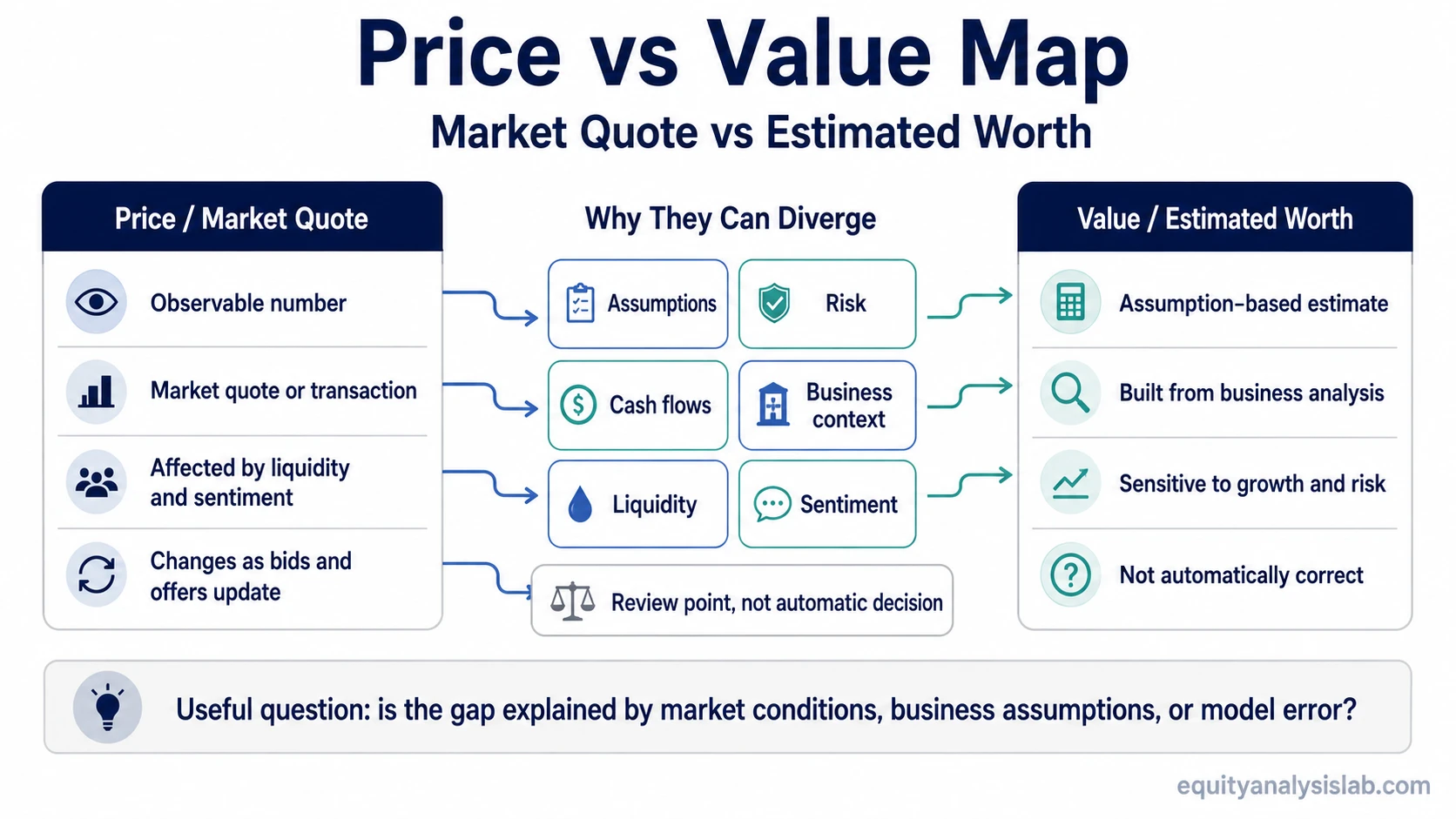

Price and value can refer to the same company, but they answer different investor questions: price shows what the market is quoting now, while value estimates what the business or security may be worth under a specific set of assumptions.

Price vs value, in investing, separates an observable market number from an estimated worth figure. Price is visible in a quote, transaction, or market capitalization figure. Value is judged through future cash flows, asset quality, risk, growth, competitive position, and the assumptions used to interpret those inputs.

The confusion comes from the fact that both terms can point to the same stock at the same moment. A share may trade at $40, while one investor estimates its value at $48 and another estimates it at $34. The price is shared by the market. The value estimate depends on the model, assumptions, and required margin for error.

