Portfolio turnover is commonly calculated by dividing transaction activity by average portfolio value for the same period. Transaction activity is often represented by the lower of total purchases or total sales, then converted into a percentage.

Is high portfolio turnover bad?

High portfolio turnover is not automatically bad. It can raise cost, tax, and discipline questions, but its meaning depends on the strategy, time period, account type, peer set, and reason for the activity.

Is low portfolio turnover good?

Low portfolio turnover is not automatically good. It can reflect patience or low costs, but it can also hide stale holdings, allocation drift, or a lack of review if the portfolio has changed around the investor’s objectives.