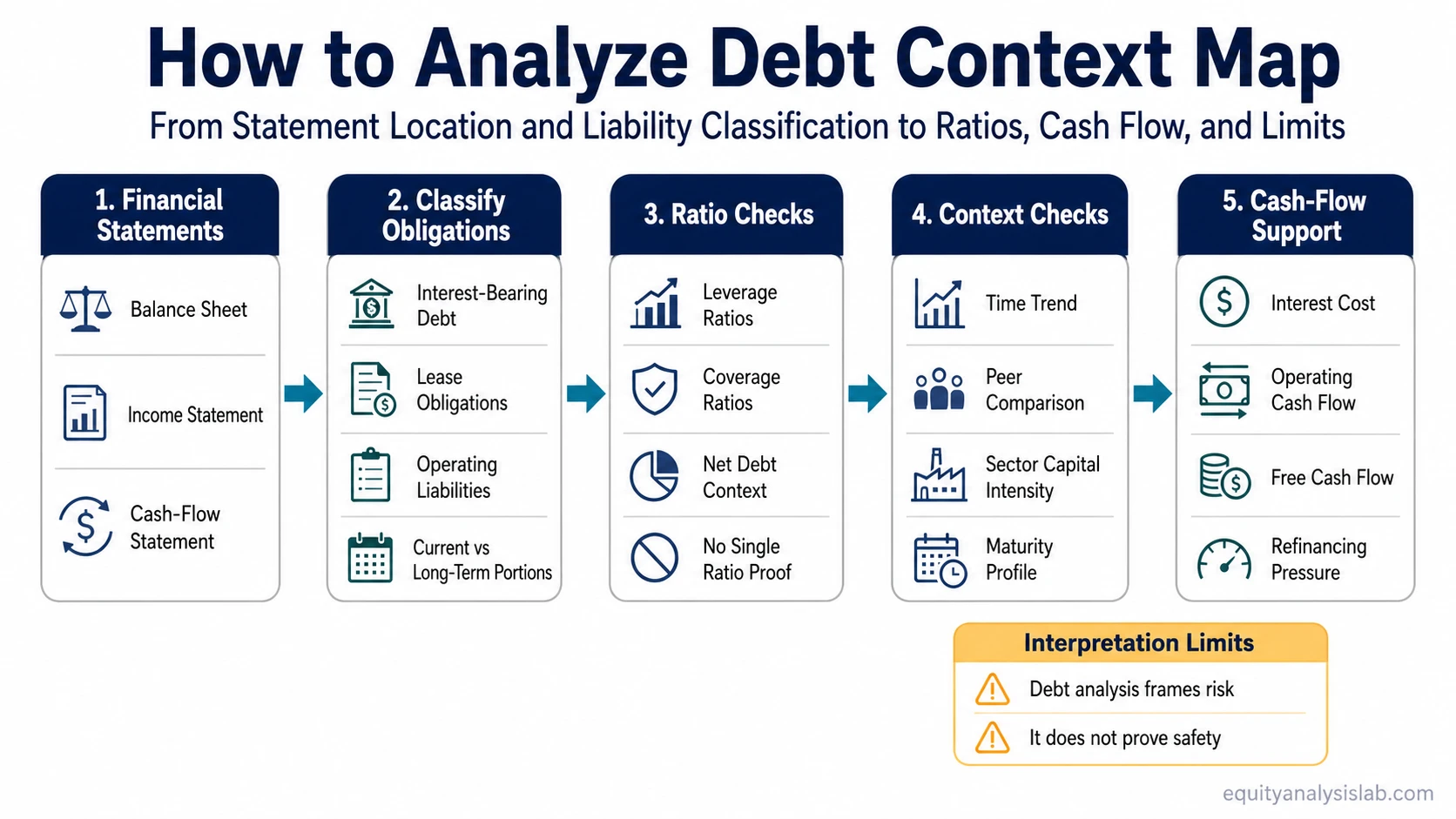

To analyze debt, start by finding where the company’s debt appears in the financial statements, then test the amount, cost, maturity, and cash-flow support behind it.

