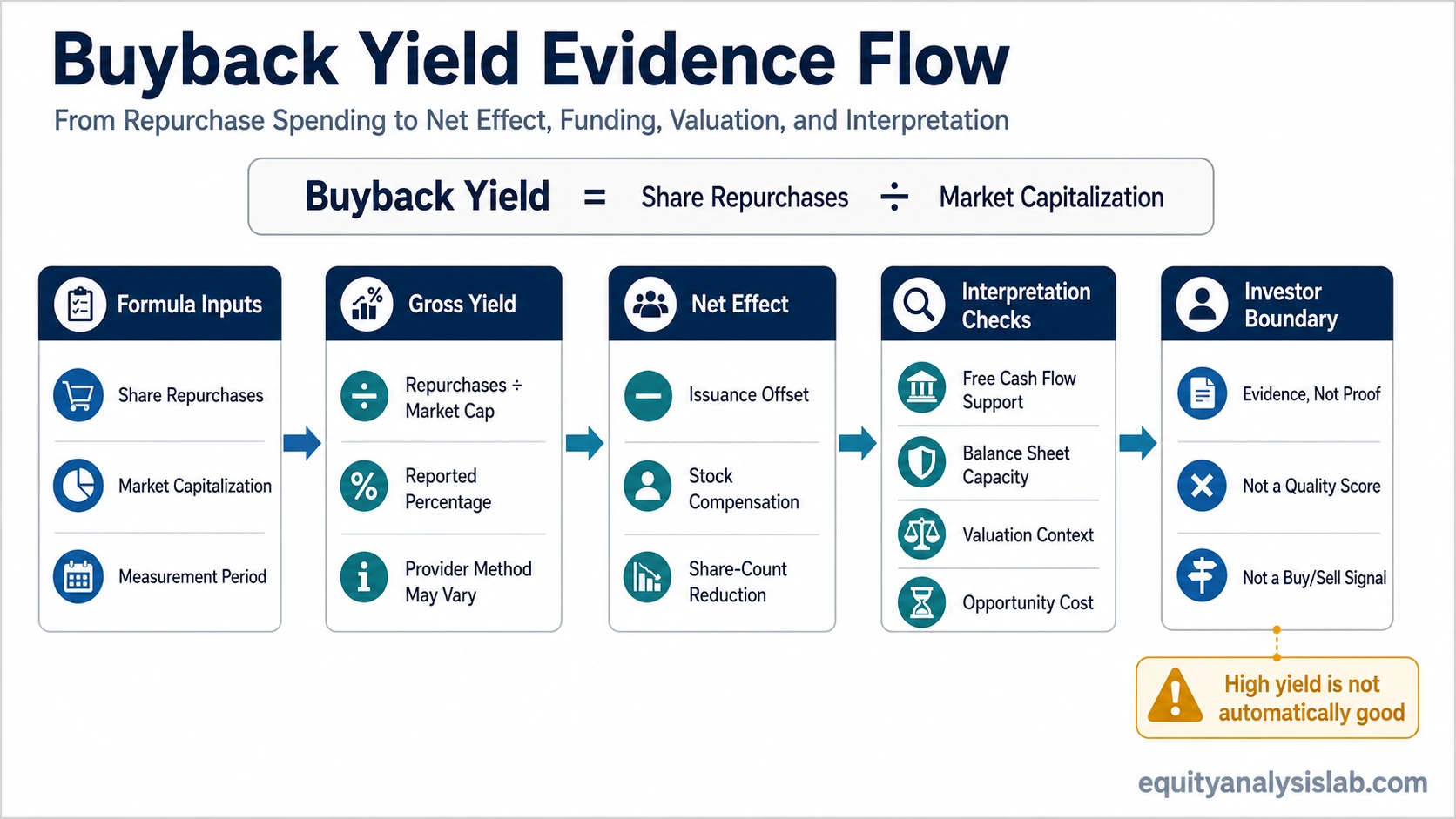

Buyback yield measures share repurchases relative to market value, but the number is only useful when the repurchases are sustainable, reduce share count meaningfully, and make sense against valuation and cash-flow context.

