Equal weighted and market cap weighted portfolios can hold the same companies, but they assign influence differently: market-cap weighting gives larger companies more weight, while equal weighting gives each constituent the same starting weight.

The difference changes how much the portfolio depends on its largest holdings, how often weights need to be reset, how exposure drifts over time, and how sector or style tilts can appear. Neither method is automatically better. The useful comparison is how each weighting rule changes portfolio behavior.

Key Points

- Market-cap weighting links each holding’s weight to its market value, so larger companies receive more influence.

- Equal weighting gives each holding the same starting weight, so smaller constituents receive more influence than they would in a market-cap weighted version.

- The two methods can own the same securities while producing different concentration, drift, rebalancing, and risk readings.

- Equal weight can reduce single-name dominance, but it can also increase turnover and shift exposure toward smaller companies or different sectors.

- Market-cap weight can be simple and self-adjusting, but it can become top-heavy when a small group of large companies dominates the index.

What Equal Weighted vs Market Cap Weighted Means

A market-cap weighted portfolio assigns larger weights to companies with larger total market value. In an index, that means a company with a larger market capitalization has more influence over index movement than a smaller company in the same index.

An equal weighted portfolio starts each constituent at the same percentage weight. If an index has 100 holdings, each holding would start at 1%. If it has 500 holdings, each holding would start at 0.2%. Those weights do not stay equal automatically, because prices move after the reset date.

Market-cap weighted: Weight follows company size as measured by market value.

Equal weighted: Weight starts the same for every constituent, regardless of company size.

Equal Weight vs Market Cap: Key Differences

The core distinction is not the list of holdings. The core distinction is the weighting rule. Two portfolios can hold identical companies but behave differently because the largest positions, smaller positions, and rebalancing rules are not the same.

| Comparison point | Market-cap weighted | Equal weighted |

|---|---|---|

| Weight source | Company market value determines the weight. | Every constituent receives the same starting weight. |

| Largest-stock influence | Higher when a few large companies dominate the index. | Lower at each rebalance date because each holding starts equally. |

| Smaller-stock influence | Lower because smaller companies receive smaller weights. | Higher because smaller companies receive the same starting weight as larger companies. |

| Rebalancing need | Lower because weights adjust naturally with market value. | Higher because weights must be reset to equal allocations. |

| Drift behavior | Winners become larger weights as their market value rises. | Weights drift between rebalance dates and are reset on schedule. |

| Common interpretation issue | Can look diversified by holding count while remaining top-heavy. | Can look balanced by holding weight while adding turnover or smaller-company exposure. |

