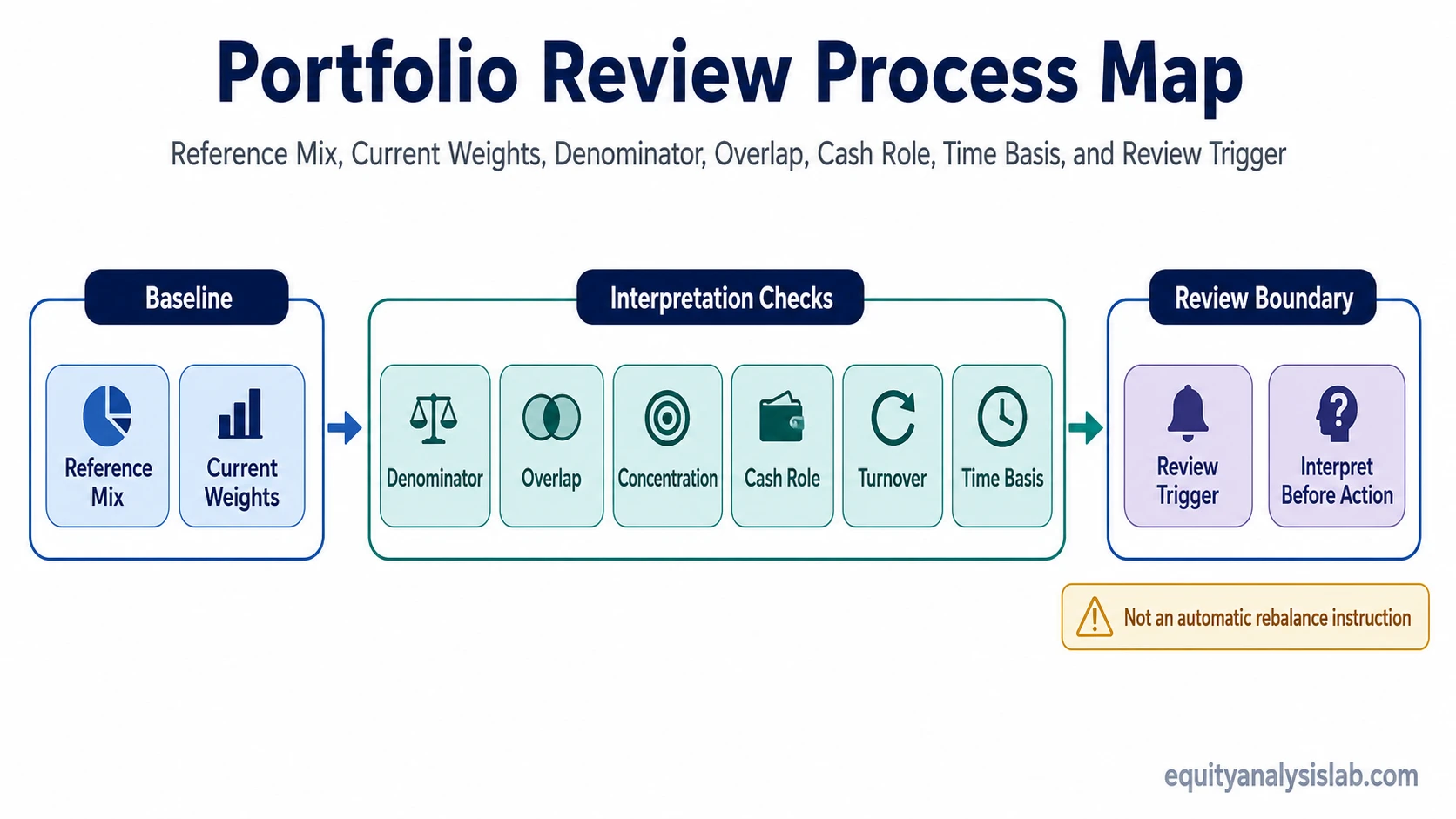

A portfolio review process is often misread as a prompt to rebalance, but its first job is diagnostic. It checks whether the portfolio is being judged against the right reference mix, denominator, time basis, cash role, concentration, and review trigger before any maintenance decision is considered.