Definition: Buyback yield is a capital-return metric that compares a company’s share repurchases with its market capitalization. It helps investors see how much of the company’s market value was effectively spent on buying back stock during a period.

The metric belongs in company analysis because buybacks can change the ownership claim attached to each remaining share. A buyback program that reduces diluted share count can increase each remaining share’s claim on future earnings and cash flow. A buyback program that mostly offsets stock compensation may look large in dollar terms while doing little for continuing shareholders.

That distinction is why buyback yield should not be read as a standalone quality score. The same percentage can reflect disciplined capital allocation, routine compensation offset, weak reinvestment opportunities, debt-funded financial engineering, or repurchases made at unattractive prices.

Key Points

- Buyback yield compares share repurchases with market value.

- The formula can use gross buybacks or net buybacks depending on the data source.

- A high buyback yield is not automatically good.

- Repurchases matter more when they reduce share count without weakening the balance sheet.

- Dividend yield and shareholder yield measure different capital-return ideas.

What Buyback Yield Means

Buyback yield shows the scale of share repurchases relative to the company’s market capitalization. If a company has a market value of $10 billion and repurchases $500 million of its own shares over a year, the gross buyback yield is 5%.

The interpretation depends on what those repurchases actually do. A company can spend cash on buybacks and still fail to reduce the diluted share count if stock-based compensation, option issuance, acquisitions, or other dilution offsets the repurchases. In that case, the headline buyback yield may overstate the economic benefit to continuing shareholders.

Buyback yield also does not explain whether the repurchase price was sensible. Buying back shares below a reasonable estimate of intrinsic value can be different from buying back shares at a stretched valuation while underinvesting in the business or increasing leverage.

Buyback Yield Formula

The basic buyback yield formula is:

Buyback yield = Share repurchases ÷ Market capitalization

Some sources express the result as a percentage:

Buyback yield (%) = (Share repurchases ÷ Market capitalization) × 100

The numerator is usually the amount spent on share repurchases during a period, often one fiscal year or the trailing twelve months. The denominator is usually market capitalization, but timing can vary. A data provider may use current market capitalization, average market capitalization, beginning-period market capitalization, or another internal convention.

| Formula input | What it represents | Why it can affect interpretation |

|---|---|---|

| Share repurchases | Cash spent buying back stock during the measurement period. | Gross spending may not equal actual reduction in shares outstanding. |

| Net buybacks | Repurchases adjusted for issuance or dilution. | Can better reflect whether continuing shareholders gained a larger ownership claim. |

| Market capitalization | Market value of the company’s equity. | Different timing conventions can change the reported yield. |

| Measurement period | The time window used for buybacks and market value. | Annual, trailing twelve-month, or fiscal-period calculations may not match exactly. |

Because data sources can define inputs differently, buyback yield should be checked against the underlying share-count trend, cash-flow statement, and capital allocation notes instead of treated as a uniform number across platforms.

Gross vs Net Buyback Yield

Gross buyback yield uses the total amount spent on repurchases. Net buyback yield tries to adjust for share issuance, stock compensation, or dilution that offsets the buyback. The net version is often more useful when the goal is to understand whether existing shareholders actually own more of the company after the repurchase program.

| Measure | Basic idea | Main limitation |

|---|---|---|

| Gross buyback yield | Repurchase spending divided by market capitalization. | Can look strong even when share count barely falls. |

| Net buyback yield | Repurchases adjusted for issuance or dilution. | Requires cleaner data and may vary by provider methodology. |

| Share-count reduction | Actual change in shares outstanding or diluted shares. | Can be affected by timing, acquisitions, option exercises, and reporting conventions. |

A company that spends heavily on repurchases while issuing a large amount of stock compensation may produce a positive gross buyback yield but a weak net ownership effect. That does not automatically make the buyback program bad, but it changes what the metric can support.

