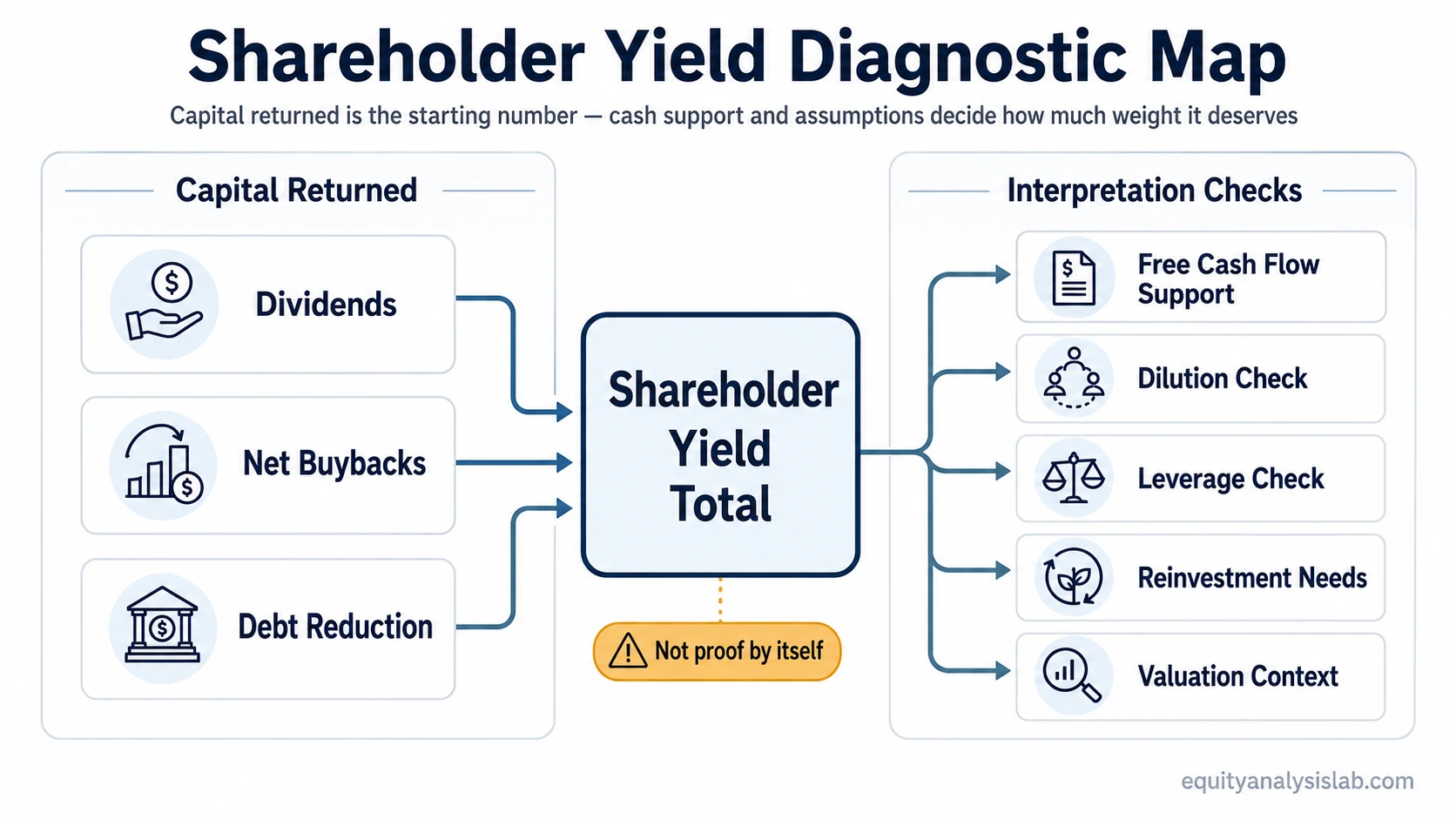

Shareholder yield is a capital-return metric that combines cash dividends, net share repurchases, and debt reduction relative to a company’s market value. It is broader than dividend yield because it captures more than the cash dividend alone, but the number only becomes useful after cash flow, dilution, leverage, reinvestment needs, and valuation context are checked.

Definition: Shareholder yield measures how much capital a company returns to shareholders through dividends, net buybacks, and net debt reduction. It is usually expressed as a percentage of market capitalization.

Key Points

- Shareholder yield is a company-level capital-return metric, not a dividend strategy by itself.