The process organizes evidence before action. It can show that the portfolio has moved away from its intended structure, that cash has changed role, that overlap is hiding concentration, or that turnover has increased, but those findings still need interpretation before they become a decision.

Key Points

- A portfolio review process organizes evidence before action.

- Drift, cash role, turnover, and concentration are review inputs, not automatic instructions.

- Review quality depends on the reference mix, denominator, and time basis used.

- A review can identify mismatch, but it cannot prescribe the correct allocation or predict returns.

What a Portfolio Review Process Checks

Definition: A portfolio review process is a diagnostic sequence used to compare a portfolio’s current structure with the reference structure, assumptions, and constraints used to judge it.

The review begins with the question being asked. A portfolio can look acceptable against one reference mix and mismatched against another. For that reason, current weights alone are not enough. The review needs to know what those weights are being compared with, what counts in the denominator, and whether the time period being measured matches the portfolio’s intended horizon.

For a long-term investor, the useful output is not a quick action list. The useful output is a clearer reading of where mismatch, drift, concentration, cash role change, turnover, or trigger-based review pressure may exist.

Common Misread: Review Means Rebalance

Common misread: A review has found a difference, so the portfolio needs to be changed.

Safer interpretation: A review has found something that needs interpretation. The next step may be no action, deeper analysis, a later rebalance decision, a cash role review, or a check against the investor’s original reference mix.

This distinction matters because a review can detect evidence without proving that the evidence is a problem. A sector weight may be higher because one holding appreciated. Cash may be higher because new contributions have not yet been allocated. Turnover may be higher because the portfolio was cleaned up after a thesis change. Each case needs context before the review becomes a maintenance decision.

Portfolio Review Sequence

A useful review sequence separates the observation from the interpretation. The same portfolio can produce different conclusions if the investor uses the wrong denominator, ignores overlap, treats all cash the same way, or compares short-term movement with a long-term reference mix.

| Review step | What to check | Why it matters | What it clarifies next |

|---|---|---|---|

| Reference mix | The intended mix of assets, sectors, position roles, or portfolio buckets. | Without a reference mix, current weights have no stable comparison point. | Whether the review is judging the portfolio against the right target structure. |

| Current weights | The actual portfolio weights at the review date. | Current weights show what the portfolio looks like now, not whether the difference is meaningful. | Whether movement has created material allocation drift. |

| Denominator | Whether weights are measured against total portfolio value, invested capital, risk assets, account value, or another base. | A portfolio can appear less concentrated or less cash-heavy when the denominator is inconsistent. | Whether the review is comparing like with like. |

| Overlap | Shared exposures across funds, stocks, sectors, themes, factors, or business drivers. | Holding count can make diversification look stronger than it is. | Whether different holdings are carrying the same underlying exposure. |

| Concentration | Single-name weight, top holdings, sector weight, factor exposure, or thesis dependence. | Concentration can be intentional or accidental, and the review should not treat both the same way. | Whether one exposure is driving more portfolio behavior than expected. |

| Cash role | Whether cash is a reserve, contribution cash, pending allocation, risk-control buffer, or unintended idle balance. | Cash cannot be interpreted correctly until its role is identified. | Whether the issue is cash structure, cash drag, or no issue at all. |

| Turnover | How much the portfolio has changed through additions, reductions, exits, or replacement positions. | Turnover can reveal maintenance activity, thesis instability, or ordinary portfolio adjustment. | Whether changes need a separate review of process discipline. |

| Time basis | The measurement period used for weights, returns, cash balances, and changes. | A short review window can exaggerate temporary movement, while a long window can hide recent mismatch. | Whether the evidence matches the investor’s actual review horizon. |

| Review trigger | Scheduled review, threshold breach, contribution, withdrawal, major price move, thesis change, or allocation mismatch. | The reason for the review affects what the investor is trying to diagnose. | Whether the review is routine, event-driven, threshold-driven, or mismatch-driven. |

Why Denominator and Time Basis Matter

A portfolio review can create false comfort when the inputs are technically measured but poorly framed. A cash weight measured against total account value may tell a different story than cash measured against the investable portion of the portfolio. A sector weight measured after a large contribution may look different from the same exposure measured before the contribution.