Buyback Yield Calculation Example

Consider a hypothetical company with a market capitalization of $20 billion. During the last fiscal year, it spent $1 billion repurchasing shares.

Example calculation: $1 billion ÷ $20 billion = 0.05, or 5% gross buyback yield.

If the company also issued shares through stock compensation and other plans, an investor may adjust the gross repurchase amount to estimate the net effect. In a simplified dollar-based proxy, $400 million of offsetting issuance would reduce the net repurchase effect to about $600 million, making the net buyback yield 3%. A share-count-based method can produce a different result.

| Calculation version | Input used | Result | Interpretation |

|---|---|---|---|

| Gross buyback yield | $1.0 billion repurchased ÷ $20 billion market cap | 5% | Shows repurchase spending relative to market value. |

| Net buyback yield | $600 million net repurchase effect ÷ $20 billion market cap | 3% | Better reflects the effect after dilution offset. |

The example is deliberately simple. Real filings can require more careful reading because repurchases, share issuance, weighted average diluted shares, and period-end shares may not move in the same way.

How Investors Interpret Buyback Yield

Buyback yield can help investors understand how aggressively a company is returning capital through repurchases. It is most useful when paired with free cash flow, balance sheet capacity, valuation, and actual share-count movement.

A higher figure can be constructive when the company is producing durable cash flow, maintaining a reasonable balance sheet, and buying shares at prices that do not look excessive relative to business value. The same figure is weaker when repurchases are funded by rising debt, offset by dilution, or made while the core business needs capital elsewhere.

Buyback yield also interacts with earnings per share, but not mechanically. Reducing the share count can support EPS because the same earnings are spread across fewer shares. That effect can disappear if earnings quality weakens, free cash flow does not support the spending, dilution offsets the repurchases, or the market assigns a lower valuation multiple.

Assumptions That Can Change the Meaning

The strongest use of buyback yield is not the raw percentage. It is the comparison between the reported figure and the assumptions behind it.

| Assumption to check | Stronger interpretation | Weaker interpretation |

|---|---|---|

| Gross vs net buybacks | Repurchases reduce the diluted share count meaningfully. | Gross spending is mostly offset by stock issuance or compensation. |

| Free cash flow support | Buybacks are funded from recurring cash generation. | Repurchases exceed sustainable cash flow or depend on asset sales. |

| Balance sheet capacity | Leverage remains manageable after repurchases. | Debt rises mainly to support buybacks while flexibility declines. |

| Valuation context | Repurchases occur at prices that appear reasonable relative to business value. | Management buys heavily when the stock already reflects aggressive expectations. |

| Opportunity cost | Repurchases do not crowd out high-return reinvestment needs. | Buybacks replace necessary investment in the business. |

| Data-provider method | The calculation method matches the investor’s intended question. | The reported figure hides timing, issuance, or denominator differences. |

This sensitivity layer prevents the metric from becoming a shortcut. Buyback yield can be a useful capital-return clue, but it still needs evidence from the cash-flow statement, share-count history, and management’s broader capital allocation choices.

Why Buyback Yield Can Be Misleading

Buyback yield can mislead when it is treated as proof that management is creating value. A company can repurchase shares for reasons that are neutral or even harmful to long-term owners.

Key limitation: Buyback yield measures repurchase scale. It does not prove repurchase quality.

Several conditions can weaken the signal:

- Stock compensation offset: Repurchases may mainly absorb new shares issued to employees or executives.

- Debt-funded repurchases: Borrowing to buy back stock can reduce future flexibility if leverage becomes stretched.

- Weak free cash flow: Repurchases are less durable when operating cash generation cannot support them.

- Overvalued repurchases: Buying back shares at inflated prices can destroy value even if the buyback yield looks high.