A single debt ratio can be useful, but it is not enough. Debt analysis becomes more reliable when the ratio is checked against liabilities classification, interest expense, period trends, sector context, and cash generation.

Debt Analysis Checks That Matter

- Locate debt in the statements before interpreting any ratio.

- Separate interest-bearing debt from operating liabilities.

- Use ratios to frame leverage, not to prove safety or risk by themselves.

- Compare debt across time, peers, maturity profile, and sector capital needs.

- Check whether cash flow can support interest, refinancing, and repayment pressure.

Start With Where Debt Appears

Debt analysis starts with the balance sheet, because that is where investors can usually see borrowings, lease obligations, current portions of long-term debt, and other liability categories that shape leverage interpretation.

The income statement adds a second layer by showing interest expense. This helps connect the debt balance to the cost of carrying it. A company can have manageable debt principal on the surface but still face pressure if interest expense rises faster than operating profit.

The cash-flow record adds the third layer. Operating cash flow, capital expenditures, debt issuance, and debt repayment can show whether the debt burden is being supported by recurring cash generation or mainly pushed forward through refinancing.

| Statement area | What to look for | Why it changes the debt read |

|---|---|---|

| Balance sheet | Short-term debt, long-term debt, lease liabilities, total liabilities, cash | Shows the scale and classification of obligations at a point in time |

| Income statement | Interest expense, operating income, earnings volatility | Shows whether profit can absorb the cost of debt |

| Cash-flow statement | Operating cash flow, capital expenditures, financing cash flows, repayments | Shows whether the company is generating cash or relying on external financing |

Do Not Treat All Liabilities as Debt

Debt usually refers to interest-bearing obligations, but company filings also include operating liabilities. Accounts payable, accrued expenses, deferred revenue, provisions, and some lease liabilities can have different economic meanings from bank loans or bonds.

The distinction matters because total liabilities can overstate or understate the specific financing burden the investor is trying to understand. A retailer with large accounts payable may look liability-heavy, while a company with long-term bonds may carry a clearer financing obligation even if reported liabilities look simpler.

| Weak approach | Better debt-analysis approach |

|---|---|

| Read one debt ratio as proof of risk | Classify the debt, compare periods, and check cash-flow support |

| Treat all liabilities as debt | Separate interest-bearing debt from operating liabilities |

| Assume high debt is always bad | Compare debt with sector norms, cash-flow stability, maturity, and cost |

| Assume low debt is always safe | Check asset quality, business durability, cash conversion, and financing needs |

Use Debt Ratios as Interpretation Tools

Debt ratios are useful because they compress complex statement data into comparable checks. They become weaker when the formula is treated as the conclusion. The same ratio can mean different things for a regulated utility, a software company, a cyclical manufacturer, or a commodity producer.

The definitions also matter. Some versions of debt ratio use total liabilities, while others focus only on interest-bearing debt. The numerator should be clear before the result is compared across companies.

| Check | What it compares | Useful question | Main limit |

|---|---|---|---|

| Debt ratio | Debt or liabilities vs assets | How much of the asset base is financed by obligations? | Definitions vary; not all liabilities are interest-bearing debt |

| Debt-to-equity | Debt or liabilities vs equity | How leveraged is the capital structure? | Equity can be distorted by buybacks, losses, or accounting effects |

| Interest coverage | EBIT or operating income vs interest expense | Can operating profit cover interest cost? | Does not show principal maturity or refinancing risk |

| Net debt | Debt minus cash and equivalents | How much debt remains after cash is considered? | Cash may be restricted or needed for operations |

| FCF-to-debt | Free cash flow vs total debt | Is cash generation meaningful relative to debt burden? | Free cash flow can be cyclical, temporarily elevated, or temporarily weak |

Compare Debt Across Time and Peers

A debt figure is more useful when it is compared with the company’s own history. Rising debt may be reasonable if it funds productive assets and cash flow follows. It is more concerning when borrowings rise while margins, operating cash flow, or asset quality weaken.

Peer comparison adds context, but it should stay inside the right sector or business model. Capital-intensive companies often use more debt than asset-light companies. Stable contracted revenue may support a different debt profile from volatile earnings, but that does not remove refinancing, interest-rate, or execution risk.