Time basis creates a similar problem. A portfolio can look stable over a full year while drifting meaningfully over the last quarter. It can also look unusually unstable after a short market move even though the long-term structure has not changed much. The review is more useful when the time window matches the reason for the review.

False comfort risk: A portfolio can appear reviewed even when the reference mix, denominator, overlap, cash role, time basis, or trigger is wrong. In that case, the review produces a neat output but weak interpretation.

Cash, Drift, and Turnover in a Review

Cash, drift, and turnover are common review findings, but they are not the same type of issue. Cash is a role question first. Drift is a difference between current exposure and reference exposure. Turnover is a change-intensity question. Combining them into one broad checklist can make the review look complete while hiding the actual source of the mismatch.

Cash needs role identification before judgment. A planned liquidity reserve, a recent contribution, and an unintended idle balance can all appear as cash, but they do not have the same meaning. The relevant next concept may be a cash position, not a performance problem.

Drift needs a reference point. A portfolio that moved from its intended mix may require closer review, but the review still has to separate normal movement from meaningful mismatch. Turnover needs a process reading. A portfolio that changed frequently may reflect disciplined maintenance, changing objectives, or unstable decision-making, depending on the reason for the changes.

Practical Mistake: Treating Every Cash Position as Drag

Practical mistake: An investor sees a visible cash balance and assumes the portfolio has cash drag.

Better review sequence: The review first asks whether the cash is a liquidity reserve, pending contribution cash, planned allocation capacity, or unintended idle balance. Only after the cash role is clear can the investor decide whether cash drag is the relevant interpretation.

This is why a portfolio review process needs more than a checklist. The observation is the cash weight. The interpretation depends on purpose, duration, portfolio role, and whether the cash level still matches the investor’s intended structure.

Review Process vs Rebalancing Decision

A portfolio review process comes before a rebalancing decision. It can show that weights moved, cash changed role, concentration increased, or turnover rose. It does not automatically decide whether any of those findings require action.

Review process: Collects and organizes the evidence: reference mix, current weights, denominator, overlap, concentration, cash role, turnover, time basis, and trigger.

Rebalancing decision: Interprets the evidence against the investor’s rules, objectives, constraints, costs, taxes, and maintenance policy.

The distinction keeps the review from becoming mechanical. A difference can be noted without being corrected immediately. A trigger can be recorded without becoming a trade. A finding can lead to further analysis instead of a portfolio change.

What a Review Process Cannot Tell You

Limitations: A portfolio review process cannot predict returns, prove that a portfolio is safe, identify the correct allocation, or tell an investor what to buy or sell. It can only improve the quality of the evidence used before a later maintenance decision.

The review also cannot remove judgment. Two investors can review similar portfolios and reach different conclusions because their objectives, liquidity needs, risk capacity, tax situation, and time horizon differ. The review process is useful because it makes those differences visible rather than hiding them inside a generic checklist.

Fees and tax considerations may be part of a later maintenance review, but they should remain separate from the diagnostic review itself. The review can flag where costs or taxes may need separate analysis without turning the process into tax strategy or cost optimization advice.

Portfolio Review Framework Summary

A useful portfolio review process is not defined by the longest checklist. It is defined by the order of interpretation: reference mix first, current weights second, denominator and time basis before judgment, then overlap, concentration, cash role, turnover, and trigger.

That order reduces the risk of acting on a weak reading. It helps separate observed facts from interpretation and keeps later maintenance decisions from being driven by a single number taken out of context.

FAQ

Is a portfolio review process the same as rebalancing?

No. A portfolio review process identifies and organizes evidence. Rebalancing is a later decision that may or may not follow from that evidence.

What can trigger a portfolio review?

A review can be scheduled, threshold-based, event-based, or mismatch-based. The useful review trigger depends on the investor’s own portfolio structure and decision process.

Can a portfolio review show that no action is needed?

Yes. A review can identify that the portfolio still matches its reference mix, that cash has a valid role, or that apparent drift is not meaningful enough to require a later maintenance decision.