- Capital allocation trade-off: Repurchases may be less attractive when the business has better reinvestment opportunities.

- Timing mismatch: A market cap denominator taken at one date can distort the comparison with buybacks made across a full year.

Debt-funded buybacks are not automatically bad. The risk depends on leverage, interest coverage, business stability, maturity schedule, and whether the repurchased shares were attractively priced. The metric should start that analysis, not finish it.

Buyback Yield vs Dividend Yield and Shareholder Yield

Buyback yield is one capital-return measure, but it is not the same as a dividend measure or a total shareholder-return measure. The differences matter because each metric answers a different question.

| Metric | What it measures | Best use |

|---|---|---|

| Buyback yield | Share repurchases relative to market capitalization. | Evaluating the scale and quality of repurchases. |

| Cash dividend yield | Cash dividends relative to share price. | Comparing current cash income relative to market price. |

| A broader capital-return measure | Often combines dividends, net buybacks, and sometimes debt reduction. | Viewing capital returns beyond repurchases alone. |

Dividend-focused analysis also needs sustainability checks. A company can have a high dividend yield while the payout is under pressure, which is why the dividend coverage ratio belongs in a different part of the capital-return review.

Dividend reinvesting is another separate decision. Reinvested dividends describe what the investor does with distributed cash, while buyback yield describes what the company does with capital at the corporate level.

Common Mistakes With Buyback Yield

The most common mistake is treating a high buyback yield as automatically positive. The better question is whether the repurchases improved the ownership economics of the remaining shares without weakening the company’s financial position.

| Mistake | Why it matters | Better check |

|---|---|---|

| Assuming higher is always better | A large repurchase can be poorly timed or debt-funded. | Compare buybacks with free cash flow, leverage, and valuation. |

| Ignoring dilution | Repurchases may only offset stock issuance. | Review diluted share count over several periods. |

| Using one provider’s formula as universal | Data sources can use different inputs and timing conventions. | Check numerator, denominator, and measurement period. |

| Confusing buyback yield with shareholder yield | Buyback yield excludes some broader capital-return components. | Separate repurchases, dividends, and debt reduction. |

| Ignoring business reinvestment needs | Buybacks can crowd out higher-return internal investment. | Assess growth opportunities and capital allocation trade-offs. |

A cleaner interpretation asks whether repurchases are funded by real cash generation, reduce the share base, fit the company’s valuation, and leave enough capacity for debt obligations and reinvestment.

Related Capital-Return Concepts

Buyback yield works best as part of a wider capital-return review. Dividend yield focuses on cash distributions to shareholders. Shareholder yield expands the frame to combine multiple forms of capital return. Dividend coverage focuses on whether dividend payments are supported by earnings or cash flow. Dividend reinvestment describes how investors may redeploy dividends after receiving them.

Keeping those concepts separate prevents the buyback yield figure from carrying too much meaning. Repurchases are one part of capital allocation, not a complete investment case. The separation matters because buyback yield answers one narrow question: how large repurchases are relative to equity market value, not whether the full capital-return policy is attractive.

FAQ

What is buyback yield?

Buyback yield is a capital-return metric that compares a company’s share repurchases with its market capitalization. It shows how large repurchases are relative to the company’s market value.

Is a high buyback yield always good?

No. A high buyback yield is more useful when repurchases are supported by free cash flow, reduce share count, do not strain the balance sheet, and occur at sensible valuations.

Why can gross buyback yield differ from net buyback yield?

Gross buyback yield uses total repurchase spending. Net buyback yield adjusts for share issuance, stock compensation, or dilution that can offset the effect of repurchases. Data providers may calculate the adjustment differently.

How is buyback yield different from dividend yield and shareholder yield?

Buyback yield measures repurchases relative to market value. Dividend yield measures cash dividends relative to share price. Shareholder yield is broader because it can combine dividends, net buybacks, and sometimes debt reduction.