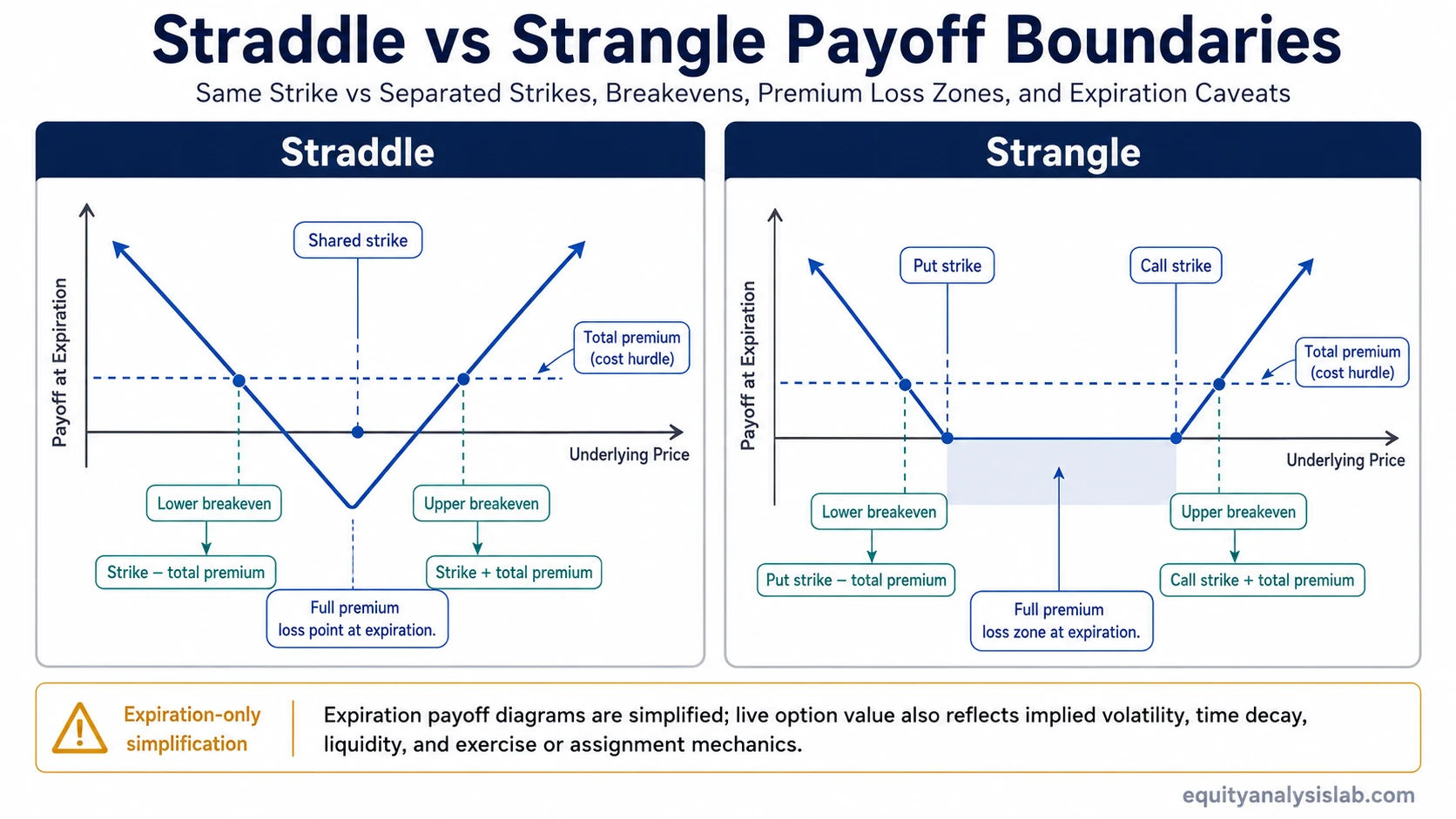

A straddle and a strangle both combine a call and a put with the same expiration, but they use different strike logic. A straddle places both options at the same strike, while a strangle separates the call and put strikes, which changes premium, breakevens, payoff boundaries, and the movement needed before expiration.

Direct answer: A straddle uses one call and one put at the same strike and expiration. A strangle uses one call and one put with different strikes and the same expiration. In long debit form, both structures pay an upfront premium, but the strike relationship changes where the position begins to move beyond its total premium cost.

What Is the Difference Between a Straddle and a Strangle?

The core difference is the strike relationship. In a straddle, the call and put share one strike. In a strangle, the call strike is above the put strike, so the structure has a wider zone between the two options before either side is meaningfully in the money.

That difference affects the cost hurdle. In many standard long/debit examples, a long straddle often has a higher upfront premium because both options are centered near the same strike. A long strangle often has a lower upfront premium because the options are separated, but that lower cost comes with a wider movement requirement before the structure reaches a breakeven at expiration.

The comparison is structural, not a ranking. A lower premium does not automatically make the strangle better, and a tighter strike structure does not automatically make the straddle more suitable. The relevant distinction is how strike placement changes cost, breakevens, payoff exposure, and the zone where the full premium can be lost.

