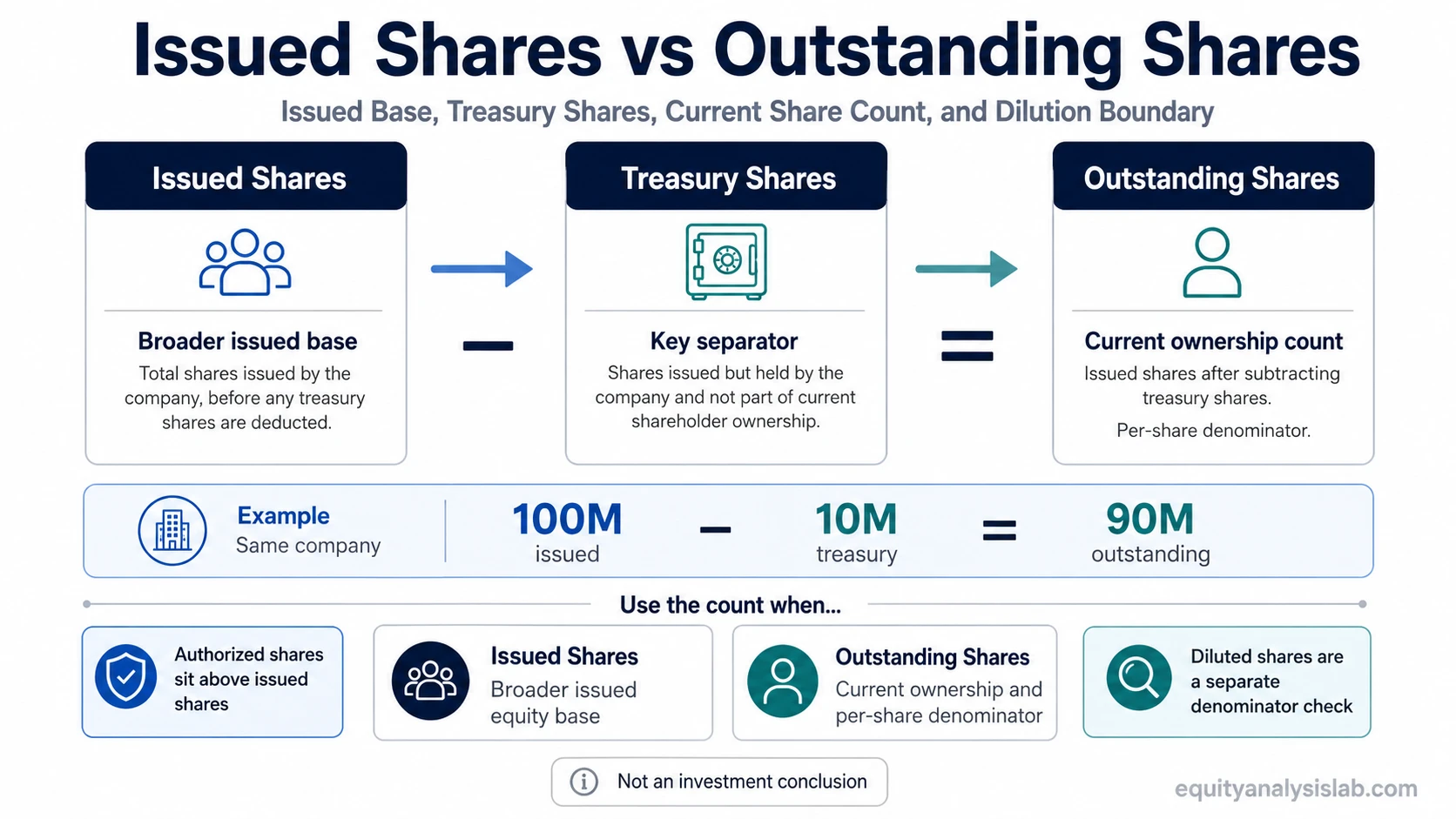

Issued shares are the shares a company has issued at any point, while outstanding shares are the shares currently counted in shareholder hands. The practical difference is treasury stock: shares repurchased and held by the company can remain issued, but they are not outstanding.

For investor analysis, the distinction is not about which number is better. Issued shares describe the broader issued equity base. Shares outstanding usually matter more for ownership percentages, market capitalization context, and per-share metrics because they exclude shares the company holds itself.

Key Points

- Issued shares include the broader group of shares that have been issued by the company.

- Outstanding shares exclude shares held as treasury stock and represent the current shareholder count.

- Treasury stock is the main reason outstanding shares can be lower than issued shares.

- Investors usually look at outstanding shares when they need a current ownership or per-share denominator.