- The broader formula adds dividend yield, net buyback yield, and debt reduction yield.

- A high shareholder yield does not prove quality, undervaluation, or strong management.

- The same percentage can mean different things depending on free cash flow, share dilution, debt funding, reinvestment needs, and market capitalization.

What Is Shareholder Yield?

Shareholder yield estimates how much capital a company is returning to shareholders relative to the market value of its equity. It belongs inside capital-return analysis because it looks beyond the dividend line and includes other ways management may return capital.

The metric is a starting point for analysis. A company that pays dividends, reduces its share count, and lowers debt may show a strong shareholder-yield figure, but that figure still needs to be compared with the company’s cash generation and capital needs.

The better question is not only “how high is the yield?” It is whether the return of capital is sustainable, economically sensible, and supported by the business rather than by temporary financing choices or a shrinking investment opportunity set.

Shareholder Yield Formula

The broader version of shareholder yield adds three components: dividend yield, net buyback yield, and debt reduction yield.

Shareholder Yield = Dividend Yield + Net Buyback Yield + Debt Reduction Yield

A numerator-based version expresses the same idea relative to market capitalization:

Shareholder Yield = (Cash Dividends + Net Share Repurchases + Net Debt Reduction) ÷ Market Capitalization

Formula variants differ. Some analysts use only dividends and net buybacks, while others include net debt reduction because lowering debt can improve the equity holder’s claim on the enterprise by reducing creditor claims, although it is not the same as a direct cash distribution. The chosen version should be stated clearly before comparing companies.

Formula note: Net buybacks should account for share issuance. A company can spend heavily on repurchases while still failing to reduce the diluted share count if stock-based compensation or new issuance offsets the buyback.

What Shareholder Yield Includes

Shareholder yield combines several capital-return channels that can look similar in a headline number but mean different things in investor analysis.

| Component | What it measures | What to check before giving it weight |

|---|---|---|

| Dividends | Cash paid directly to shareholders. | Whether the payout is covered by earnings and free cash flow rather than funded by balance-sheet strain. |

| Net buybacks | Share repurchases after adjusting for share issuance. | Whether the diluted share count actually falls and whether repurchases were made at sensible valuation levels. This connects directly to buyback yield. |

| Debt reduction | Debt paydown that may increase the portion of enterprise value attributable to equity holders. | Whether the debt reduction is recurring, financially prudent, and not replacing higher-return reinvestment opportunities. |

The component mix matters. A 6% shareholder yield from sustainable free-cash-flow-funded dividends and real share-count reduction is different from a 6% yield created by debt-funded buybacks or a one-time balance-sheet adjustment.

How Investors Interpret Shareholder Yield

Shareholder yield helps separate companies that return capital through only dividends from companies that also use repurchases or balance-sheet repair. It can make capital allocation more visible, especially for companies that prefer buybacks over large recurring dividends.

The metric becomes more informative when it is compared over time. A company with stable shareholder yield, declining share count, manageable leverage, and strong free cash flow may be returning capital from a position of strength. A company with rising shareholder yield but weaker cash generation deserves more scrutiny.

Shareholder yield should not be treated as a quality score. It measures capital returned relative to market value. Quality depends on the source of the capital, the company’s future investment needs, the valuation at which buybacks occur, and whether balance-sheet flexibility remains intact.

Investor-use boundary: Shareholder yield can show how much capital is being returned, but it does not by itself show whether the capital return creates long-term value.

Why Shareholder Yield Can Mislead

A high shareholder yield can look attractive because it compresses several capital-return channels into one percentage. The risk is that the single number can hide weak assumptions underneath it.

Common interpretation risks:

- Weak free cash flow support: Capital returns deserve less weight when the business is not producing enough cash to support them.

- Debt-funded buybacks: Repurchases can increase shareholder yield while weakening the balance sheet if they rely too heavily on borrowing.

- Dilution offset: Buybacks may not improve per-share economics if stock issuance or compensation dilution offsets the repurchased shares.

- One-time debt reduction: A temporary debt paydown can lift the metric without creating a recurring capital-return pattern.

- Market-cap sensitivity: A falling share price can mechanically raise the yield denominator effect, even if the business outlook is deteriorating.

- Reinvestment tradeoff: Returning cash can be less attractive if the company still has high-return internal investment opportunities.

- Sector differences: Capital intensity, cyclicality, regulation, and growth runway can make the same shareholder-yield percentage mean different things across industries.