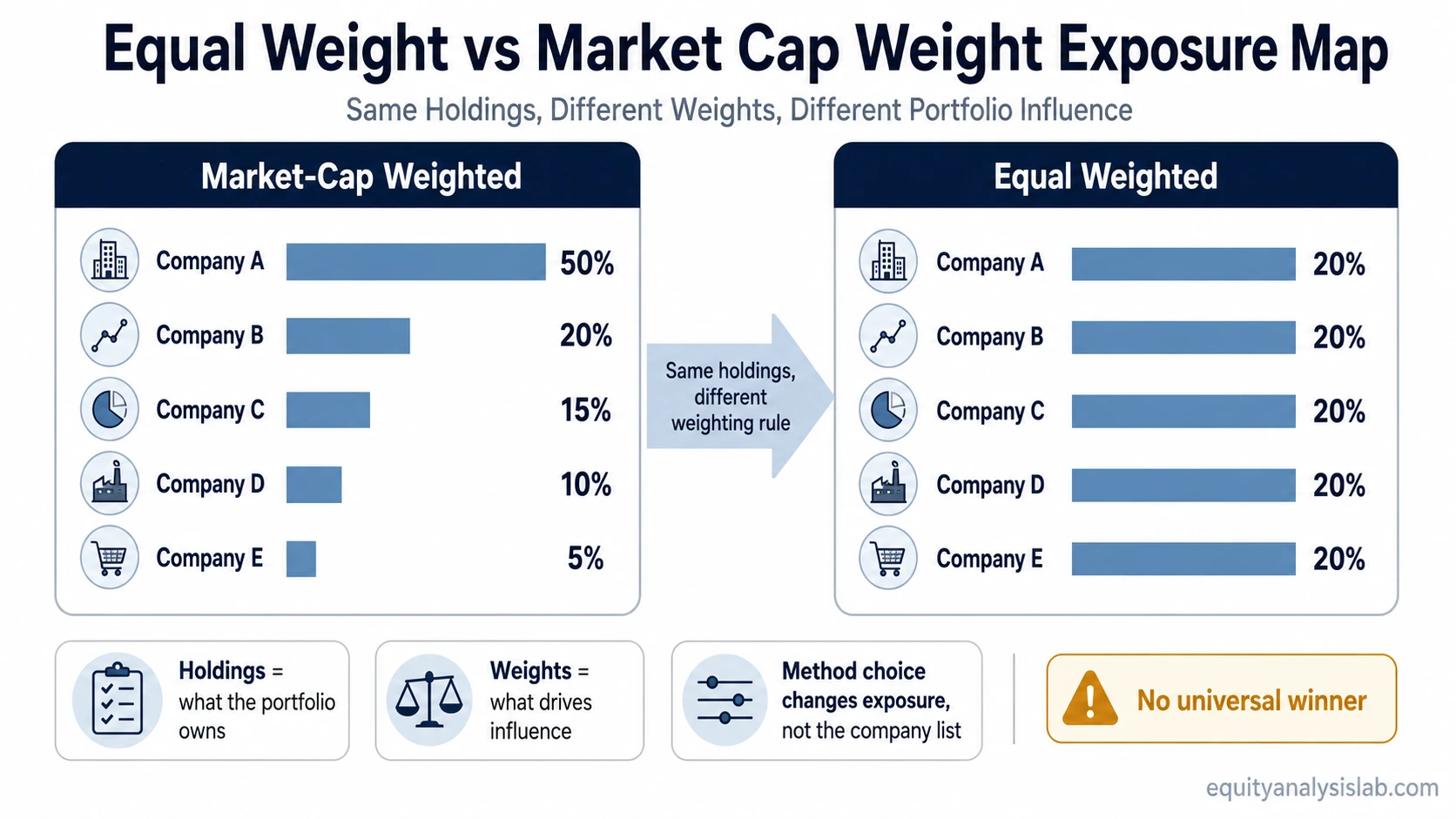

Same Holdings, Different Weights

The clearest way to compare equal weighted vs market cap weighted construction is to keep the holdings constant and change only the weighting rule.

Illustrative five-stock mini-index:

| Company | Illustrative market value | Market-cap weighted allocation | Equal weighted allocation |

|---|---|---|---|

| Company A | $500 billion | 50% | 20% |

| Company B | $200 billion | 20% | 20% |

| Company C | $150 billion | 15% | 20% |

| Company D | $100 billion | 10% | 20% |

| Company E | $50 billion | 5% | 20% |

Both versions own the same five companies. The market-cap weighted version depends heavily on Company A. The equal weighted version spreads starting influence evenly, which increases the role of Companies D and E compared with the cap-weighted version.

This example does not prove that one method is safer or more profitable. It shows that the weighting rule changes what the portfolio is actually exposed to, even before any discussion of returns.

The diagnostic separation is simple: holdings show what the portfolio owns, while weights show which holdings drive most of the portfolio’s behavior.

How Weighting Changes Concentration and Exposure

Weighting method changes portfolio concentration because it determines which holdings receive the most influence. Market-cap weighting can become concentrated when a small number of very large companies dominate the index. Equal weighting can reduce that specific top-heavy structure at each rebalance date, but it does not remove concentration risk entirely.

Equal weighting may shift exposure toward smaller companies, different sectors, or different factor profiles compared with the market-cap weighted version of the same universe. That shift can be meaningful even when the holding list is unchanged.

Important distinction: Equal weighting changes the source of exposure. It does not automatically make a portfolio safer, more diversified in every sense, or more suitable for every investor.

Rebalancing, Turnover, and Drift

Market-cap weighted portfolios are often described as self-adjusting because a company’s weight changes as its market value changes. If a company becomes larger relative to the index, its weight rises. If it becomes smaller, its weight falls.

Equal weighted portfolios require periodic rebalancing to restore equal starting weights. Between rebalance dates, winners can grow above their target weight and laggards can fall below it. The reset process brings the portfolio back to its equal-weight rule.

This creates a practical trade-off. Equal weighting may keep the portfolio from becoming dominated by the largest names at each rebalance date, but it can also increase turnover, transaction costs, and tax considerations depending on the vehicle and account structure.

When Each Weighting Method Can Behave Differently

The difference between equal weighted and market cap weighted construction becomes more visible when leadership is narrow. If a small group of large companies drives most of the market-cap weighted index, the cap-weighted version may move more with those leaders than with the average constituent.

Equal weighting can behave differently because every constituent starts with the same influence. If smaller or mid-sized constituents outperform, the equal weighted version may reflect that more strongly. If the largest companies dominate, the market-cap weighted version may reflect that leadership more strongly.

This distinction matters for asset allocation because the same label, such as a broad equity index, can hide different exposure profiles depending on how the index is weighted.

Common Mistakes When Comparing Weighting Methods

A common mistake is treating equal weight as automatically more diversified. Equal weight can reduce top-heavy single-name exposure, but it may increase exposure to smaller companies or sectors that are less dominant in a cap-weighted index.

Another mistake is treating market-cap weighting as automatically passive or neutral in every sense. Market-cap weighting follows market value, but that can still produce a portfolio that is heavily influenced by the largest companies or the strongest recent leadership groups.

The cleaner comparison is not “better versus worse.” It is: which weighting rule creates the exposure pattern the investor is trying to understand?

Related Concepts

Equal weight and market cap weight sit inside a broader portfolio construction process. Holding count, position size, sector exposure, index methodology, and rebalancing rules all affect how a portfolio behaves.

For an investor, the practical reading is to separate the holdings list from the weighting structure. A portfolio can look broad by name count while still being driven by a few large weights. Another portfolio can look more evenly spread while carrying different turnover, size, or sector exposure.

FAQ

Is equal weighted better than market cap weighted?

Equal weighted is not automatically better. It changes the exposure profile by giving every constituent the same starting weight, which can reduce top-heavy concentration but may increase turnover and smaller-company exposure.

Is market cap weighted more concentrated?

Market cap weighted portfolios can become more concentrated when the largest companies dominate the index by market value. The degree of concentration depends on the index, the size gap between constituents, and the current leadership structure.

Why does equal weight need rebalancing?

Equal weight needs rebalancing because price changes cause constituent weights to drift away from the same starting percentage. Rebalancing restores the equal-weight structure at the scheduled reset point.

Can equal weighted and market cap weighted portfolios hold the same stocks?

Yes. The holdings can be identical while the weights differ. The same companies can produce different portfolio behavior when one version weights by market value and the other gives each constituent the same starting weight.