Price vs Value: Key Differences

The most useful distinction is not linguistic. Price and value sit on different measurement bases. Price is observed. Value is estimated.

| Criterion | Price | Value |

|---|---|---|

| Question answered | What is the market quoting or what was paid? | What may the asset be worth under a defined assumption set? |

| Main source | Market quote, trade, offer, or transaction data. | Valuation work, business analysis, future expectations, and risk judgment. |

| Timing | Current or transaction-specific. | Forward-looking and assumption-sensitive. |

| Inputs | Supply, demand, liquidity, sentiment, order flow, and transaction conditions. | Cash flow, earnings quality, growth, risk, capital structure, competitive position, and required return. |

| Sensitivity | Can change quickly as buyers and sellers update bids and offers. | Can change when the underlying assumptions or business outlook change. |

| Investor use | Shows the current market reference point for investor review. | Provides a reference point for judging whether the quote looks reasonable. |

| Common mistake | Assuming a lower price automatically means better opportunity. | Assuming a model estimate is automatically correct because it looks precise. |

Why Price and Value Diverge

Price and value diverge because markets and valuation models respond to different forces. The quoted price reflects the point where buyers and sellers are currently willing to transact. That point can be shaped by liquidity, sentiment, forced selling, short-term news, positioning, and the availability of comparable alternatives.

Value is slower and more assumption-driven. An investor estimating intrinsic value is asking what the company may be worth based on future benefits and risk, not only what the quote shows today.

This gap does not automatically mean the market is wrong. Sometimes price moves before the valuation case is visible in reported numbers. Sometimes a model lags reality because its assumptions are stale. The useful question is not whether price or value is always superior. The useful question is whether the difference is explained by a real assumption gap, a temporary market condition, or a weak valuation estimate.

Same Company, Different Reading

Assume a hypothetical company trades at $40 per share. An investor estimates that the business may be worth $46 per share if revenue growth remains steady, margins hold, and the discount rate used in the model stays unchanged. Under a more cautious assumption set, with slower growth and lower margins, the same investor may estimate value closer to $35 per share.

The $40 price is observable. The $46 and $35 value estimates are not facts. They are outputs from different assumptions.

The same company can therefore look inexpensive, fairly priced, or expensive depending on the valuation case being tested. That is why price comparison alone is not enough. A quote only becomes meaningful when it is compared with a well-defined estimate of business value, uncertainty, and risk.

For public companies, market capitalization extends the quoted share price into a total public equity market value. That still does not make it the same thing as a full valuation estimate.

Common Confusion Trap

A lower price is not automatically better value. A stock can fall because the business outlook has deteriorated, because dilution risk has increased, because expected cash flows are weaker, or because the market is demanding a higher return for the same uncertainty.

The opposite trap is treating a model as truth. A valuation model can produce a clean-looking value estimate while relying on fragile inputs. Growth, margin, reinvestment, discount rate, debt, and diluted share count can all change the result. A weak model can be less useful than the market quote it tries to challenge.

The distinction also depends on the value basis being used. A discussion of the whole firm may use an enterprise value framework, while a common-share estimate focuses on what belongs to equity holders after the relevant claims and share-count assumptions are considered.

Market Price vs Fair Value

Market price is the number available now. Fair value, in this investor valuation context, means an estimate of what the security or business may be worth under a more balanced or internally consistent set of assumptions. It should not be treated as the same thing as a formal accounting fair value measurement unless that accounting context is explicitly being discussed.

For an investor, fair value is most useful when the assumptions are explicit. A fair value estimate without stated growth, cash-flow, risk, capital-structure, and share-count assumptions is difficult to test. A price without valuation context is also incomplete because it shows where the market is, not whether the quote is reasonable.

When the analysis is focused on common shareholders, the relevant estimate may be described as the value of equity or common equity value. That is a narrower question than the value of the entire operating business and should not be mixed casually with firm-level valuation measures.

Related Valuation Concepts

Price vs value is a starting distinction. The deeper work is deciding which value basis is being estimated and which assumptions control the estimate.

The clean measurement sequence begins with share price, then extends into market capitalization when the quoted share price is multiplied across the public equity base.

From there, enterprise value helps frame the value of the operating business before the analysis narrows to debt, cash, and shareholder-level claims.

A shareholder-focused estimate may then move toward the value attributable to common equity, while intrinsic value focuses on estimated worth under business and risk assumptions.

These concepts should not be blended into one number. A cleaner comparison starts by naming the measurement basis, then asking whether the current quote is being compared with the right estimate.

FAQ

Is price the same as value?

No. Price is the observable quote or transaction number. Value is an estimate of worth based on assumptions about future benefits, risk, and context.

Can price and value be equal?

Yes. They can be close or even effectively equal if the market quote is consistent with a reasonable valuation estimate. The problem is that equality cannot be assumed without checking the assumptions behind the estimate.

Does a lower price always mean better value?

No. A lower price can reflect weaker fundamentals, higher risk, worse expectations, dilution, or changed market conditions. Price only becomes meaningful when compared with a defensible value estimate.

Why do investors compare price and value?

Investors compare price and value to judge whether the market quote appears reasonable relative to the estimated worth of the business or security. The comparison is not a prediction and does not remove uncertainty.