Straddle vs Strangle Comparison Table

| Comparison point | Straddle | Strangle |

|---|---|---|

| Basic construction | One call and one put with the same expiration. | One call and one put with the same expiration. |

| Strike relationship | The call and put use the same strike. | The call and put use different strikes. |

| Typical long/debit cost profile | Often higher in many standard long/debit examples because both options are centered near the same strike. | Often lower in many standard long/debit examples because the strikes are separated, though the movement hurdle is wider. |

| Upper breakeven at expiration | Strike plus total premium. | Call strike plus total premium. |

| Lower breakeven at expiration | Strike minus total premium. | Put strike minus total premium. |

| Full premium loss zone at expiration | The full premium can be lost if the underlying finishes at the shared strike. | The full premium can be lost if the underlying finishes between the put strike and call strike. |

| Payoff boundary | More centered around one strike, with breakevens around that same strike. | Wider boundary because the two strikes are separated before premium is added to the breakeven calculation. |

| Volatility exposure | Often used to understand exposure to large movement from a central strike, but live value still depends on implied volatility, time decay, and liquidity. | Often used to understand exposure to larger movement outside separated strikes, but live value still depends on implied volatility, time decay, and liquidity. |

| Exercise / assignment caveat | Expiration payoff math is only one boundary. Before expiration, exercise mechanics and assignment risk can affect interpretation in relevant option contexts. | Expiration payoff math is only one boundary. Before expiration, exercise mechanics and assignment risk can affect interpretation in relevant option contexts. |

| Common confusion | Confused with a strangle because both use a call and a put with the same expiration. | Confused with a straddle because both can express exposure to movement in either direction. |

| Main structural tradeoff | Tighter strike placement, often higher premium, closer breakevens. | Separated strike placement, often lower premium, farther breakevens. |

Same Scenario, Different Structure

Assume an investor is studying a stock before a major information event. The investor does not know whether the stock will move higher or lower, but wants to understand how option structures can reflect exposure to a large move in either direction. No real ticker or recommendation is needed for the comparison.

With a straddle, the call and put are placed at the same strike. The structure is centered around one price area, so the total premium is paid for exposure on both sides of that shared strike. At expiration, the underlying has to move above the upper breakeven or below the lower breakeven before the structure moves beyond the total premium cost.

With a strangle, the call and put are placed at different strikes. The initial premium may be lower, but the underlying has to move beyond a farther upper or lower breakeven because the option strikes start farther apart. The same broad volatility view becomes a different contract shape: the straddle concentrates exposure around one price, while the strangle creates a wider middle zone before either side reaches a breakeven.

Payoff, Premium, and Expiration Risk Boundaries

For a long straddle, the expiration breakevens are based on the shared strike and the total premium paid. The upper breakeven is the shared strike plus total premium, and the lower breakeven is the shared strike minus total premium.

For a long strangle, the expiration breakevens are based on the two separated strikes and the total premium paid. The upper breakeven is the call strike plus total premium, and the lower breakeven is the put strike minus total premium.

Boundary note: Standard payoff diagrams are expiration simplifications. Before expiration, the structure can be affected by implied volatility changes, time decay, liquidity, bid/ask spreads, early exercise considerations where applicable, and assignment risk in relevant option contexts. The expiration payoff boundary is useful, but it does not fully describe live option behavior before expiration.

The full premium loss area is also different. A straddle can lose the full premium at expiration if the underlying finishes at the shared strike. A strangle can lose the full premium at expiration if the underlying finishes between the put strike and the call strike, because both options can expire out of the money within that middle zone.

Common Confusion: Similar Volatility View, Different Contract Shape

Common mistake: Treating a strangle as simply a cheaper straddle can hide the real tradeoff. The strangle may require less upfront premium, but the separated strikes usually push the breakevens farther away. Lower upfront cost changes the payoff boundary; it does not automatically improve the structure.

The useful distinction is contract shape. Both structures can be associated with exposure to movement in either direction, but they do not create the same breakeven map. The straddle concentrates the call and put around one strike. The strangle spreads the call and put across two strikes, which creates a wider middle zone and a different premium-to-movement relationship.

Short straddles and short strangles reverse the premium logic and introduce different obligation and assignment considerations. They are not the main focus here because the broad comparison is best resolved first through the long/debit structure: same strike versus different strikes, then premium, breakevens, and payoff boundary.

When to Study Each Structure Separately

When the call and put share one strike, the relevant debit structure is a long straddle. Its main comparison points are the shared strike, total premium, and breakevens around that single strike.

When the call and put use separated strikes, the relevant debit structure is a long strangle. Its main comparison points are the separated call and put strikes, wider middle zone, and breakevens outside both strikes.

FAQ

Is a straddle the same as a strangle?

No. Both structures use a call and a put with the same expiration, but a straddle uses the same strike for both options, while a strangle uses different strikes.

Why can a strangle have a lower premium than a straddle?

A strangle often uses options with strikes farther away from the current price area, so the upfront premium may be lower. That lower premium usually comes with farther breakevens because the call and put strikes are separated before total premium is added to the calculation.

Does lower premium make a strangle better?

No. Lower premium changes the cost hurdle, but it does not automatically make the structure better. The underlying usually needs to move farther before a long strangle reaches a breakeven at expiration.

Are payoff diagrams enough to compare straddles and strangles?

Payoff diagrams are useful for expiration boundaries, but they simplify live option behavior. Before expiration, implied volatility, time decay, liquidity, bid/ask spreads, and exercise or assignment considerations can affect interpretation.