Maturity timing is part of the comparison. Debt due soon can create pressure even when the long-term ratio looks acceptable. Long maturities can reduce near-term pressure, but only if interest cost and operating cash generation remain manageable.

Check Whether Cash Flow Supports the Debt

The strongest debt read connects the balance sheet to cash generation. A company that reports profit but repeatedly fails to convert earnings into cash may have less flexibility to service debt, fund capital expenditures, or reduce borrowings.

The statement of cash flows helps separate operating cash generation from financing activity. If debt repayment is funded by new borrowing rather than operating cash, the investor should treat the debt profile differently from a company that can reduce debt from internally generated cash.

Cash-flow support should also be viewed after capital expenditures. A business can show strong operating cash flow and still have limited debt flexibility if most of that cash must be reinvested just to maintain operations. That is why cash generation after reinvestment is often a more useful debt-service lens than profit alone.

When debt service is being evaluated, the key question is not only whether the company has cash today. It is whether recurring cash after reinvestment can support interest, maturities, and refinancing needs without weakening the business. That makes cash generation after capital spending an important part of the debt analysis.

Hypothetical Debt Analysis Example

Consider two hypothetical companies. Company A has a moderate debt ratio, but interest expense is rising, operating cash flow is falling, and most maturities arrive within the next two years. Company B has a higher debt ratio, but cash flow is steadier, maturities are spread out, and interest coverage has not deteriorated.

The example does not prove that Company B is better or safer. It shows why the debt ratio is only the first layer. A useful debt read compares the amount of debt with cost, timing, business stability, refinancing pressure, and cash-flow support before drawing an investor conclusion.

Common Debt Analysis Mistakes

Using one ratio as the answer: A ratio can highlight leverage, but it cannot show maturity timing, cash restrictions, refinancing access, or business cyclicality by itself.

Mixing debt with all liabilities: Total liabilities may include operating items that do not behave like borrowings. The analysis should identify what kind of obligation is being measured.

Treating high debt as automatically bad: A higher debt load may be more manageable when cash flows are durable, maturities are long, and interest cost is controlled.

Accepting the story before checking cash: A low headline ratio or convincing growth narrative can still be weak if operating cash flow and free cash flow do not support interest, reinvestment, and repayment needs.

Treating low debt as automatically safe: A low-debt company can still be risky if cash conversion is weak, assets are poor quality, or the business requires heavy reinvestment.

Ignoring the cost and timing of debt: Principal amount matters, but interest expense and maturity schedule often determine when pressure becomes visible.

What Debt Analysis Cannot Prove

Debt analysis cannot prove that a company is undervalued, high quality, or likely to deliver a specific return. It can only show how obligations, financing cost, cash generation, and refinancing pressure affect the investor’s interpretation of the company.

It also cannot replace a full business review. A debt profile that looks manageable today can weaken if earnings fall, rates rise, capital needs increase, or access to refinancing changes. The conclusion should remain conditional, not absolute.

Where Debt Analysis Fits in a Financial Statement Review

Debt analysis works best as part of a broader financial statement review. It starts with statement location, then moves through obligation type, ratio framing, peer comparison, and cash-flow confirmation.

The useful sequence is: identify the obligation, measure the burden, test the cost, compare the context, and then check whether recurring cash generation can support the conclusion. That sequence keeps debt analysis from becoming a one-ratio shortcut.

FAQ

What is the first step in analyzing company debt?

The first step is to locate debt and related liabilities in the financial statements, then identify whether the obligations are interest-bearing debt, operating liabilities, leases, or other items that need different interpretation.

Is a high debt ratio always bad?

No. A high debt ratio can be a risk, but its meaning depends on cash-flow stability, interest cost, maturity timing, sector norms, asset quality, and access to refinancing.

Why is cash flow important in debt analysis?

Cash flow helps show whether the company can support interest, reinvestment, repayment, or refinancing needs from recurring operations rather than relying only on new financing.

Can debt analysis show whether a stock is attractive?

No. Debt analysis can clarify financial risk and flexibility, but it does not determine valuation, expected return, price targets, or investment suitability by itself.