Issued Shares vs Outstanding Shares: The Core Difference

The core difference is whether company-held repurchased shares are still counted. Issued shares can include shares that were issued and later bought back. Outstanding shares exclude shares held as treasury stock.

| Comparison point | Issued shares | Outstanding shares |

|---|---|---|

| Basic meaning | Shares the company has issued. | Shares currently held by shareholders outside the company. |

| Treasury stock treatment | Can include treasury shares if they were issued and later repurchased. | Excludes treasury shares. |

| Investor use | Useful for understanding the broader issued equity base. | Useful for ownership, market capitalization context, and per-share calculations. |

| Common filing context | May appear in share-capital, equity, or note disclosures depending on reporting format. | Often used in per-share metrics, capitalization context, and shareholder-count analysis. |

| Common mistake | Treating issued shares as the current public ownership count. | Assuming outstanding shares include shares the company holds itself. |

The Formula Relationship

Basic relationship: outstanding shares = issued shares minus treasury shares.

This relationship explains why the two numbers are sometimes identical and sometimes different. If a company has issued shares but has not repurchased any into treasury, issued shares and outstanding shares may be the same. If the company holds treasury shares, outstanding shares will usually be lower than issued shares.

This is a share-count relationship, not a valuation conclusion. A lower outstanding share count may affect per-share metrics, but it does not by itself prove that a stock is attractive, cheap, high quality, or likely to perform well.

A Same-Company Example

Suppose a company issues 100 million shares. Later, it repurchases 10 million shares and holds them as treasury stock.

| Step | Issued shares | Treasury shares | Outstanding shares |

|---|---|---|---|

| After issuing shares | 100 million | 0 | 100 million |

| After repurchasing 10 million into treasury | 100 million | 10 million | 90 million |

The issued-share count still describes the broader shares that were issued. The outstanding-share count answers a different question: how many shares are currently counted outside the company for ownership and per-share analysis.

Which Number Should Investors Use?

Use issued shares when the question is about the broader issued equity base. This can help when reading equity notes, understanding share-capital history, or separating issued shares from authorized shares.

Use outstanding shares when the question is about the current ownership base. Market capitalization, ownership percentage, earnings per share context, and many per-share comparisons usually depend on the shares currently outstanding, not the broader issued-share total.

| Investor question | More relevant count | Why |

|---|---|---|

| How many shares are currently counted outside the company? | Outstanding shares | It excludes treasury shares. |

| What is the broader issued equity base? | Issued shares | It starts from shares the company has issued. |

| Why did the current share count fall after buybacks? | Outstanding shares, with treasury-stock context | Repurchased shares may reduce the outstanding count if held by the company. |

| Which denominator is used for per-share analysis? | Usually outstanding shares, with dilution checks | Per-share metrics generally need the current shareholder denominator, while diluted analysis may include potential future shares. |

Common Mistakes When Reading the Two Counts

Mistake 1: reading issued shares as the current ownership count. Issued shares can be broader than the current shareholder count if the company holds treasury shares.

Mistake 2: ignoring filing labels. Companies may present share counts in different sections, notes, or time periods. A number from one disclosure line should not be compared mechanically with another period or label unless the same period, same disclosure basis, and same inclusion rule are checked.

Mistake 3: treating all repurchased shares the same way. Repurchased shares may be held as treasury stock or retired, depending on the company and jurisdiction. That treatment can affect how the issued-share and outstanding-share relationship appears.

Mistake 4: turning the distinction into an investment judgment. Share-count structure can affect analysis, but it does not prove business quality, valuation quality, or future return potential by itself.

Authorized Shares Are a Separate Boundary

Authorized shares are not the same as issued shares or outstanding shares. Authorized shares are the maximum number a company is allowed to issue under its governing documents, subject to the applicable corporate rules and approvals.

That means authorized shares sit above the issued-share count. A company may be authorized to issue more shares than it has actually issued. The lower-level distinction is between issued shares and outstanding shares, where treasury stock is usually the key separator.

Issued Shares, Outstanding Shares, and Diluted Shares

Diluted share count is a separate denominator question. Issued shares and outstanding shares describe current or historical share-count categories, while diluted shares outstanding can include potential shares from instruments such as options, warrants, restricted stock units, or convertible securities when they are dilutive under the relevant reporting rules.

This matters because a company can have a clean outstanding-share count today and still have potential future dilution from securities that are not yet common shares. The issued-versus-outstanding distinction should therefore be read together with treasury-stock treatment, filing labels, and dilution disclosures.

Short Interpretation

Issued shares vs outstanding shares is mainly a denominator problem. Issued shares show what has been issued. Outstanding shares show what is currently counted outside the company. The difference becomes important when treasury stock, buybacks, retired shares, per-share metrics, or filing labels change the share-count lens.

FAQ

Can issued shares and outstanding shares be the same?

Yes. They can be the same when the company has no treasury shares or when no repurchased shares are being held in a way that separates the issued count from the outstanding count.

Why are outstanding shares lower than issued shares?

Outstanding shares are usually lower when the company has repurchased shares and holds them as treasury stock. Those shares may remain issued, but they are not counted as outstanding.

Are issued shares or outstanding shares better for investors?

Neither number is automatically better. Issued shares help explain the broader issued base, while outstanding shares are usually more useful for current ownership and per-share analysis.