Payout support should be checked separately. A company may show a strong shareholder yield while its dividend is becoming harder to sustain, which is why the dividend coverage ratio remains a separate test rather than a detail inside shareholder yield.

Shareholder Yield Example

Assume a hypothetical company has a market capitalization of $10 billion. During the year, it pays $250 million in dividends, spends $500 million on share repurchases, issues $100 million worth of new shares through compensation and other issuance, and reduces net debt by $150 million.

| Item | Hypothetical amount | Yield contribution |

|---|---|---|

| Cash dividends | $250 million | 2.5% |

| Gross repurchases | $500 million | 5.0% |

| Share issuance offset | -$100 million | -1.0% |

| Net buybacks | $400 million | 4.0% |

| Net debt reduction | $150 million | 1.5% |

| Total shareholder yield | $800 million | 8.0% |

In this example, the 8.0% shareholder yield does not automatically mean the company is attractive. The number needs context: whether the $800 million capital return was supported by free cash flow, whether the repurchases reduced the diluted share count, whether debt reduction was part of a durable balance-sheet plan, and whether the company still had enough capital for reinvestment.

How Assumptions Change Shareholder Yield

The same shareholder-yield percentage can point to different conclusions when the assumptions behind it change.

| Surface result | Assumption behind the number | Interpretation effect |

|---|---|---|

| High shareholder yield | Free cash flow comfortably covers dividends, buybacks, and debt paydown. | Stronger as a capital-allocation signal, though valuation and reinvestment needs still matter. |

| High shareholder yield | Buybacks are funded with rising leverage. | Weaker signal because capital return may be borrowing-supported rather than business-supported. |

| High buyback component | Diluted shares outstanding do not fall. | Weaker signal because repurchases may be offset by issuance or stock-based compensation. |

| High debt reduction component | Debt paydown is a one-time event after asset sales or temporary cash release. | Less useful as a recurring capital-return indicator. |

| Rising shareholder yield | Market capitalization falls faster than capital returns. | Potentially misleading because the yield may rise as business risk increases. |

| Moderate shareholder yield | The company retains capital for high-return reinvestment. | Not automatically weak; lower capital return can be rational if reinvestment opportunities are strong. |

This is why shareholder yield works better as an assumption check than as a ranking shortcut. The investor still has to ask what funded the capital return, whether per-share value improved, and what future cash needs could change the picture.

Shareholder Yield vs Dividend Yield

Dividend yield measures annual dividends relative to share price or market value. Shareholder yield is broader because it adds net share repurchases and, in some versions, debt reduction.

Dividend yield: focuses on direct cash distributions to shareholders.

Shareholder yield: focuses on total capital returned through dividends, net buybacks, and debt reduction.

The distinction matters because a company with a low dividend yield may still return significant capital through buybacks. The reverse can also be true: a company with a high dividend yield may have a weaker shareholder-yield profile if it issues shares, carries rising debt, or lacks cash-flow support.

Related Capital Return Metrics

Shareholder yield sits inside a wider capital-return toolkit. It should be read beside the metrics that isolate each component rather than replacing them.

| Related metric or concept | How it differs from shareholder yield |

|---|---|

| Dividend yield | Looks only at cash dividends relative to price or market value. |

| Buyback yield | Focuses on the net repurchase component instead of total capital returned. |

| Dividend coverage ratio | Tests whether dividend payments are supported by earnings or cash flow. |

| Dividend reinvestment | Describes what an investor does after receiving dividends, not how much capital the company returns. |

Used carefully, shareholder yield can connect dividend policy, repurchase activity, and balance-sheet decisions into one capital-return view. Used carelessly, it can hide the quality of those decisions behind a clean-looking percentage.

FAQ

Can shareholder yield be negative?

Yes. Shareholder yield can be negative if share issuance, rising debt, or other capital-structure changes more than offset dividends and buybacks. A negative result does not automatically make a company poor quality, but it means the investor should check why capital is moving away from shareholders on a net basis.

When can a high shareholder yield be weak?

A high shareholder yield can be weak when the capital return is funded by borrowing, offset by dilution, unsupported by free cash flow, or caused mainly by a falling market capitalization. The number should be treated as a starting point for analysis, not as proof that capital allocation is strong.

Why include debt reduction in shareholder yield?

Some versions include debt reduction because paying down debt can increase the equity holder’s claim on enterprise value. The limitation is that debt paydown is not the same as a direct cash distribution, so the formula version should be stated clearly before comparing companies.